Rising Interest Rates are Exploding the Debt

The 30-year Treasury note just reached its highest yield in almost 19 years, 5.2%, and other interest rates are approaching similar highs. This week the 10-year Treasury yield hit 4.7%, around 55 basis points above projections from the Congressional Budget Office (CBO). If interest rates remain this far above projections across the yield curve, it would have large fiscal consequences. Under this scenario, we estimate:

- Debt would increase an additional $2.0 trillion over a decade, reaching 125% of Gross Domestic Product (GDP) by 2036.

- Interest costs would grow from a record 3.2% of GDP ($970 billion) in 2025 to 5.3% of GDP ($2.5 trillion) by 2036.

- Interest would consume 30% of revenue by 2036, up from 19% in 2025.

- On a per household basis, interest costs would grow from $7,900 today to $17,000 by 2036.

- Interest costs would become the second largest government program next year, exceeding defense, Medicare, and Medicaid.

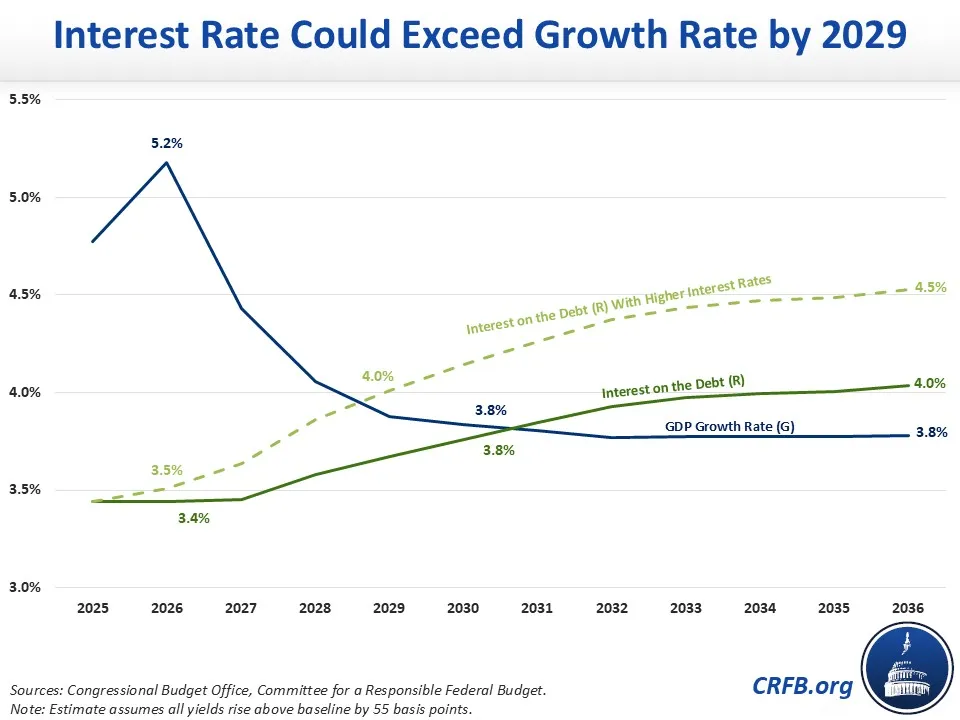

- The average interest rate would exceed the economic growth rate (R>G) by 2029, with the gap reaching 75 basis points by 2036.

- Interest rates on consumer loans would increase, pushing mortgage costs up by thousands of dollars.

