Intergovernmental Transfers (IGTs) Can Inflate Federal Medicaid Matching Funds

The Medicaid program provides health insurance to roughly 70 million lower-income Americans and is jointly financed by states and the federal government.1 The federal government covers about 65% of this spending, at a cost of $668 billion in 2025 and an expected cost of $8.3 trillion over the next decade.2

States have long employed creative financing schemes to boost the amount of federal matching funds they receive, which is calculated using the Federal Medical Assistance Percentage (FMAP). One such arrangement involves making large payments to state or local government-owned health care providers, and then employing intergovernmental transfers (IGTs) that require those providers to transfer funding to the state to help pay for the state’s share of Medicaid.3 These schemes can allow states to inflate their federal funding through the FMAP, thereby increasing federal Medicaid costs.

IGTs have some similarities with provider taxes, a well-known financing mechanism restricted but not banned under the 2025 One Big Beautiful Bill Act (OBBBA).4 As states freeze or reduce their use of provider taxes, they may turn to IGT arrangements to replace these dollars.

In this brief we explain:

- How states use IGTs to fund their share of Medicaid payments;

- States’ growing use of IGTs to shift costs to the federal government, particularly for supplemental payments;

- Loopholes that allow gaming to persist; and

- Options to address financing schemes and reduce cost shifting.

With the national debt now larger than the economy and federal health care costs continuing to grow, policymakers should work to lower health care costs and rein in excessive borrowing. Continued efforts to address Medicaid financing schemes should be part of this solution. Congress should consider ways to restore the federal-state partnership and hold states accountable for federal funds. This could include limiting the use and abuse of IGTs.

IGTs Fund a Meaningful Share of Medicaid Costs

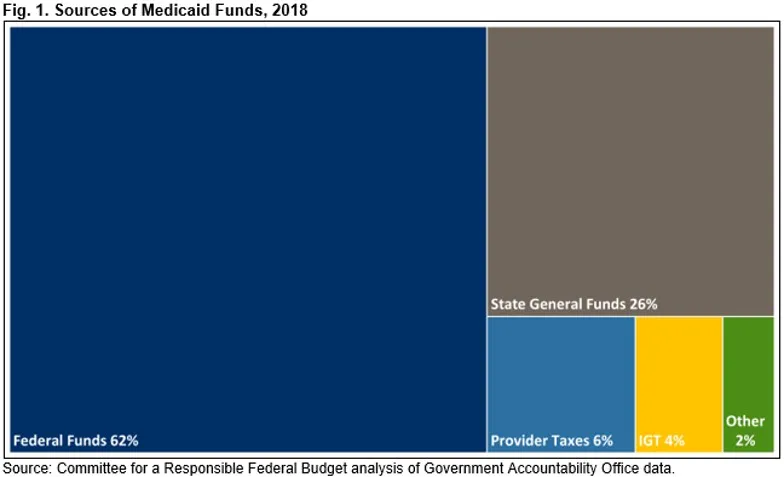

Although states are responsible for funding roughly 35% of their share of Medicaid costs, on average, only about two-thirds of that money comes from general state funds.5 Based on data from 2018, the only comprehensive data available, 16% of state Medicaid funding came from health care provider taxes (6% of total) – which we have previously explained are used to inflate federal contributions, but which face increasing restrictions under OBBBA. IGT’s made up another 10% of state Medicaid payments in 2018 (4% of total), generating $22 billion for states.6

IGTs are funds derived from government entities outside of a state government’s general fund and transferred into the Medicaid program.7 The ability to use local government revenue to fund the “nonfederal share” of Medicaid costs was established when Medicaid was created and reflects the role of local and other public funding for low-income populations that predated Medicaid coverage. IGTs can come from local governments such as counties and cities, who contribute on behalf of their residents. But often, IGTs come from hospitals, nursing facilities, or other providers owned or operated by the state or local governments.

Federal law effectively limits the amount of funds states can raise via IGTs by requiring that at least 40% of the state’s Medicaid share come from state-imposed sources – including from state general funds or provider taxes. This means that up to 60% of the nonfederal share may come from IGTs and other sources, though no state comes close to this limit.8 At the high end, IGTs make up 30% of New York’s nonfederal share of the Medicaid program and 28% of Indiana’s. Ten states, including New Jersey and Connecticut, don’t use any IGTs to fund Medicaid.

