Social Security Reform Can Boost Incomes, Grow the Economy

According to recent estimates from the Congressional Budget Office (CBO), restoring Social Security solvency through blunt changes could ultimately accelerate income growth by more than one-fifth. We estimate that thoughtful reforms could boost income growth by one-third over the same period, increasing average real income by roughly $10,000 per person in 2053 alone.

Under CBO's extended baseline, debt is projected to rise to 181 percent of Gross Domestic Product (GDP) by the end of Fiscal Year (FY) 2053, in part because CBO assumes that the Social Security system will borrow to continue paying benefits beyond insolvency. Under alternative projections that prevent Social Security from borrowing once its trust fund is exhausted – as required under the law – CBO projects debt would rise to 132 percent of GDP by 2053.

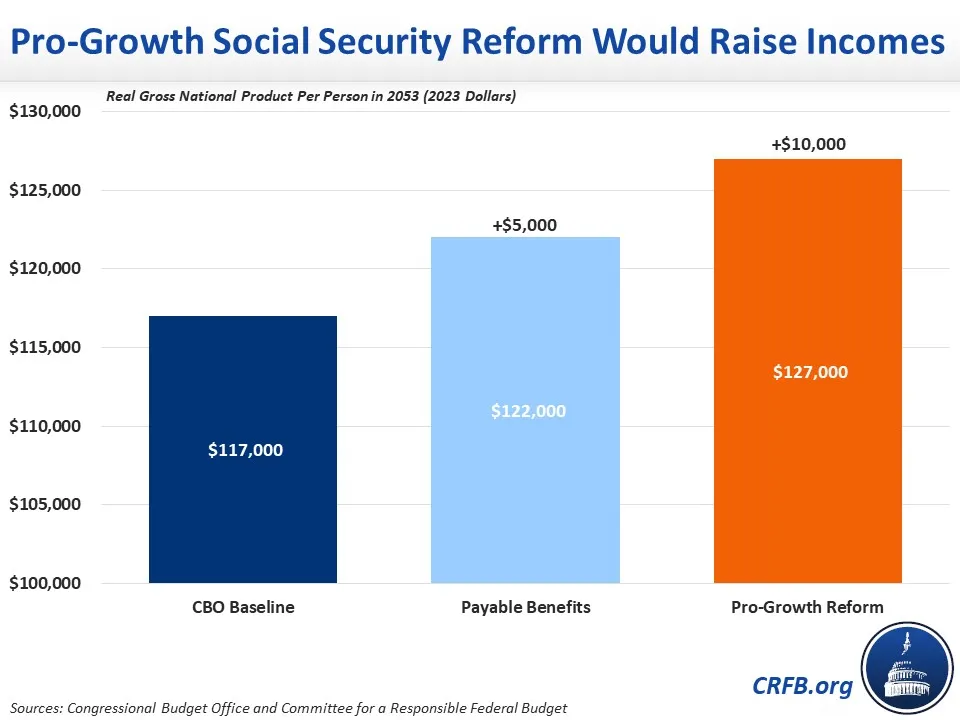

As we recently showed, allowing Social Security to run out of funds in 2033 would lead to abrupt benefit cuts, devastating many retirees and reducing benefits by over $17,000 for a typical newly retired dual-income couple. CBO estimates this cut would also reduce real economic output by about 1.2 percent in 2034. However, without the additional borrowing assumed under CBO's baseline, this scenario would slow growth of the national debt and as a result boost incomes over the long term.1 Specifically, CBO projects this scenario would boost the growth rate in average income by about one-fifth, increasing real per capita Gross National Product (GNP) to $122,000 by 2053 - $5,000 higher than the $117,000 under CBO’s baseline.

Of course, allowing a deep across-the-board cut in benefits would be the worst possible way to restore solvency. Phasing in a thoughtful combination of revenue and benefit adjustments would be more fair and better targeted, would give workers more time to plan and adjust, would avoid a one-time reduction in national income, and could do more to grow the economy over time.

We estimate a Pro-Growth Social Security Reform framework, such as the one proposed by Committee for a Responsible Federal Budget president Maya MacGuineas, senior vice president and senior policy director Marc Goldwein, and policy director Chris Towner, could boost the rate of income growth by about one-third by 2053 and generate additional growth over subsequent decades. Specifically, we estimate this approach could boost income to $127,000 per person after 30 years, a $10,000 increase over the $117,000 in CBO’s baseline.

Simply acting sooner to implement a gradual plan to secure Social Security would on its own would accelerate income growth by reducing near-term debt, giving workers more time to adjust their savings and retirement plans, and creating more security over the future of the program. Focusing adjustments on higher earners could lead to further income gains, as those earners are better equipped to save and invest more when expected benefits decline.

But a thoughtful Social Security reform plan would also have specific pro-growth elements. These elements could be part of a comprehensive plan to restore solvency and strengthen retirement security for those most at risk.

For example, carefully raising the retirement age to account for rising longevity would encourage workers to delay their retirement - bolstering labor supply, economic output, and incomes. The MacGuineas-Goldwein-Towner plan combines a proposed gradual retirement age increase with a new Poverty Protection Benefit available to all workers starting at age 62.

The plan also counts all years of a worker’s earnings equally toward benefits, instead of counting only the highest 35 years in a way that effectively weights early years of work far more heavily and excludes workers with less than ten years of work history. This change reduces the implicit tax on working more years over one’s lifetime, leading to further labor and income growth.

Other reforms, such as automatically enrolling workers in voluntary retirement accounts on top of Social Security would boost savings, leading to greater investment and stronger growth. Improvements to the payroll tax – for example, replacing the employer-side tax with a broader compensation tax – could improve efficiency and progressivity, leading to additional output gains.

Additional economic growth could be achieved by repealing the Retirement Earnings Test, improving the information provided to future beneficiaries, and expanding opportunities for workers with disabilities.

As MacGuineas, Goldwein, and Towner explained in their proposal:

Social Security is the single largest federal government program as well as the greatest source of retirement income for most seniors [and is financed with] the single largest tax paid by the majority of Americans…Social Security provides workers with powerful – though sometimes confusing – signals and incentives about how much to save, how many years to work, and when and how to retire…Pro-Growth Social Security Reform can use these signals and incentives to its advantage to support a more productive workforce and to better promote work and savings while reducing debt.

Lawmakers should act quickly to avoid Social Security’s looming insolvency and prevent a 23 percent across-the-board benefit cut. But as they develop a package of revenue and benefit adjustments, they should focus on promoting stronger economic growth and implementing smart solutions that maximize living standards for all Americans while securing Social Security for future generations. Thoughtful reforms could accelerate growth by one-third and boost average income by up to $10,000 per person.

1 According to CBO, the “payable benefits” scenario would boost long-run output (and thus per capita income) in three ways. Most significantly, lower spending would reduce budget deficits, crowding in private investment and thus accelerating economic growth. In addition, lower benefits would lead many workers to work longer and save more, boosting labor and capital and thus economic output.