CBO Projects Possible Debt Spiral, as R Exceeds G

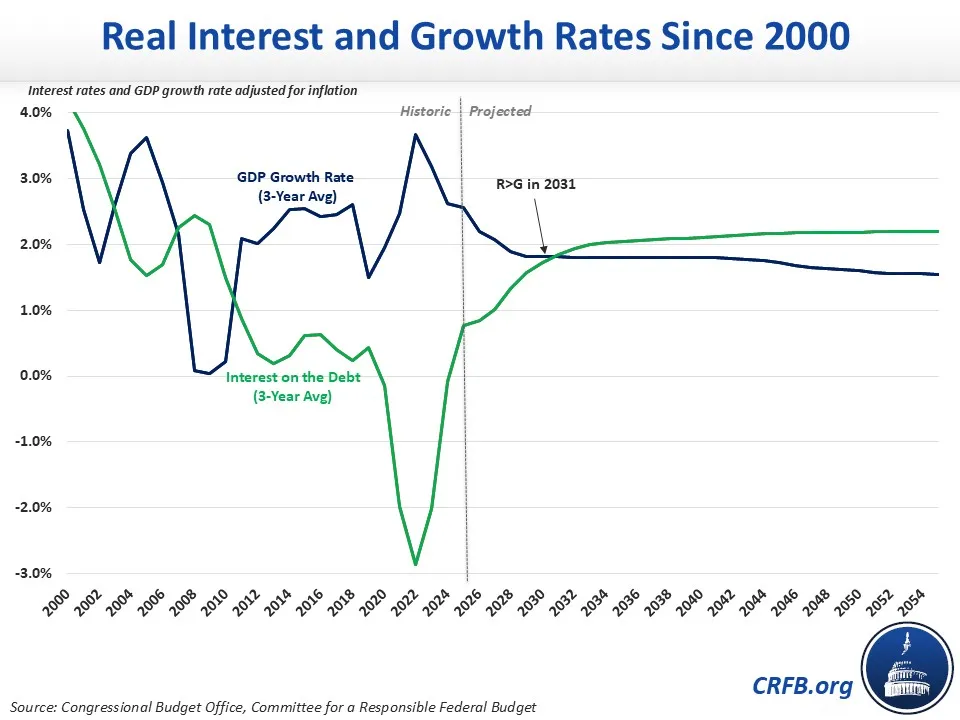

The U.S. national debt has long been on an unsustainable path. Nonetheless, for most of the 20th century, debt sustainability has been bolstered by the fact that the average interest rate paid on the debt (R) has been lower than the rate of economic growth (G). Unfortunately, this may soon no longer be the case. According to the latest estimates from the Congressional Budget Office (CBO), R will exceed G in just five years – by Fiscal Year 2031. Over time, this could lead to a debt spiral, putting the debt on an increasingly unsustainable trajectory and perhaps even sparking a fiscal crisis.

When the interest rate paid on federal debt is below the economic growth rate (R<G), the existing stock of debt will erode relative to the size of the economy. While debt would rise due to interest payments, Gross Domestic Product (GDP) will rise faster and so debt-to-GDP will fall absent additional non-interest borrowing. In this scenario, it is possible for debt to be sustainable even when a country is running persistent (but modest and stable) primary (non-interest) deficits. Once interest rates exceed the growth rate, however, primary deficits will lead debt to grow indefinitely.

For most of the last 60 years and all of the past 15 years, the interest rate has been below the growth rate (R<G) except for brief periods of economic contraction during recessions. Adjusted for inflation, real interest rates on federal debt have averaged 0.9% over the past 15 years, while the real growth rate has averaged 2.2%

However, since 2023, most newly issued debt has paid interest rates above the expected long-term economic growth rate – with most yields ranging between 4% and 5%. As an increasing amount of debt is issued or rolled over at these higher rates, the average interest rate on U.S. debt will exceed the economic growth rate.