IGTs Fund Supplemental Payments

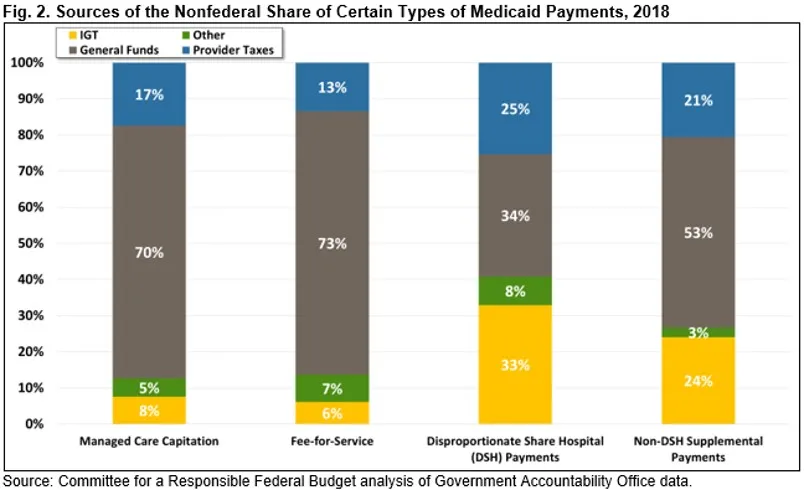

In recent years, Medicaid supplemental payments – lump-sum payments to providers on top of direct payment for services – have become increasingly costly without corresponding improvements in access to services, provider capacity, or care quality. Although IGTs can be used to finance any Medicaid payments or the program as a whole, they are mainly used to cover supplemental payments.

While 6% of the nonfederal share of fee-for-service payments came from IGTs, IGTs funded 33% of one type of supplemental payment called Disproportionate Share Hospital (DSH) payments and 24% of non-DSH supplemental payments. In some cases, IGTs fund most of the nonfederal share of supplemental payments. For example, Minnesota used $43 million in IGTs to make $100 million worth of non-DSH supplemental payments in 2018 – enough for the federal government to cover the remaining cost with no state tax dollars.

Although data is limited, it is clear that IGT use is growing. The number of state directed payments (SDPs) funded in whole or part with IGTs more than doubled, from 42 to 96 SDPs between 2020 and 2024, while SDPs themselves have grown five-fold.9 Unfortunately, we do not know exactly how much IGTs have grown because states do not report how they fund the nonfederal share of Medicaid payments. In fact, nearly all of the comprehensive data on funding IGTs comes from a single survey of states conducted by the Government Accountability Office (GAO) in 2018.10 The Centers for Medicare & Medicaid Services (CMS) and other oversight entities lack transparent data that could hold states accountable for the required mix of funding sources.

States Use IGTs to Inflate their Federal Match

Although the FMAP formula establishes a specific formula for federal Medicaid funding – covering 50% to 77% of most costs for the base (non-expansion) population and 90% of costs for those covered under the Affordable Care Act – state governments have found ways to inflate their effective federal match.11 One well-known tactic involves increasing payments to providers and then using provider taxes to recover much of the funds while reporting a higher total cost to the federal government. States often use IGTs in a similar way to increase the amount of federal Medicaid funds they receive relative to state and local funds.

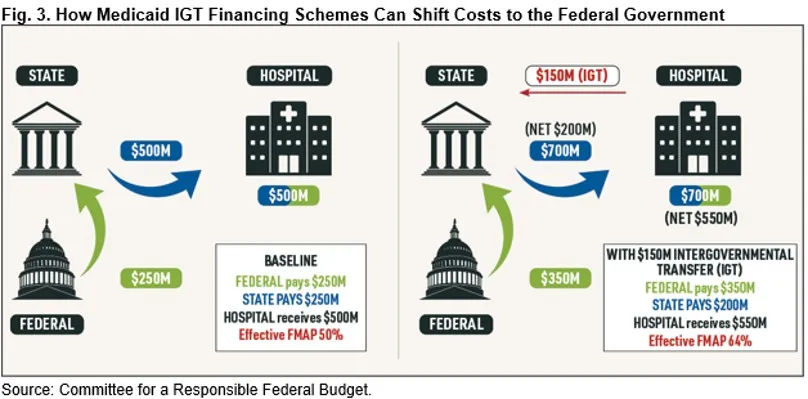

Under this IGT arrangement, state and local government entities such as public hospitals or nursing facilities first transfer funds to the state. The state then returns these funds to the same providers in the form of higher Medicaid payments, and reports the payments to the federal government in order to receive a higher federal match. In this way, states can either reduce their net Medicaid payments or increase payments to providers without incurring further costs.

