Social Security Solvency Can Strengthen the Economy and Budget

The Social Security retirement trust fund is projected to go insolvent in Fiscal Year (FY) 2032 under the Congressional Budget Office’s (CBO) new February 2026 Baseline, almost a year earlier than was estimated last year. The resulting benefit cut could be extremely painful for many seniors counting on benefits. But by bringing Social Security’s dedicated spending and revenue in line, CBO finds it would improve the nation’s fiscal and economic outlook. A more thoughtful reform package could achieve these same benefits with far less disruption.

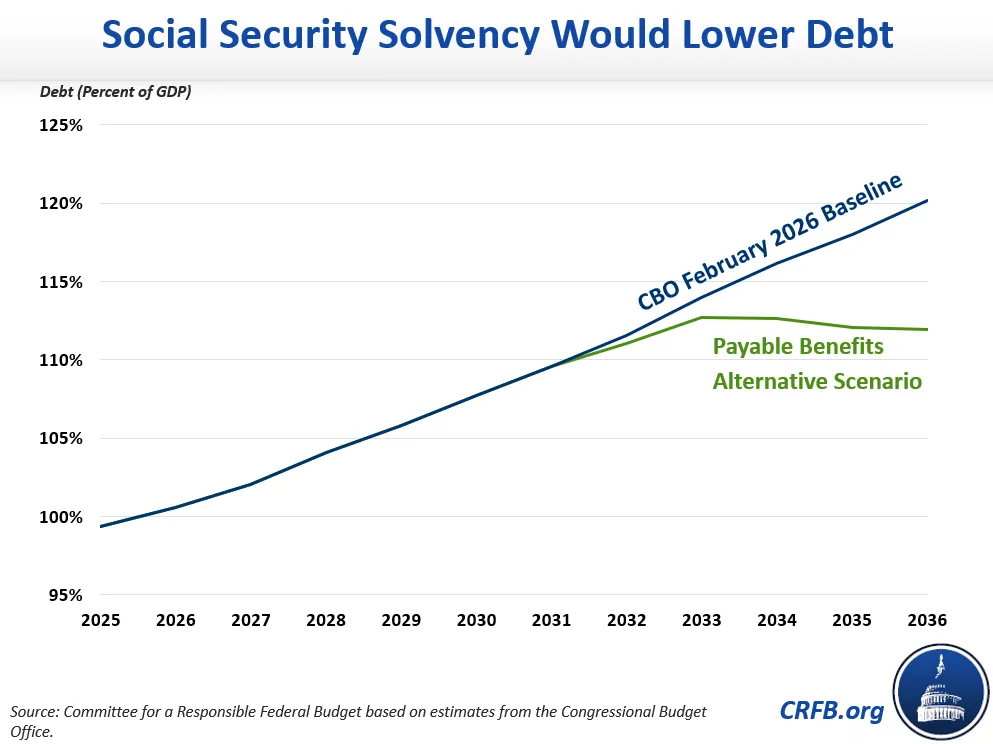

Under CBO’s baseline, which is required by law to assume that Social Security will continue to pay scheduled benefits after its trust funds become insolvent, the national debt is projected to rise from a near-record 100% of Gross Domestic Product (GDP) today to 120% of GDP by FY 2036, and annual deficits will grow to 6.7% of GDP.

But the actual law does not allow Social Security to continue to pay full benefits. In 2032, when today’s 61-year-olds reach the Normal Retirement Age and when today’s youngest retirees turn 68, the Social Security Old-Age and Survivors Insurance (OASI) trust fund is projected to run out of reserves. At that point, benefits must be reduced to match revenue, leading to an average benefit cut of 28% in the years following insolvency, according to CBO.

To estimate the impact of this cut on the budget and economy, CBO now produces an alternative “payable benefits” scenario that assumes Social Security’s benefits are limited to incoming revenues after trust fund exhaustion. Under this scenario, deficits and debt would grow far more slowly upon insolvency. After growing from 100% of GDP today to 111% by 2032, debt would grow just 1 point to 112% by FY 2036 – 8% below baseline projections. Deficits, meanwhile, would fall from 5.6% of GDP in 2032 to 4.7% in 2036, instead of rising to 6.7%.

