Analysis of the 2026 Social Security Trustees' Report

The Social Security and Medicare Trustees released their annual reports today on the financial status of the programs. The Trustees find that these programs are approaching insolvency and face large long-term shortfalls, necessitating trust fund solutions. The 2026 Social Security Trustees' Report projects:

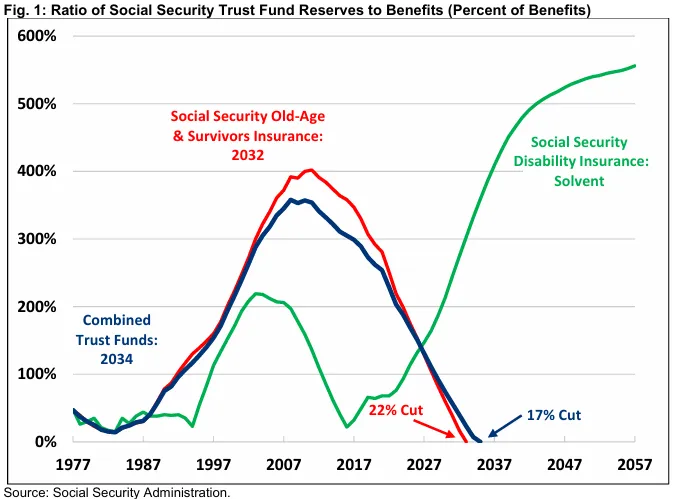

- Social Security is only six years from insolvency. The Old-Age and Survivors Insurance (OASI) trust fund is projected to be insolvent in 2032, when today’s youngest retirees turn 68, at which point retirees face an automatic 22% benefit cut. On a theoretically combined basis, the OASI and Disability Insurance trust funds will run out in 2034, leading to a 17% benefit cut.

- Social Security faces large and growing imbalances. Social Security faces cash deficits totaling $3.8 trillion over the next ten years, the equivalent of 2.7% of taxable payroll or 0.9% of Gross Domestic Product (GDP). Annual cash deficits will grow to 3.7% of payroll (1.3% of GDP) by 2050 and to 6.6% of payroll (2.2% of GDP) by 2100.

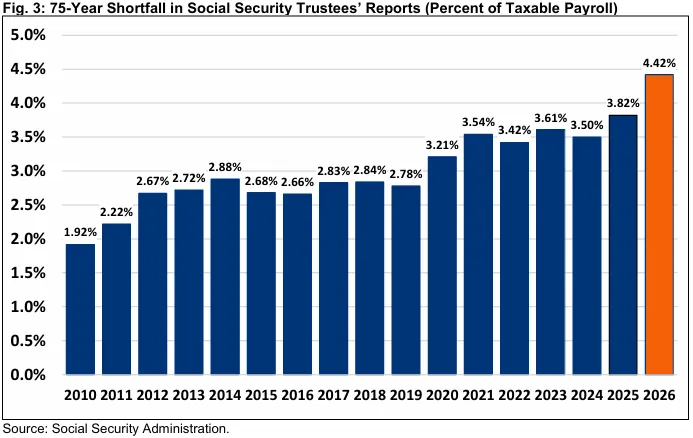

- Social Security faces a large actuarial shortfall. Over the next 75 years, Social Security faces a 4.42% of payroll (1.5% of GDP) actuarial deficit, the equivalent of $31 trillion on a present value basis.

- Social Security’s financial outlook has substantially worsened. Social Security’s 75-year solvency gap has grown 16% relative to last year’s projections, from 3.82% of payroll to 4.42% of payroll. Over half of this deterioration was due to lower projected fertility rates while a third was the result of lower assumed immigration. A quarter of the increase was due to the enactment of the One Big Beautiful Bill Act, which reduced revenue from the income taxation of Social Security benefits.

- It’s time for trust fund solutions. Policymakers are running out of time to enact the reforms necessary to prevent trust fund insolvency. The longer they wait, the fewer policy options that will be available and the less time there will be to phase in reforms that give workers and retirees time to prepare.