Government hospitals and other providers are amenable to paying IGTs because they are confident that they will receive at least as much back, if not more, in return from the state. Unlike for provider taxes, federal statutes do not prohibit the states from guaranteeing these “hold harmless” arrangements using IGTs.12

This scheme is most effective at achieving the hold harmless outcome – and most lucrative for states and providers – when the state makes supplemental payments. In practice, many supplemental payments are paid based on the providers’ ability to raise the nonfederal share, via provider taxes (for private providers) or IGTs (for providers owned by local governments). In contrast, when IGTs are used for base payments distributed to all providers in the Medicaid program, it becomes much more challenging to ensure providers are held harmless.

States Often Circumvent Rules Meant to Avoid Holding Providers Harmless

Using IGTs, states find creative ways to circumvent, strain, or even violate laws meant to limit direct hold harmless arrangements that apply elsewhere. These schemes are often designed to get around federal limits to provider taxes: states can only impose taxes on private hospitals effectively up to 6% of patient revenue. But IGTs from public providers have no limit. So, states facilitate ways to make private providers look like public ones.

Some types of IGT schemes are prohibited under current law. For example, private hospitals are not allowed to donate a significant amount of funds to public hospitals to facilitate effective hold harmless relationships.13 Under such a scheme, the public hospital would transfer the funds via IGT to the state for the nonfederal share. The state pays the private hospitals a supplemental payment and then seeks reimbursement from the federal government at the state’s FMAP rate. This scheme is illegal because the private donations are considered “non-bona fide donations.”14 This prohibition is in place precisely to avoid holding private providers harmless for their contributions to the nonfederal share. However, states have sought potential workarounds.

Providers have come up with two main ways to mask non-bona fide provider donations as the source of the IGTs. Some states artificially expand the number of government-owned providers through complex agreements with private entities. For example, in Indiana, hundreds of private nursing homes entered into ownership and/or operating agreements with county hospitals that allowed them to participate in the state’s Non-State Governmental Organization (NSGO) supplemental payment program funded with IGTs.15 This allows essentially private entities to transfer funds as IGTs (rather than illegal non-bona fide donations) to fund supplemental payments.

Other states take advantage of non-bona fide donation rules. Specifically, private hospitals create non-profit entities that reach agreements with local governments to assume the costs of health care services that the local governments previously purchased. The local government monies freed up under these agreements are then used as local government IGTs to fund the non-federal share of supplemental payments to the private providers. See the Appendix for more examples.

While CMS has found the above schemes illegal, a recent court decision may expand allowable IGT schemes. In September 2025, a federal court ruled in favor of the state of Texas, finding that its IGT arrangements were permissible.16 Local governments taxed private hospitals and then IGT’d the funds to the state for the nonfederal share. Afterwards, the private hospitals were paid supplemental payments. The hospitals then pooled the supplemental payments together and redistributed them to each other in proportion to each’s contributions, ensuring each hospital received their IGT’d-tax funds back.

This complex arrangement avoided the limit on provider taxes by using IGTs. CMS argued that the state should prevent these arrangements because it violates the statutory prohibition on holding providers harmless.17 But the court disagreed, vacating CMS’ regulation prohibiting pooling, saying CMS can only regulate how the state handles federal funds; in the Texas case, it was local hospitals that were creating the hold harmless.18

Restricting IGTs Could Reduce Federal Costs and State Gaming

The One Big Beautiful Bill Act (OBBBA) took positive steps toward reducing provider tax financing gimmicks that shift costs to the federal government, but policymakers could do more to limit problematic IGT arrangements and restore the Medicaid federal-state partnership. Importantly, some IGTs represent legitimate burden-sharing between state and local governments; thoughtful reforms would continue to allow these IGTs while restricting others.