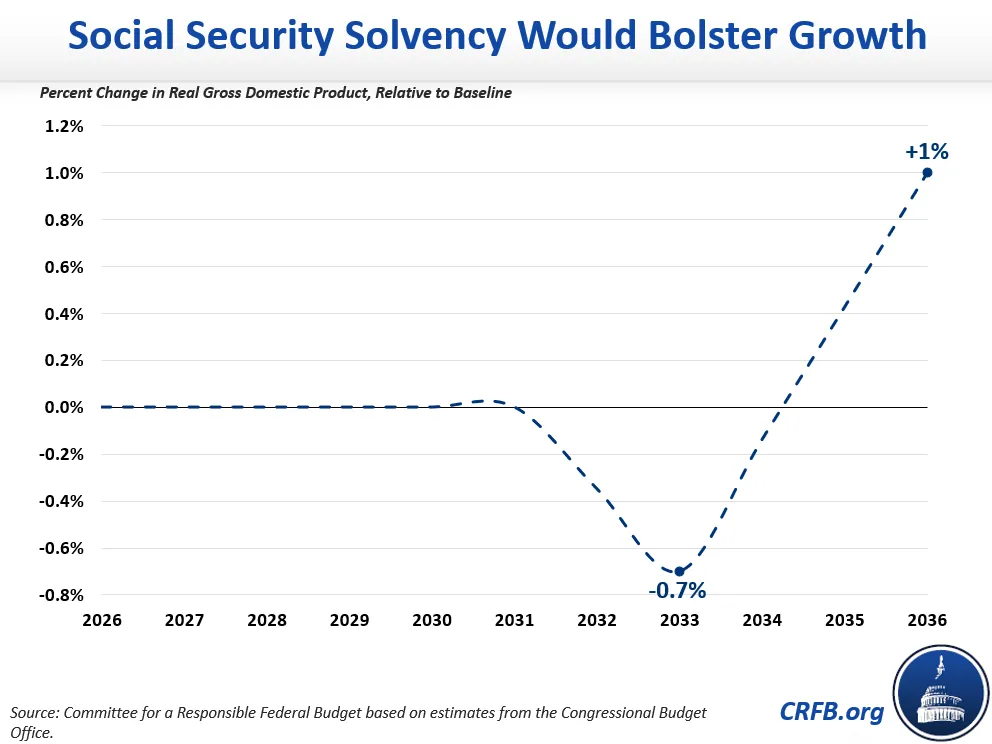

In the near-term, the sharp cut in benefits would weaken the economy, reducing output by 0.7% in FY 2033 (the impact would be moderated by a significant Federal Reserve response).

However, after the initial response, CBO believes the benefit reduction will not only reduce the national debt but also increase the incentive for people to work and save to offset the potential cut. Over time, CBO projects these effects will boost the labor supply and increase the amount of private investment that goes toward factories, machines, software, and equipment. This will in turn put upward pressure on income and output. By FY 2036, CBO expects real output to be 1% higher as a result of bringing Social Security into balance.

Over the longer term, the positive economic effects from lower debt and a Social Security system in financial balance would likely compound. While CBO’s alternative scenario projections end in FY 2036, a 2023 CBO analysis of a similar payable benefits scenario found that real output and per person incomes would be 4.5% higher after 30 years.

Of course, as CBO’s own analysis shows, failure to stop insolvency and an across-the-board benefit cut would be destabilizing in the immediate term, both for retirees and the economy. Cuts would be sudden and indiscriminate – with a typical couple retiring in 2033 facing an $18,400 annual benefit cut.

To avoid this, timely trust fund solutions enacted ahead of time would avert these short-term costs while securing the long-term gains of a solvent system. Any number of potential options exist.

Unlike an across-the-board cut, a comprehensive reform package can be designed to avoid disruptions by phasing in changes gradually, strengthen retirement security, improve the fairness and efficiency of the Social Security system, and significantly improve the budget outlook.

Over time, thoughtful reform has the potential to be far more pro-growth than an across-the-board cut. Penn Wharton Budget Model recently analyzed a series of reform packages that achieve partial solvency, finding they would boost GDP by 2% to 6% by 2060. In our own estimates of a specifically pro-growth solvency reform, we found it could boost Gross National Product by 8% in 2060. As these figures show, policies aimed at promoting work, savings, investment, and productive aging have the potential to bolster incomes as well as support solvency goals.

As CBO’s analysis underscores, policymakers should begin the urgent work of shoring up Social Security’s finances and restoring long-term solvency to the program. Even blunt and abrupt changes to bring Social Security into balance would meaningfully improve the budget and economy over time. A thoughtful solvency package could go a long way toward boosting incomes and fixing the debt.