Social Security is on a collision course toward insolvency. If policymakers fail to act, they will effectively be supporting a 22% benefit cut for all retirees, survivors, and their dependents in just six years. Fortunately, there is still time for policymakers to enact pro-growth solutions that protect the long-term viability of the program and that give participants time to plan and adjust.

Social Security is Nearing Insolvency

According to the Social Security Trustees, Social Security’s Old-Age and Survivors Insurance (OASI) trust fund will become insolvent in just six years, in 2032, when today’s youngest retirees turn 68. If trust fund reserves are reallocated from Social Security’s Disability Insurance (SSDI) trust fund, the theoretically combined trust funds will be exhausted two years later in 2034.

Social Security cannot legally spend more than its revenues and assets, necessitating a 22% cut in retirement benefits when OASI’s trust fund is exhausted, growing to 38% at the end of the century. We previously estimated the impact of a similar cut, finding that a typical couple retiring in 2033 would face an $18,400 annual reduction to their benefits. We also recently produced a state-by-state analysis of the effect of the cut if imposed today.

If the OASI and SSDI trust funds were theoretically combined, beneficiaries would instead experience a 17% benefit cut in 2034, growing to 35% by 2100. The projections of the Social Security Trustees are similar to those released by the Congressional Budget Office (CBO) earlier this year, which found the OASI fund would go insolvent in fiscal year 2032, leading to a 28% average cut to benefits in the years following insolvency, while the theoretically combined trust funds will run out of reserves in 2033.

Social Security Faces Large and Growing Imbalances

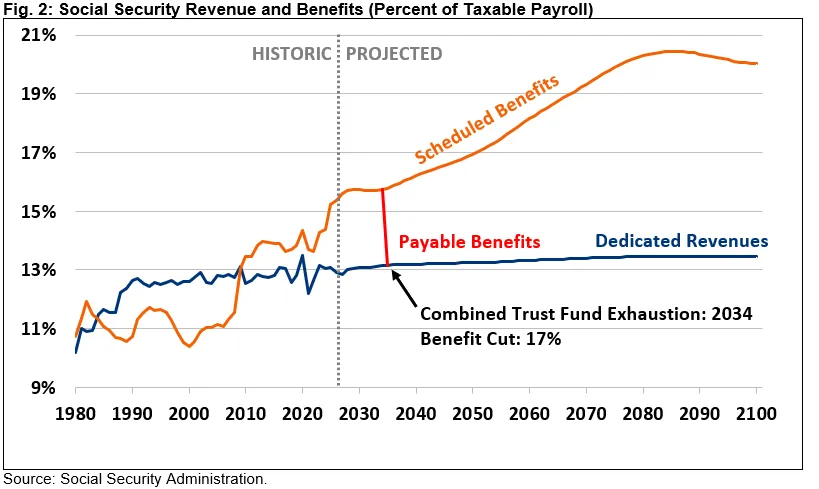

The Trustees project Social Security faces large and growing shortfalls. This year, they estimate the program faces a combined cash deficit of $270 billion. Over the next decade, Social Security will spend $3.8 trillion more than it collects, which is 2.7% of taxable payroll or 0.9% of GDP.

In the decades that follow, Social Security’s deficits will grow dramatically, rising from 2.7% of payroll (1.0% of GDP) by 2036 to 3.7% of payroll (1.3% of GDP) in 2050 and 6.6% of payroll (2.2% of GDP) by 2100.

Social Security’s growing deficits are largely the result of rising costs, which are driven by the aging of the population and the growing generosity of benefits. The program’s total costs rose from 10.4% of payroll in 2000 to 13.5% in 2010, when deficits first reemerged, and reached 15.2% in 2025. Costs are projected to rise further to 16.9% of payroll in 2050 and then to 20.0% in 2100. Meanwhile, revenues are not projected to keep pace, increasing from about 13.1% of payroll in 2025 to 13.5% in 2100.