The lack of data on financing makes it difficult to estimate the savings to the federal government that may accrue under various proposals. However, a number of options have been put forward over the years that could reduce the incidence of states holding providers harmless for IGTs and reduce gaming through non-bona fide donations. Some options include:

- Curtail Non-Bona Fide Donations. Policymakers should curtail states’ gaming that allows private providers to pose as public ones to make IGTs, avoiding limits on provider taxes and masking non-bona fide donations. CMS’s 2019 Medicaid Fiscal Accountability Regulation (MFAR), which was proposed but never finalized, included several reforms that could be revived by CMS or codified by Congress.19 As outlined in MFAR, to limit the abuse of IGTs through non-bona fide donations, policymakers could limit IGTs to public funds only (e.g., funds appropriated from the state to a teaching hospital or other state entity; or, local funds that come from state or local taxes), not funds transmitted from private providers. In this way, funds that come from a private nursing facility, for example, would be excluded. They could also give CMS more authority to evaluate IGTs’ circumstances to ensure the true source is not a non-bona fide donation.

- Limit Providers’ Ability to Redistribute Medicaid Funds. The federal court decision in favor of Texas’s IGT arrangements undermines CMS’ oversight. It allows providers to pool and redistribute supplemental payments paid for with IGTs to ensure every provider is held harmless. CMS should be able to restrict supplemental payments to states that allow providers to hold harmless the contributing providers. Allowing this to continue invites private providers to masquerade as public ones. Congress could clarify in statute that such pooling and redistribution of Medicaid funds is not allowed.20

- Restrict Medicaid Payment Rates to Public Providers. To extract additional federal dollars, IGTs from government-owned or affiliated hospitals or nursing homes are generally coupled with higher payment rates to those same health providers. The use of this circular financing scheme could be curtailed or in some cases prevented by limiting payments that can be made to public entities that participate in IGTs.21 One option – proposed by CMS in 2007 and later vacated by the courts for procedural reasons – is to cap payments to IGT-eligible providers to the cost of caring for Medicaid patients.22 A second alternative would be to require that payments to public and private providers should be the same for the same services – removing the potential additional spending to government-owned facilities used to boost the federal match.23

- Place a Moratorium on New IGTs. OBBBA imposed a moratorium on imposing new provider taxes or increasing existing ones. Although this moratorium may encourage states to instead expand their reliance on IGTs, it also provides a model for how to avoid such a cost-shift. Congress could simply place a moratorium on new or increased IGTs nationwide. To better target such restrictions, Congress could freeze IGTs that are used for supplemental payments.

- Restrict Use of IGTs for Supplemental Payments. Federal law requires states to use general funds to fund at least 40% of the state’s share of Medicaid payments (including provider taxes), allowing up to 60% to come from other sources such as IGTs.24 The law does not specify that all payments should reflect that mix, and instead applies to the total. This allows states to aggressively use IGTs in some circumstance – for example, CMS recently approved Missouri’s application for a supplemental payment for hospitals funded exclusively by IGTs.25 To reduce the use of IGTs that shift costs to the federal government, policymakers could increase the required portion of the nonfederal share that comes from general funds. Congress could also require that the “mix” of nonfederal share sources apply equally to supplemental payments and base payments alike.26

- Improve Reporting of the Source of the State Medicaid Share. Regardless of whether new IGT restrictions are enacted, financing transparency is long overdue. CMS lacks data showing what mix of funding sources make up the nonfederal share for different types of payments. The persistent lack of data makes it difficult for CMS and policymakers to understand the prevalence, scope, and growth of financing arrangements and adaptations states make to respond to restrictions and take advantage of additional loopholes. The lack of transparency also makes it difficult to enforce existing limits and develop and enforce new policies. In MFAR, CMS proposed reporting requirements on the source of the nonfederal share, but MFAR was withdrawn in 2020.27

Although we are not able to provide formal estimates of these options without better data, they could potentially save tens or hundreds of billions of dollars over a decade. In 2008, the Congressional Budget Office (CBO) estimated that a rule to restrict IGT payments to public providers would save $22 billion over a decade.28 This would be the equivalent of more than $50 billion today if savings were a constant share of Medicaid, and is likely to save much more given the growth in IGTs and supplemental payments. As another datapoint, requiring states to use general funds for at least 40% of the nonfederal share of supplemental payments – as opposed to 40% of all payments across the state – could save in the neighborhood of $200 billion or more.29

In combination with other reforms, restricting IGTs could help to meaningfully lower federal health care spending, improve fairness with the states, and reduce budget deficits.