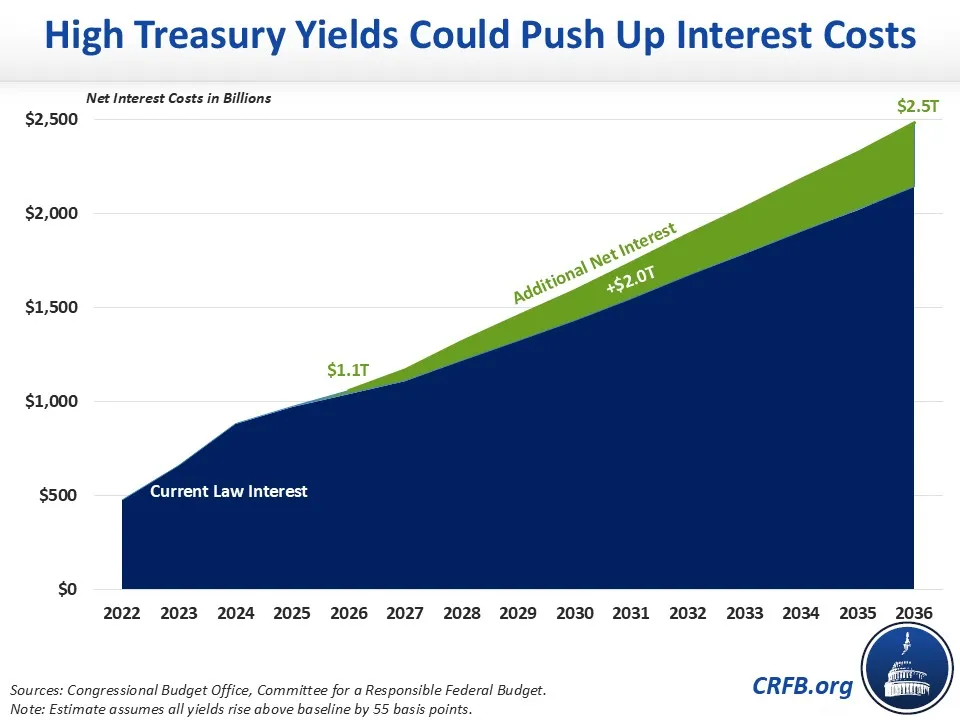

Interest Costs Could Grow by $2 Trillion

If Treasury yields remain 55 basis points above CBO’s projections over the next decade, the federal government would spend an additional $2 trillion in interest costs. Under this scenario, interest costs would grow 2.5 fold, from $970 billion in Fiscal Year (FY) 2025 to $2.5 trillion by 2036. Debt under this scenario would rise from around 100% of GDP today to a record 125% by 2036, compared to 120% under CBO’s baseline.

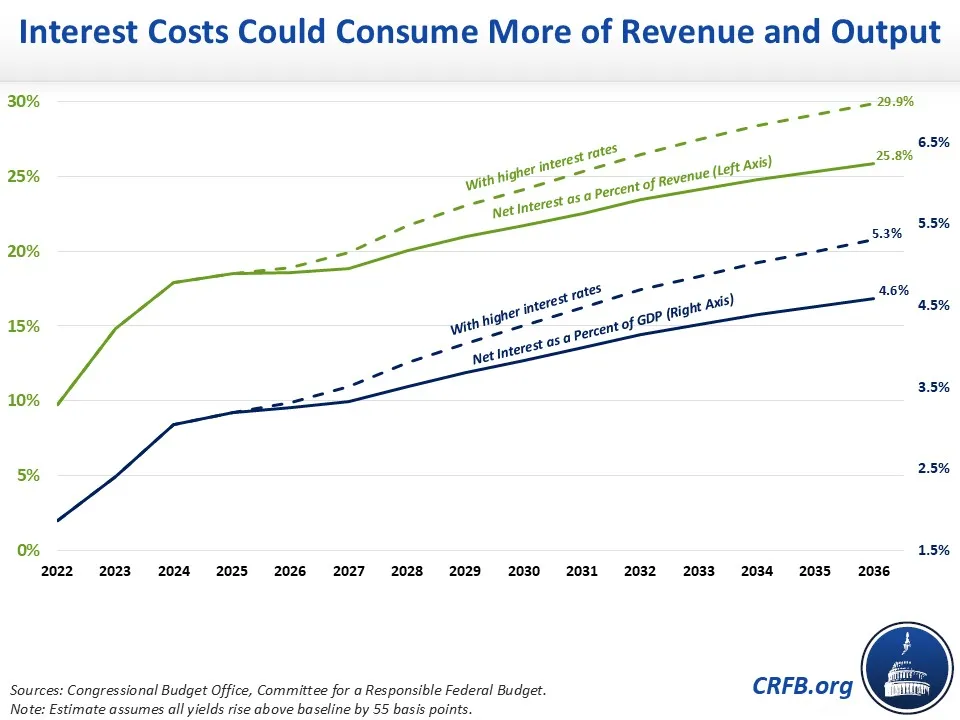

Interest Could Consume 30% of Revenue

Interest costs as a share of GDP have already exceeded the record, 3.2%, and would grow to 5.3% of GDP by 2036 if rates remain elevated. Interest would consume almost 30% of all revenue by 2036 under this scenario, up from 19% today and 12% on average over the past half century.