Through 2100, the theoretically combined Social Security trust funds face an actuarial imbalance of 4.42% of payroll, or 1.5% of GDP, the largest since 1977. The shortfall is equal to $31 trillion on a present value basis, nearly the equivalent of this year’s entire GDP, according to the Trustees’ projections.

Social Security's Finances Continue to Deteriorate

Social Security’s finances have deteriorated significantly in recent years. This year’s 4.42% of payroll shortfall is the largest in nearly half a century, 16% (0.60 percentage points) larger than the 3.82% shortfall projected in the 2025 Social Security Trustees’ Report and 2.3 times as large as the shortfall projected back in 2010. The Trustees now project the OASI retirement trust fund will go insolvent in 2032, compared to 2033 in last year’s report. The theoretically combined trust fund insolvency date of 2034 is the same as last year.

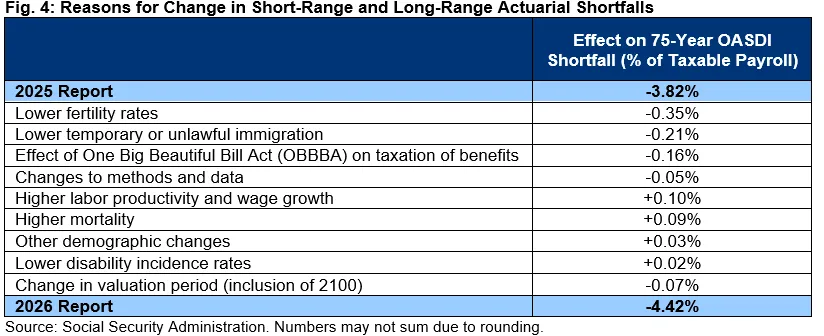

The two biggest factors behind the worsened outlook are changing demographic assumptions. Lower birth rates explain a 0.35% reduction (worsening) in the actuarial balance, mainly due to the Trustees lowering their ultimate fertility rate from 1.9 to 1.75 children per woman in light of the ongoing decline in births. Reductions in temporary or unlawfully present immigrants explains another 0.21% reduction in the actuarial balance, driven mainly from an assumption that the ultimate level of these would be 1.2 million instead of 1.35 million per year.

The third biggest factor behind the worsened outlook is the enactment of the One Big Beautiful Bill Act (OBBBA), which reduced the actuarial balance by 0.16% of payroll by reducing revenue collected from the income taxation of Social Security benefits. Lower taxation of benefits is responsible for increasing Medicare’s trust fund shortfall by 0.09% of payroll. These estimates roughly match previous projections from CRFB and the Social Security Actuary.

Four changes to methods and programmatic data reduced the actuarial balance by an additional 0.05% of payroll. The changes included: improved modeling of labor force participation by those age 75 and older, better projection of the age distribution of those eligible for aged spouse and widow(er) benefits, lower revenue from income taxation of benefits, and better projection of average benefit levels for newly-entitled workers.

Demographic assumptions were also updated to reflect recent mortality data. As a result, the Actuary now predicts higher mortality rates and fewer future beneficiaries, increasing the actuarial balance by 0.09% of payroll. Other demographic changes such as changes in lawful immigration, marriage, and divorce had a small positive effect on the 75-year imbalance, improving it by 0.03% of payroll. Expected disability incidence rates also declined slightly, improving the balance by 0.02% of payroll.

Stronger economic assumptions further improved the actuarial balance. The Trustees now expect stronger labor productivity and average earnings growth in the next decade – with real wages projected to rise 1.72% per year through 2035, as opposed to 1.44%. These changes improve the actuarial balance by 0.10% of payroll.

Finally, the new projection window worsened Social Security’s 75-year actuarial imbalance by 0.07% of payroll – thanks to adding 2100 into the 75-year window.

Notably, the deterioration of Social Security’s fiscal outlook appears entirely on the retirement trust fund. The disability insurance trust fund had a small improvement in its actuarial balance, from 0.12% of payroll to 0.13%, mainly due to new data and a change in the assumed disabled-worker incidence rates for the short term and a more gradual transition to the long-term incidence rate.