Conclusion

OBBBA made important changes to financing Medicaid using provider taxes, but it did not address states’ creative use of IGTs. As provider taxes decline starting in 2027, states may look for new ways to fund Medicaid payments without increasing state contributions. Between the lack of restrictions on IGTs and the documented use of IGTs to creatively increase federal Medicaid spending through legal and illegal financing schemes, states may try to replace some lost provider tax revenues with IGTs.

While frequently used simply to fund base payments, states creatively use IGTs to abuse the broad federal rules and generate tens of billions in federal funding annually. Federal action is needed to implement common sense steps to tighten rules that different administrations have identified as needed and curtail state efforts to increase federal matching funds without a commensurate increase in state funds.

Without further action from Congress, the long history of state financing schemes and growing use of supplemental payments suggests that restrictions in one area can spur additional gaming in another area. Tighter restrictions are needed to better ensure states and the federal government share in Medicaid costs and that circular financing and payment schemes end. Equally important are reporting requirements to improve the transparency of state financing and payment arrangements, as data is the key to effective oversight, enforcement, and identifying where new policies are needed.

Appendix: Examples of States Gaming Rules on Bona Fide Provider Donations

As described above, some states try to avoid limits on provider taxes by taking advantage of IGT rules. They do this by artificially expanding the number of government-owned providers. However, these schemes usually violate rules that prohibit private providers from making non-bona fide donations to fund the federal share.

- Utah applies a designation “nonstate government entities” (NSGE) – which usually refers to entities like city hospitals – to switch a nursing home’s ownership status from private to local government.30 One audit found that a community hospital acquired the licenses via contract of 40 nursing homes located throughout the state, despite neither owning nor operating the facilities.31 Instead, the prior nursing home administrators operate the nursing homes per the contract. Utah uses no state general funds to finance the supplemental payments to the nursing homes, but rather the community hospital uses an IGT to transfer “public funds” to cover the nonfederal share. The funds are returned to the nursing homes via a supplemental payment, which is not linked to the Medicaid services provided. One study found that the non-DSH supplemental payments resulted in payments exceeding nursing homes costs on average by 25%.32

- Texas also established an NSGE to collect funds from “local government” nursing homes to fund IGTs. An audit identified several concerns including: nursing homes using bank promissory notes and lines of credit to fund their IGT contributions; nursing homes not receiving all of the supplemental payments; and supplemental payments made to nursing homes that do not meet required quality improvement goals.33

Some states develop complex private-public partnerships to obscure donations that expand IGT use.

- In Texas, CMS disallowed over $25 million in federal funds after finding that private hospitals assumed costs previously paid by public health districts and in return received supplemental payments that held the private hospitals harmless for the costs they incurred. CMS found that the IGTs were funded with non-bona fide provider donations.34

- A federal audit of one private-public partnership in Texas found that $146.6 million (or 77% of the total non-federal share) transferred as IGTs were non-bona fide donations.35 Specifically, private hospitals created a non-profit entity and assumed costs of health care services previously incurred by local governments, effectively donating the care. In return, the hospitals received supplemental payments that exceeded their costs, effectively holding them harmless for the costs of care, making the donation impermissible.

1 Centers for Medicare & Medicaid Services (CMS), “February 2026: Medicaid & CHIP Eligibility Operations and Enrollment Snapshot,” https://www.medicaid.gov/resources-for-states/downloads/eligib-oper-and-enrol-snap-feb2026.pdf.

2 Percent of Medicaid costs contributed by federal government computed by Committee for Responsible Federal Budget (CRFB) using data from the Medicaid and CHIP Payment and Access Commission (MACPAC), “EXHIBIT 16. Medicaid Spending by State, Category, and Source of Funds, FY 2024,” https://www.macpac.gov/macstats/program-enrollment-and-spending/; cost projections based on Congressional Budget Office(CBO), “The Budget and Economic Outlook: 2026 to 2036,” https://www.cbo.gov/publication/61882.

3 Federal policy requires that intergovernmental transfers occur before the state makes a Medicaid payment to the provider and that the amount of the transfer cannot be greater than the nonfederal share of the Medicaid payment amount.

4 See Sec. 71115 and Sec. 71116: One Big Beautiful Bill Act, H.R. 1, 119th Congress, 2025, https://www.congress.gov/bill/119th-congress/house-bill/1. In total, $190 billion in savings is projected from reducing provider taxes and $150 billion from limiting state directed Medicaid payment limits through 2034. See CBO, “Estimated Budgetary Effects of an Amendment in the Nature of a Substitute to H.R. 1, the One Big Beautiful Bill Act, Relative to CBO‘s January 2025 Baseline,“ June 29, 2025, https://www.cbo.gov/publication/61534.

