A Sovereign Debt Fund Can’t Save Social Security

Social Security is projected to be insolvent in less than seven years. Lawmakers need to make changes to the funding and benefit structure of this important program as quickly as possible to avoid a 24% across-the-board benefit cut in 2032. A number of solvency plans have been put forward from the left, right, and center to gradually bring the revenues and benefits back into alignment.

An alternative proposal from Senator Bill Cassidy (R-LA) – which has been supported by Senator Tim Kaine (D-VA) and several other senators – would instead borrow an unprecedented amount of money to fund benefits and invest in the stock market. (At a hearing on March 25, Senator Kaine indicated that the proposed investment fund is intended as one "ingredient" within a broader solvency package, though no other ingredients have been specified.) This is a dangerous debt-funded gamble that would come with huge risks and costs.

The proposal would issue $1.5 trillion of debt to fund investments in the stock market and then allow Social Security to borrow over the next 75 years to pay scheduled benefits. After 75 years, assets in the investment fund would be sold and transferred back to Social Security in an effort to ultimately refund Social Security’s borrowing.

Although the plan in some ways resembles a sovereign wealth fund, it would be financed completely with new borrowing, and it might be better described as a Sovereign Debt Fund (SDF). Unfortunately, the proposal is likely to worsen the overall fiscal situation and introduce significant risks to the budget, the Social Security program, the economy, and public policy.

Over the Trustees’ 75-year projection window and relative to what is allowed under the law, we find that borrowing to fund Social Security under the SDF plan as we understand it would:

- Add up to $170 trillion to the debt when adjusted for inflation, or $775 trillion nominally

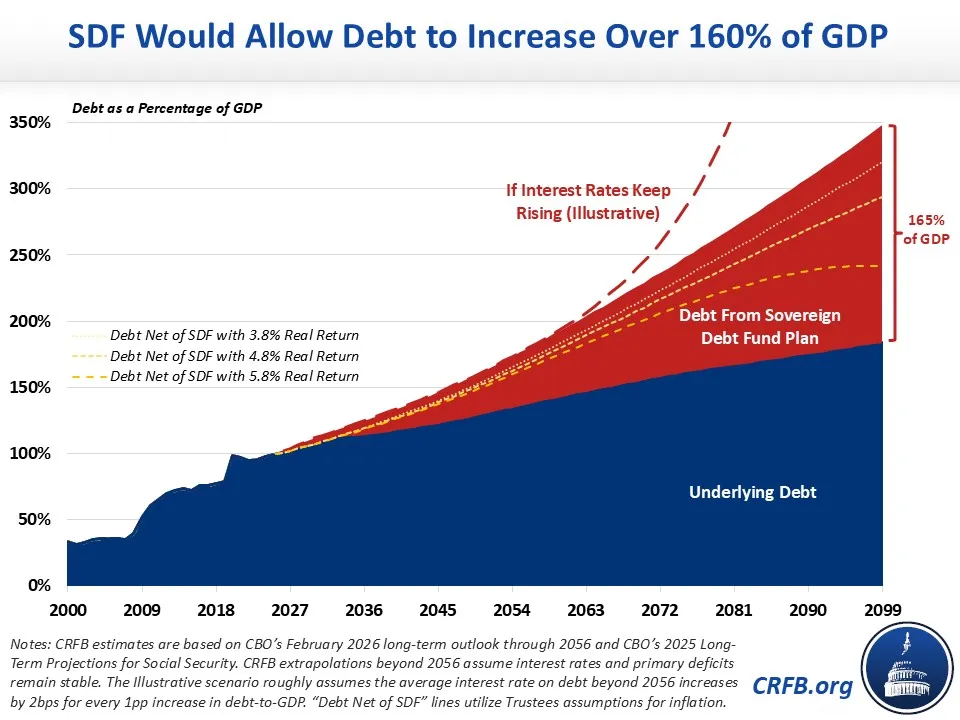

- Boost debt-to-GDP by at least 140% of Gross Domestic Product (GDP) – potentially sparking a debt crisis

- Expose Social Security to significant stock market risk, requiring high and highly uncertain returns to generate the needed funds

- Push up interest rates on government debt and push down returns on private investments

- Make the federal government a major shareholder of private companies

- End Social Security’s current structure as a self-financed, contributory program

- Open the door to “free lunch” budget gimmicks for future tax cuts or spending

A number of experts across the political spectrum have raised concern about the many costs and risks associated with the SDF approach. Last year, we explained how funding the Social Security shortfall through general revenue would be a costly mistake. A Sovereign Debt Fund would essentially build upon this idea by borrowing to pay benefits and then borrowing even further to fund new investments. Building on our previous piece, the below analysis explains why this could be an even costlier mistake.