Time is Running Out to Fix Social Security

The Social Security Trustees recommend “lawmakers address the projected trust fund shortfalls in a timely way in order to phase in necessary changes gradually and give workers and beneficiaries time to adjust.”

The existing cost of delay is already very large. Reforms that would have once restored solvency – like eliminating the $184,500 payroll tax cap or re-indexing benefits with “progressive price indexing” – would now close around half of Social Security’s solvency gap.

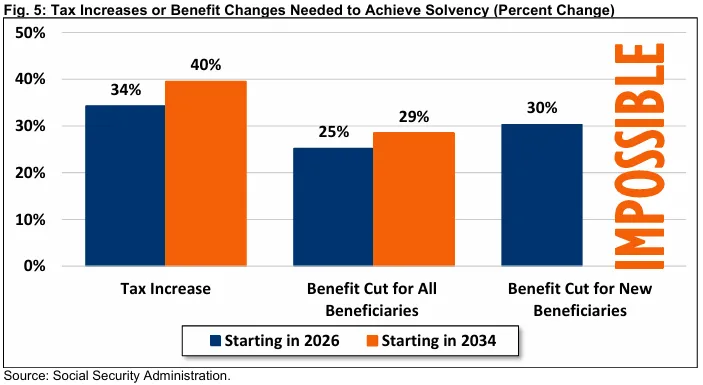

Further delay will make adjustments even more painful. Today, lawmakers could restore long-term solvency of the theoretically combined trust funds with the equivalent of a 34% (4.25 percentage point) payroll tax increase, a 25% reduction in total benefits, or a 30% reduction in benefits for new beneficiaries if they acted today. By 2034, adjustments would need to be about 15% larger – taxes would need to be raised by 40% (4.9 percentage points) or benefits cut by 29% for all beneficiaries. Changes to benefits for new beneficiaries alone would be insufficient to restore solvency to the program, even if their benefits were eliminated entirely.

Acting today can still allow adjustments to be phased in and can give workers and retirees some time to plan and adjust. Thoughtful trust fund solutions could not only prevent abrupt benefit cuts, but also strengthen retirement and disability security, promote economic growth, support productive aging, and improve the nation’s fiscal outlook. As part of our Trust Fund Solutions Initiative, we have and are continuing to publish novel, practical solutions, including a Six Figure Limit, a COLA Cap and an Employer Compensation Tax.

Conclusion

The Social Security Trustees warn that Social Security faces the largest financial imbalance since 1977 and is closer to insolvency than any time since 1983. In just six years, nearly all retirees, survivors, and dependents on Social Security will face a deep 22% benefit cut unless necessary reforms are enacted. Just half a year later, under current projections, their access to health care will be compromised by the insolvency of the Medicare Hospital Insurance trust fund.

By failing to reform Social Security and Medicare, policymakers are implicitly endorsing deep benefit and service cuts for most current and future beneficiaries. No state will be spared from these cuts.

With each year that action is delayed, the worse Social Security’s finances become, making it harder to enact reforms that avoid abrupt changes to taxes or benefits and that give workers and retirees time to plan accordingly. Many options that would have once restored solvency are no longer available. Continued inaction has the potential to take even more reforms off the table.

In the context of an insolvency date just six years away, all options – on both the revenue and benefit side of the equation – need to be on the table.

Despite the looming insolvency of its trust funds, many solutions to shore up Social Security’s finances still exist. Our own Social Security Reformer Tool allows anyone to design a plan of their own. And our Trust Fund Solutions Initiative is developing new ideas – like a Six Figure Limit or COLA Cap for Social Security and an Employer Compensation Tax for Social Security and Medicare – to help restore solvency while strengthening retirement security, bolstering economic growth, enabling healthy and productive aging, making the program more efficient, and strengthening the nation’s finances.

Policymakers should enact thoughtful Social Security reforms as soon as possible. It’s time for trust fund solutions.