Waiting To Rescue Social Security Has Weakened Our Options

Social Security’s retirement trust fund is less than seven years from insolvency, at which point beneficiaries face the prospect of a 24% benefit cut. Social Security’s looming insolvency has been well known and understood for over three decades, yet policymakers have refused to act – except to make its finances worse. This delay has narrowed the available options – compared to 30 years ago, adjustments will now have to be larger, phased in quicker, and enacted with much less warning.

As an example, either eliminating the payroll tax cap or applying progressive price indexing to benefits above the 30th percentile of earners would have each restored 75-year solvency on their own if enacted back in the 1990s.1 These same options enacted today would be far less effective. Eliminating the tax cap today would close two-thirds of the solvency gap and delay insolvency by 21 years. Progressive price indexing would close half of the solvency gap and only delay insolvency by one week. Restoring sustainable solvency today would require enacting both policies together.

Waiting For Solvency Has Narrowed the Options

| Enacted in 1995 | Enacted in 2026 | |

|---|---|---|

| Solvency Gap Closed over 75-Year Window | (1995-2069) | (2025-2099) |

| Eliminate Tax Cap | 120% | 65% |

| Progressive Price Indexing | 105% | 50% |

| Eliminate Tax Cap & Progressive Price Indexing | 225% | 110% |

| Solvency Gap Closed Through 2099 | (1995-2099) | (2025-2099) |

| Eliminate Tax Cap | 90% | 65% |

| Progressive Price Indexing | 110% | 50% |

| Eliminate Tax Cap & Progressive Price Indexing | 200% | 110% |

| Year of Combined Trust Fund Insolvency | ||

| Eliminate Tax Cap | 2094 (+60 years) | 2055 (+21 years) |

| Progressive Price Indexing | Never | 2034 (+1 week) |

| Eliminate Tax Cap & Progressive Price Indexing | Never | Never |

Source: CRFB estimates based on estimates from the Social Security Administration’s Actuarial Services, rounded to the nearest 5%.

Note: Figures represent current estimates of what the policies would have achieved, not estimates made in 1995. Options were modeled based on actual historical outcomes and projections from the 2025 Social Security Trustees Report, adjusted for the impact of the One Big Beautiful Bill Act. Estimates based on theoretically combined old-age and disability trust funds, which are projected to be insolvent in 2034.

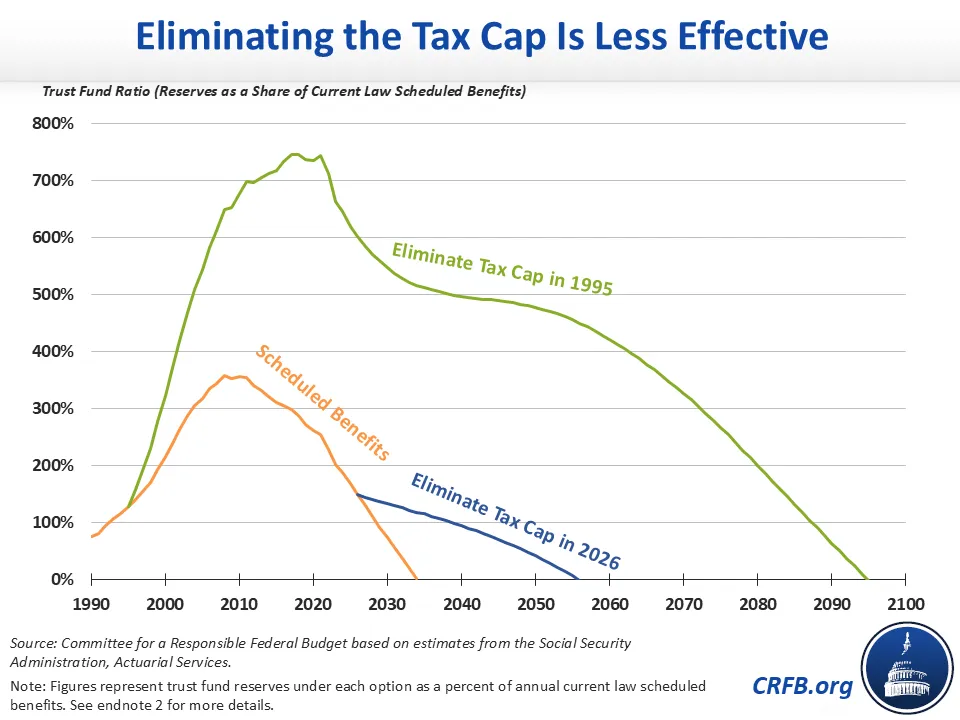

Compared to the 1990s, eliminating the Social Security taxable maximum (the “tax cap”) is no longer sufficient to restore 75-year solvency on its own.

Currently, the 12.4% Social Security payroll tax is applied to each worker’s first $184,500 of earnings, with benefits calculated based on those earnings. Each year the cap grows with average wages.

Had policymakers eliminated the cap and applied the payroll tax to all wages starting in 1995, without crediting additional benefits, it would have generated enough revenue to extend solvency by 60 years to 2094. This would have achieved 75-year solvency at the time (through 2069) and closed 90% of the current solvency gap through 2099.