5 Government Accountability Office (GAO), “Medicaid: CMS Needs More Information on States’ Financing and Payment Arrangements to Improve Oversight,” GAO-21-98, Washington, DC, December 2020, https://www.gao.gov/products/gao-21-98. CMS issued a rule in 2024 to this effect. Federal Register, Department of Health and Human Services (HHS), CMS, “Medicaid Program; Medicaid and Children’s Health Insurance Program (CHIP) Manage Care Access, Finance, and Quality,” 42 CFR Parts 430, 438, and 457, May 10, 2024 https://www.federalregister.gov/documents/2024/05/10/2024-08085/medicaid-program-medicaid-and-childrens-health-insurance-program-chip-managed-care-access-finance. The 2024 managed care rule followed a separate attempt by CMS to restrict states from implementing this kind of hold harmless arrangement. In 2019, CMS proposed the Medicaid Financial Accountability Regulation (MFAR), which would have required providers to retain the funds they were paid. CMS withdrew this proposed rule in 2020 after significant opposition.

6 GAO, “Medicaid: CMS Needs More Information on States’ Financing and Payment Arrangements to Improve Oversight,” GAO-21-98, Washington, DC, December 2020, https://www.gao.gov/products/gao-21-98.

7 Federal statute prohibits the restriction of the use of IGTs when such funds are derived from state or local tax revenue and transferred to the Medicaid agency. Social Security Act, Pub. L. No. 117–2, § 9813, 135 Stat. 213, https://www.law.cornell.edu/uscode/text/42/1396w-6; as implemented by 42 CFR Part 433.51, https://www.ecfr.gov/current/title-42/chapter-IV/subchapter-C/part-433/subpart-B/section-433.51.

8 The other large source of local government financing is from certified public expenditures (CPEs), which made up about 2% of the nonfederal share in 2018, the most recent data available. See GAO, “Medicaid: CMS Needs More Information on States’ Financing and Payment Arrangements to Improve Oversight,” GAO-21-98, Washington, DC, December 2020, https://www.gao.gov/products/gao-21-98. See also Kaiser Family Foundation (KFF), “Medicaid Financing Issues: Intergovernmental Transfers and Fiscal Integrity,” February 2005, https://www.kff.org/wp-content/uploads/2013/01/medicaid-financing-issues-intergovernmental-transfers-and-fiscal-integrity-fact-sheet.pdf.

9 See MACPAC, “Directed Payments in Medicaid Managed Care,” October 2024, https://www.macpac.gov/wp-content/uploads/2024/10/Directed-Payments-in-Medicaid-Managed-Care.pdf, MACPAC, “Directed Payments in Medicaid Managed Care,” June 2022, https://www.macpac.gov/wp-content/uploads/2022/06/June-2022-Directed-Payments-Issue-Brief-FINAL.pdf and CMS, “CMS Issues Guidance to Strengthen Oversight of Medicaid State Directed Payments,” September 9, 2025, https://www.cms.gov/newsroom/press-releases/cms-issues-guidance-strengthen-oversight-medicaid-state-directed-payments. The One Big Beautiful Bill Act (OBBBA) restricts new SDPs to the amount Medicare pays in states that have adopted the Affordable Care Act Medicaid expansion and to 110% of Medicare in other states. For existing SDPs, these caps are phased in over time. See Sec. 71116: One Big Beautiful Bill Act, H.R. 1, 119th Congress, 2025 https://www.congress.gov/bill/119th-congress/house-bill/1.

10 GAO, “Medicaid: CMS Needs More Information on States’ Financing and Payment Arrangements to Improve Oversight,” GAO-21-98, Washington, DC, December 2020, https://www.gao.gov/products/gao-21-98.

11 77% represents the maximum “regular” FMAP for the 50 states and District of Columbia. The FMAP for U.S. overseas territories is set in statute at 83%.

12 The One Big Beautiful Bill Act (OBBBA) restricts states from increasing their provider taxes or enacting any new provider taxes. See CRFB, “Energy & Commerce Draft Would Help Limit Medicaid Gaming,” May 12, 2025, https://www.crfb.org/blogs/energy-commerce-draft-would-help-limit-medicaid-gaming.