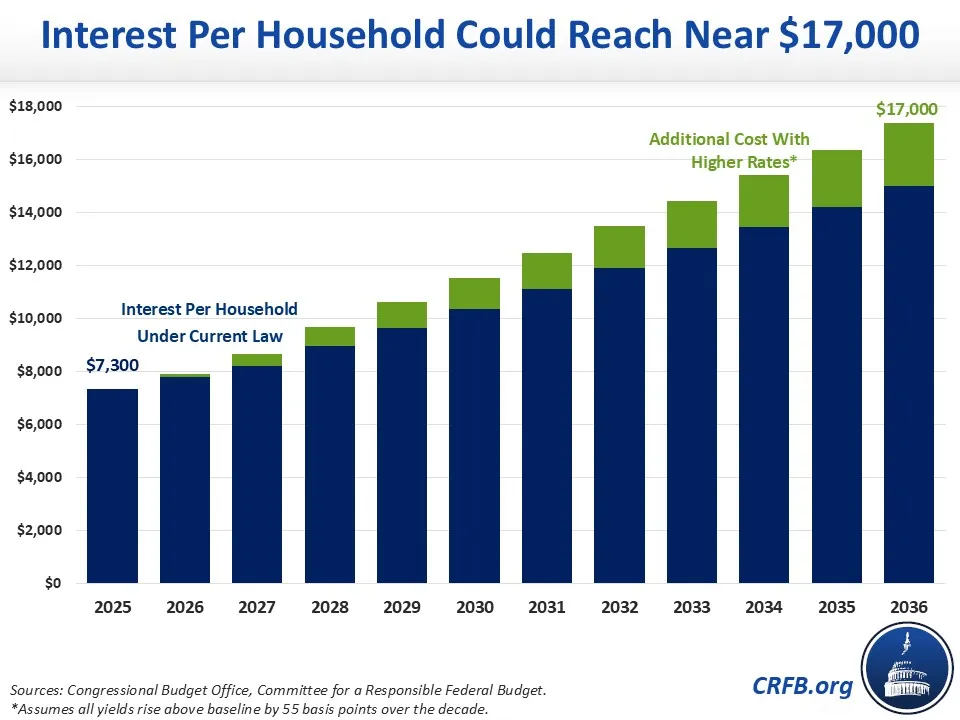

Interest Per Household Could Double

The amount of net interest per household that the federal government pays exceeded $7,300 in FY 2025. If interest rates remain 55 basis points above projections, net interest costs per household would exceed $11,000 by FY 2030 and $17,000 by 2036. Higher rates explain about $2,000 more per household of this increase.

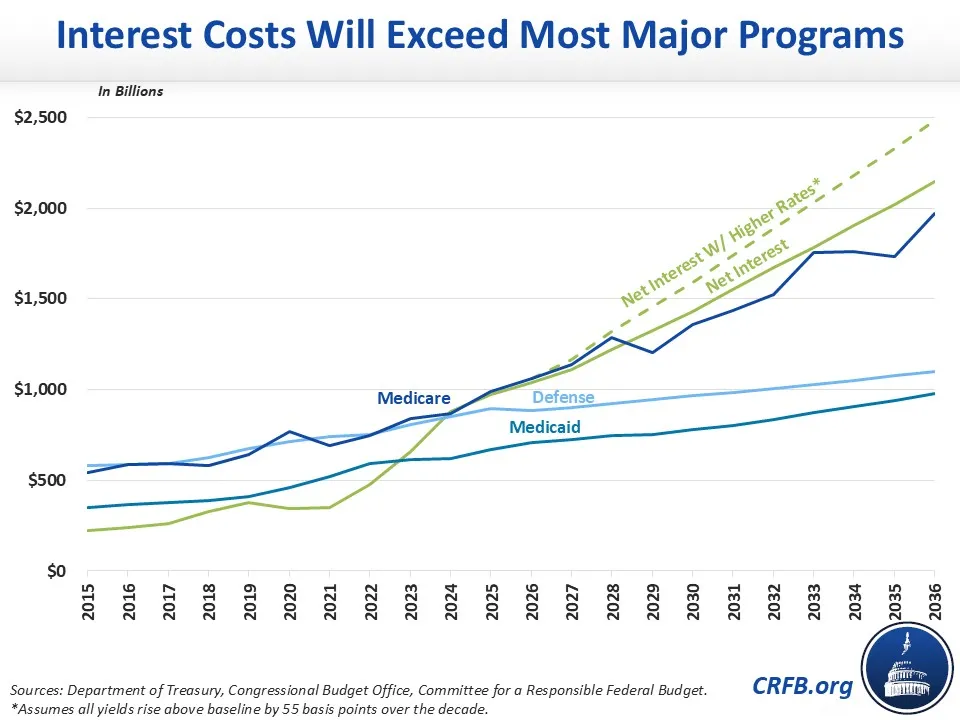

Interest Could Crowd Out Other Spending

Today, the federal government spends more on interest than on Medicaid, national defense, and total nondefense discretionary spending. With higher rates, interest costs would exceed Medicare spending next year – in FY 2027 – making it the second largest government program. By 2036, the federal government would spend almost as much on interest as on Social Security’s retirement program.