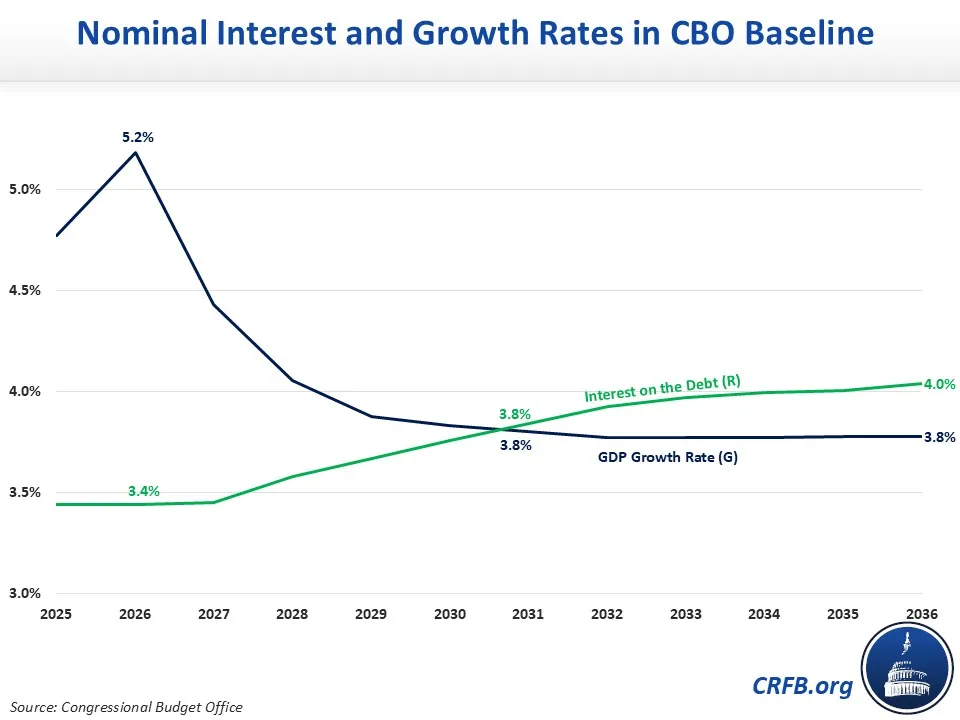

Under CBO’s latest projections, the interest rate will exceed the growth rate (R>G) starting in 2031, when both are projected to total about 3.8% on a nominal basis and 1.8% on a real basis. Over time that gap will widen; by 2056, CBO projects a 4.2% (2.2% real) interest rate compared to a 3.5% (1.5% real) GDP growth rate.

As the gap between the interest rate and growth rate widen, debt sustainability becomes more difficult to achieve. With the 0.7% gap CBO projects, the U.S. would need to run a 0.7% of GDP primary surplus to prevent debt-to-GDP from rising indefinitely. This would mean roughly $2.7 trillion (2.9% of GDP) of spending cuts or tax increases in 2056, alone.

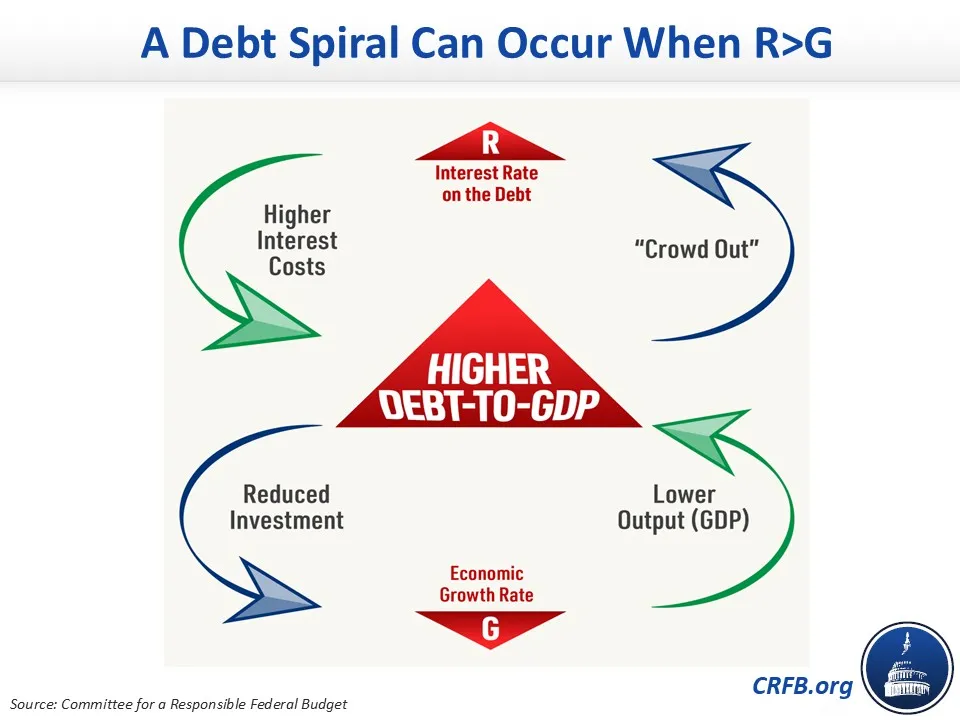

Failure to enact such savings could lead to a debt spiral, where higher debt pushes up interest rates and slows growth, which boosts interest payments and reduces GDP, further pushing up debt and leading to even higher interest rates and thus even higher debt. Over time, this could lead to accelerating growth in the debt, which could eventually be too rapid to correct, absent a major disruption or crisis.

CBO’s current baseline projects only a modest debt spiral, with rising debt slowly pushing up interest rates and pulling down growth – and even under their scenario, debt will grow to an unprecedented 175% of GDP by 2056. If CBO underestimated the neutral interest rate, overestimated potential growth, or miscalculated the level of crowd-out for a given amount of debt, the spiral could be far worse. And if policymakers continue to worsen underlying deficits with further tax cuts and spending increases, the spiral could arrive sooner and with greater intensity than projected.

With R>G expected in the near future, lawmakers should act fast to begin bringing deficits under control, which is the best way to prevent a debt spiral and avoid a potential debt crisis.