What is the Sovereign Debt Fund proposal?

The Sovereign Debt Fund (SDF) proposal is a plan developed by Senator Cassidy and supported by Senator Kaine and several other senators from both parties. The plan aims to fund Social Security’s shortfall retroactively by investing funds in the stock market and allowing them to grow over a very extended period of time.

Although numerous iterations of the SDF have been discussed, the version put forward last summer would, to our understanding:

- Allow the Social Security trust fund to exhaust its reserves and then go into debt for the next 75 years in order to continue paying scheduled benefits in excess of revenue collection

- Issue $1.5 trillion in new federal debt over five years to invest in the stock market, keeping the investments and returns in the market for 75 years without withdrawal

- Use the investment fund, after 75 years of growth, to refund Social Security’s 75-year borrowing

Supporters of the SDF plan have sometimes discussed combining it with solvency-improving benefit or revenue adjustments or a tax ‘backstop’ – though none of these ideas are mentioned in the most recent discussion of the proposal, and in all cases the investment fund would be made responsible for closing the lion’s share of Social Security’s shortfall.

The Sovereign Debt Fund Plan Would Allow Massive Borrowing

At 100% of GDP, the national debt is already twice the historic average and on course to exceed the previous record of 106% – set just after World War II – by 2030. The Sovereign Debt Fund plan would substantially increase this borrowing.

Importantly, the SDF plan would authorize more borrowing in two distinct ways. First, it would require issuing $1.5 trillion of debt – along with 75 years of subsequent interest payments – in order to fund new investments in the stock market. And more significantly, the SDF plan would allow Social Security to borrow to fund its shortfall for the next 75 years.

Although CBO’s baseline assumes Social Security will continue to pay scheduled benefits – an assumption that is responsible for much of the projected debt-to-GDP growth in the coming decades – the law does not allow payments to be made beyond trust fund assets and dedicated revenue.

Using assumptions from the Social Security Trustees, we estimate the SDF plan would allow $170 trillion of new borrowing on a real (inflation-adjusted) basis, or $775 trillion on a nominal basis, over the next 75 years. On a present value basis, it would require $29 trillion of borrowing. Using CBO assumptions, real and nominal borrowing would be somewhat lower but present value borrowing would be higher. Most of the new debt – about 95% – would be used to cover Social Security’s shortfall.

Borrowing Needed to Fund a General Revenue Transfer to Social Security, Including SDF (2026-2099)

| CBO | Trustees | |

|---|---|---|

| Nominal Borrowing | $690 trillion | $775 trillion |

| Real (inflation-adjusted) Borrowing | $160 trillion | $170 trillion |

| Present Value Borrowing | $36 trillion | $29 trillion |

| Borrowing as a Percentage of Final Year GDP | 165% | 140% |

Sources: Committee for a Responsible Federal Budget, Congressional Budget Office, and Social Security Trustees. Note: Numbers are rough and rounded.

Assuming steady interest rates and economic growth, this borrowing would increase debt by more than 140% of GDP by 2099 using the Trustees’ assumptions and nearly 165% of GDP using CBO’s. This would come on top of the federal government’s large “on-budget” debt and could more than double total projected debt levels. In all likelihood, such high levels of debt would cause a rapid debt spiral long before the end of the century, leading debt to grow at an accelerating pace and perhaps sparking a fiscal crisis.

If the debt did begin to spin out of control at some point in the next few decades, lawmakers might be able to sell off assets from the Sovereign Debt Fund as part of an effort – that would also need to incorporate significant spending cuts and/or tax increases – to stem off a full-blown fiscal crisis. But doing so would forestall the asset growth needed to refund Social Security’s borrowing and could very well come at a time when markets are already under significant stress.