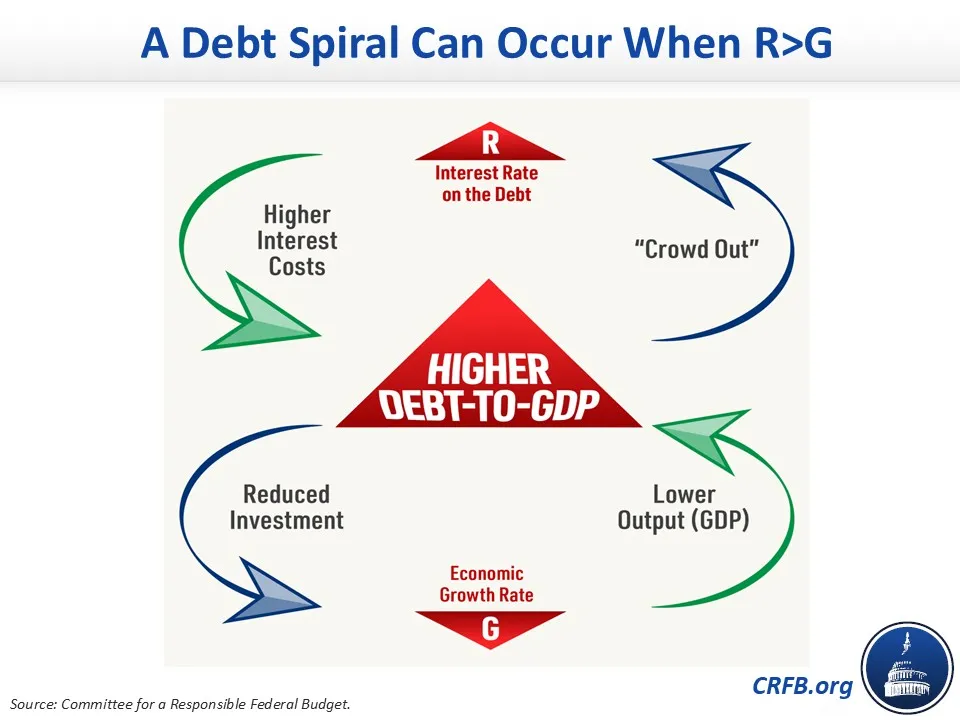

With R>G, the U.S. Could Face a Debt Spiral

As the average interest rate on debt (R) rises above the economic growth rate (G), debt can begin to rise rapidly and uncontrollably. With higher interest rates on new debt, R>G by 2029 – and by the end of the decade, interest on the debt could be 75 basis points above the growth rate. With such a large gap, debt would rise rapidly even if policymakers balance the non-interest part of the budget.

The combination of high levels of debt and a large gap between R and G can lead to a debt spiral, where rising interest costs boost debt, rising debt boosts interest rates (and slow growth), rising rates boost interest costs, and debt-to-GDP grows at an increasing and increasingly-unsustainable pace. This could ultimately spark a debt crisis.

Consumer Debt Would Become More Costly

Higher yields on Treasuries can also push up interest rates paid by ordinary Americans on mortgages, car loans, and business loans.

As an example, a 55 basis point increase in mortgage rates would increase monthly payments on a $500,000 30-year mortgage by almost $200 and would increase the lifetime cost of the mortgage by $64,000. For a million-dollar mortgage, the same change in rates would increase monthly payments by $350 and lifetime costs by nearly $130,000.

There’s No Time to Lose to Tackle the Debt

Lawmakers must work both to bring down interest rates and to prevent high rates from crowding out other priorities or sparking a fiscal crisis. The best way to accomplish these goals is through deficit reduction, which can help the Federal Reserve lower rates by reducing near-term inflationary pressures, put downward pressure on long-term rates by reducing economic crowd-out, and reduce the debt burden on which the government must pay interest. With debt approaching record levels, there is little time to lose.