By comparison, eliminating the tax cap today would extend solvency by just 21 years – one-third as long as back in the 1990s – and close 65% of the solvency gap.2

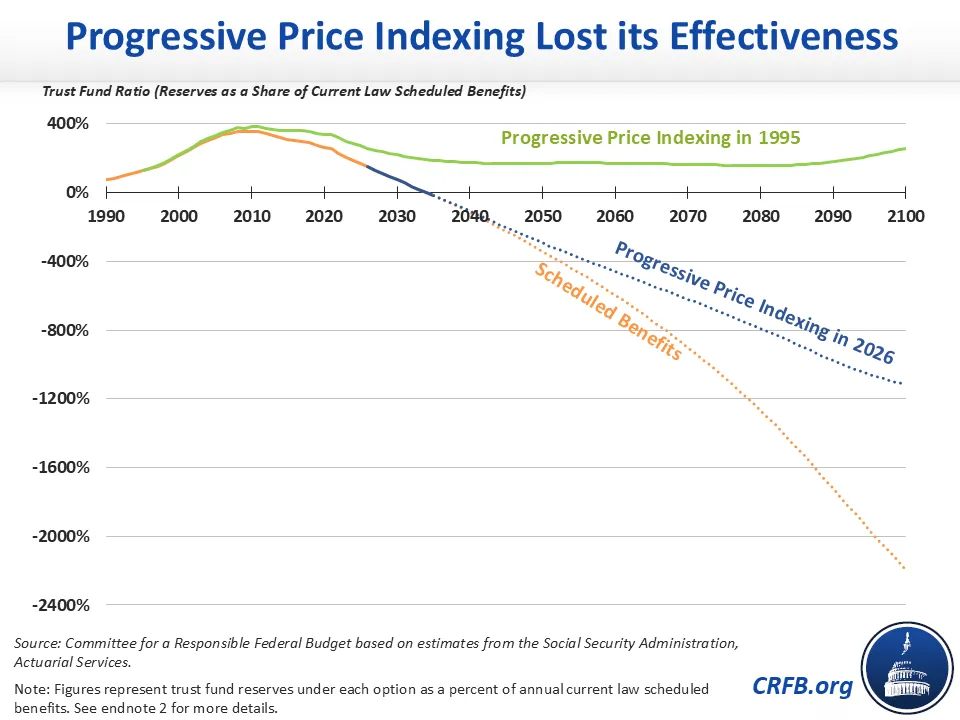

Progressive price indexing has seen an even more significant decline in its effectiveness relative to enacting it decades ago.

Social Security’s initial benefits grow each year, roughly with wages, due to indexation of the benefit formula. One common idea to restore solvency, coined “progressive price indexing,” would adjust the benefit formula so that benefits continue to grow with wages for low earners, grow with prices for the highest earners, and grow on a sliding scale in between for most workers.

Had policymakers applied progressive price indexing above the 30th percentile of earners in 1995, it would have generated enough savings to permanently restore solvency to the program.

That same policy enacted today would only extend solvency by roughly one week and would close half the program’s 75-year solvency gap.

Importantly, while progressive price indexing would no longer delay insolvency whereas eliminating the tax cap would, progressive price indexing would still do more to close Social Security’s long-term structural gap. By 2099, progressive price indexing would almost eliminate Social Security’s cash deficit, while eliminating the tax cap would only reduce it by half – or by less than one-third if new benefits were paid on wages newly subject to the tax.

Nonetheless, both approaches would be less effective at improving the program’s finances than they would have been if enacted decades ago.

This same loss of effectiveness would also apply to other options to secure Social Security. The choice to delay action means that any revenue or benefit adjustments will now be applied to and spread across fewer cohorts of workers and beneficiaries, will benefit less from the growth of compound interest, and will have little room with which to phase in changes incrementally. Delay has also reduced the ability of policymakers to ensure maintenance or growth in the real value of benefits over time, to exempt certain groups from adjustments and to give workers ample time to plan and adjust for any changes.3

Further delay would only compound these challenges. For example, solvency could still be restored today by both eliminating the tax cap and by adopting progressive price indexing. If lawmakers delay action until 2034, however, even adopting both measures together would only push back the theoretically combined insolvency date by six months. The combination would also fall short of fully restoring 75-year solvency, even with temporary borrowing authority.

Lawmakers have committed policy malpractice by failing to restore solvency decades ago and have compounded this error with recent legislation that actually worsened solvency.

Every year of delay promises more pain to come by requiring more changes to be implemented at a faster rate to avert insolvency. Fortunately, most of the solutions to rescue Social Security are well-known, and we are releasing a number of novel solutions to supplement the existing menu.

The best time to rescue Social Security was three decades ago. The next best time is now.

1 This particular option would create a new bend point at the 30th percentile of earnings, splitting the current 32% PIA factor into two segments. The upper 32% factor and the 15% factors would be reduced annually so that the maximum initial benefit grew at the same pace as the consumer price index, while the 90% and lower 32% factor would not be affected.

2 The Trust Fund ratio charts below represent trust fund reserves under each option as a percent of the annual costs scheduled under current law, referred to as Scheduled Benefits on the charts. This measure makes options and current law more comparable in magnitude, as compared to the conventional approach that measures trust fund reserves compared to post-policy costs (the difference can be significant when a policy substantially reduces or increases annual costs). Using the conventional metric, trust fund ratios in 2099 under the tax cap would equal -55% if starting in 1995 and -720% if starting in 2026, compared to -55% and -705%, respectively, under the approach used here. For progressive price indexing, trust fund ratios in 2099 under the conventional approach would equal 395% if starting in 1995 and -1,515% if starting in 2026, compared to 250% and -1,110%, respectively, under our approach.

3 Importantly, restoring sustainable solvency will eventually require bringing revenue and costs into rough balance, which means by some date in the very distant future there may be little difference in benefits received or taxes paid regardless of start date. However, the difference can be quite large over the intervening decades.