The Sovereign Debt Fund Exposes Social Security to Substantial Stock Market Risk

After 75 years, the SDF plan intends to “pay back” the $775 trillion of new borrowing through returns from stock market investments. This would be a massive gamble. The higher expected return to stocks over government bonds reflects greater levels of risk. For that reason, economist Deborah Lucas explains that “a debt-funded investment in risky assets does not improve the government’s fiscal position.”

In order to generate enough returns, stocks in the investment fund would need to grow by 9 to 13 percent per year, depending on the allocation of the fund’s investments. This is not impossible but is also far from guaranteed. Over the past 75 years, the average growth in major stock market indices – when adjusted for inflation – has been the equivalent of roughly 9 percent.

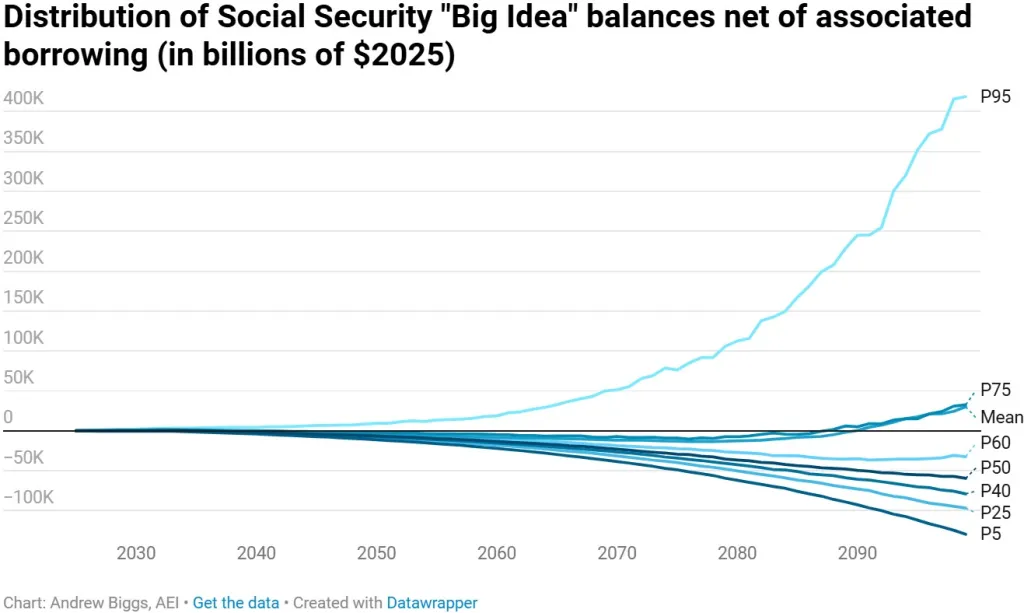

But importantly, higher returns come at the expense of higher risk. And relying on the stock market to fund roughly one-quarter of Social Security’s benefits would put the program at substantial risk. In a recent analysis, Social Security expert Andrew Biggs ran over 1,000 market simulations assuming an average 8.9% annual return. Based on this analysis, Biggs finds only a 30% chance the investment fund will generate enough to pay back the additional borrowing in full – meaning there’s a 70% chance returns will fall short. He finds roughly a 10% chance the fund won’t generate enough to cover any of the borrowing to fund Social Security benefits.

These estimates may in some ways be optimistic, as they assume the fund will be held tight and prudently invested for over seven decades without any withdrawal or political interference. Although the plan does envision protections against political interference, it’s not clear how much can be done legally to prevent Presidential intervention, and there is no mechanism short of a constitutional amendment that could stop Congressional intervention. Future policymakers may try to steer investments by prioritizing political or policy goals over returns, or they may use the available assets or investment income for other needs.

Stock market investment is risky – particularly when done from borrowed funds. While there are public pension programs that rely on the stock market – for example, the National Railroad Investment Trust, California’s CALPERS pension fund, and the Canada Pension Plan’s investments – they are much smaller than Social Security and their investments are made on a funded basis by investing new resources to help fund future benefits, not from additional borrowing.

A Sovereign Debt Fund Comes with Economic Costs and Risks

To the extent the Sovereign Debt Fund plan produces higher returns for Social Security, it will come at the expense of higher debt, rising interest costs, and lower returns in the private sector over the long term. As many experts have pointed out, the plan will reduce the returns to private pensions and retirement accounts – since they will now have to rely more heavily on lower-yield bonds or else seek even riskier investments to achieve the same return. In this sense, as Mark Warshawsky has explained, the proposal effectively “takes resources from the private sector to pay for public benefits.”

Under the SDF plan, the government may also become a major shareholder in many companies, which could inject significant political interference that further undermines economic prosperity and financial returns.

The Sovereign Debt Fund plan would also push up interest rates, which means higher federal deficits and higher costs for mortgages and other borrowing. As a rule of thumb, each percentage point increase in debt-to-GDP boosts long-run interest rates by 2 basis points, suggesting the SDF plan might increase interest rates by 2.8% to 3.3%. The actual impact could differ some since a small portion of that debt would be used to purchase financial assets (though most would be to pay benefits). But assuming such an increase relative to current borrowing rates, 10-year Treasury yields could grow above 7% by the end of the solvency window and average mortgage rates above 9%. For individuals, this could greatly undermine affordability. For Washington, it could cause a debt spiral.

A Sovereign Debt Fund Comes with Political Costs and Risks

Allowing Social Security to borrow for 75 years to pay benefits is likely to undermine its long-standing status as a self-financed, contributory program. Many have argued this could reduce public support for the program, which might no longer be thought of as an “earned benefit.” It would also weaken Social Security’s built in fiscal controls, which currently help to prevent massive spending increases and tax cuts and at least encourage corrective action by limiting outlays to current income and reserves.

Allowing leveraged borrowing to finance Social Security’s future debt also opens the door for a similar “free lunch” budget gimmick in other circumstances. Lawmakers could use a similar mechanism to restore solvency to Medicare, to “pay for” massive new tax cuts or spending programs, or to finance structural deficits projected under current law. If $1.5 trillion of borrowing can generate enough returns to make Social Security solvent, why not engage in even more borrowing to fund Medicare for All or eliminate the income tax?

* * * * *

Social Security is in desperate need of solutions to avoid a scheduled 24% benefit cut and ensure its long-term solvency. Our Social Security Reformer allows users to make the necessary revenue and benefit adjustments, while our Trust Funds Solutions Initiative has put forward several novel ideas.

There are many thoughtful solutions that can deliver benefits more efficiently and produce more winners than losers. Unfortunately, there are no free lunches. The Sovereign Debt Fund plan would put Social Security, the budget, and the economy at risk.

Additional Readings

- Our Bipartisan Plan Could Rescue Social Security, Senators Bill Cassidy and Tim Kaine, Washington Post, July 8, 2025

- Stress-Testing the Cassidy-Kaine “Big Idea” Social Security Plan, Andrew Biggs, American Enterprise Institute, January 6, 2026

- What’s the Big Idea? Sanya Bahal, Emerson Sprik, Bipartisan Policy Center, December 2, 2025

- The Economics of Government Investment Policies and Why They Cannot Undo Fiscal Imbalances, Deborah Lucas, MIT, October 17, 2025

- Cassidy-Kaine Proposal To Borrow For New Trust Fund Is A Bad Idea, Alicia Munnell, Center for Retirement Research at Boston College, October 7, 2025

- The Social Security Funding Crunch Is Looming. Current Proposals from Congress Aren’t Cutting It, Roosevelt Institute, August 21, 2025

- A Risky Plan for Social Security, Andrew Biggs, Wall Street Journal op-ed, July 24, 2025

- The Cassidy-Kaine Social Security Plan Is a Risky Bet with Taxpayer Money, Romina Boccia and Ivane Nachkebia, July 28, 2025

- Quick hits: Reactions to the Proposal by Senators Cassidy and Kaine to Rescue Social Security, Sita Slavov (American Enterprise Institute), Gopi Shah Goda (Brookings Institution), Jason Brown (Brookings Institution), July 21, 2025

- The Fool’s Gold of a US Sovereign Wealth Fund, Romina Boccia, The Hill, February 16, 2025

- A Sovereign Wealth Fund Wouldn’t Work For the US, Tyler Cowen, Bloomberg, September 10, 2024

- Senator Cassidy’s Social Security Solvency Proposal is a Tax on Pension Investments, Mark Warshawsky, American Enterprise Institute, June 12, 2023