13 If the entity donating funds subsequently receives a Medicaid payment that covers or exceeds the cost of the donation, it is being held harmless. Federal law prohibits donations to fund the state share of Medicaid costs if the entities donating the funds are directly or indirectly held harmless for the cost of the donation. Individual providers can donate up to $5,000 per year and health care organizations can donate up to $50,000.

14 States’ use of funds from private providers to fund local government IGTs have come to light through whistleblower reports that resulted in U.S. Department of Justice (DOJ) investigations and settlements. See for example, DOJ, “Florida’s BayCare Health System and Hospital Affiliates Agree to Pay $20 Million to Settle False Claims Act Allegations Relating to Impermissible Medicaid Donations,” April 6, 2022, https://www.justice.gov/archives/opa/pr/florida-s-baycare-health-system-and-hospital-affiliates-agree-pay-20-million-settle-false.

15 The billions in additional supplemental payments did not result in improved quality or increased spending on patient care. A 2023 study found that nursing homes only received a fraction of the total supplemental payments. Further, while non-state governmental organization (NSGO) nursing homes increased spending on administrative costs and on equipment purchases, spending on clinical services declined. Sharma, Hari and Lili Xu, “Use of Intergovernmental Transfers-based Medicaid Supplemental Payments to Boost Nursing Home Finances: Evidence From Indiana Nursing Homes,” Medical Care 61, no. 8 (2023): 546-553, https://pmc.ncbi.nlm.nih.gov/articles/PMC10330393/.

16 State of Texas, et al. v. CMS, et al, Case No. 6:23-cv-161-JDK, United States District Court for The Eastern District of Texas, Tyler Division, September 24, 2025, https://www.texasattorneygeneral.gov/sites/default/files/images/press/CMS_MSJ_Order%20and%20Opinion.pdf.

17 CMS issued a rule in 2024 to this effect. Federal Register, HHS, CMS, “Medicaid Program; Medicaid and Children’s Health Insurance Program (CHIP) Manage Care Access, Finance, and Quality,” 42 CFR Parts 430, 438, and 457, May 10, 2024 https://www.federalregister.gov/documents/2024/05/10/2024-08085/medicaid-program-medicaid-and-childrens-health-insurance-program-chip-managed-care-access-finance. The 2024 managed care rule followed a separate attempt by CMS to restrict states from implementing this kind of hold harmless arrangement. In 2019, CMS proposed the Medicaid Financial Accountability Regulation (MFAR), which would have required providers to retain the funds they were paid. CMS withdrew this proposed rule in 2020 after significant opposition.

18 While the case involved a CMS decision in Texas, the court action enjoined CMS provisions and policies for all state Medicaid programs. See Texas, et al v. CMS, et al, Case No. 6:23-cv-161-JDK, United States District Court for The Eastern District of Texas, Tyler Division, September 24, 2025 https://www.texasattorneygeneral.gov/sites/default/files/images/press/CMS_MSJ_Order%20and%20Opinion.pdf.

19 Federal Register, HHS, CMS, “Medicaid Program; Medicaid Fiscal Accountability Regulation,” 42 CFR Parts 430, 433, 447, 455, and 457, November 18, 2019, https://www.federalregister.gov/documents/2019/11/18/2019-24763/medicaid-program-medicaid-fiscal-accountability-regulation.

20 This policy would also apply to payments that were funded through provider taxes.

21 OBBBA limited SDPs to the amount that Medicare would pay for the same services in most states, and CMS recently proposed a rule that would implement this cap for SDPs as well as other providers, such as clinicians. See Sec. 71116: One Big Beautiful Bill Act, H.R. 1, 119th Congress, 2025, https://www.congress.gov/bill/119th-congress/house-bill/1 and Federal Register, HHS, CMS, “Medicaid Program; Medicaid Managed Care State Directed Payments and Medicaid Fee-for-Service Targeted Medicaid Practitioner Payments,” 42 CFR Parts 438, and 447, May 22, 2026 https://www.federalregister.gov/documents/2026/05/22/2026-10292/medicaid-program-medicaid-managed-care-state-directed-payments-and-medicaid-fee-for-service-targeted.

22 In 2007, CMS finalized a rule that would have: limited reimbursement of government-owned providers to cost of treating Medicaid patients, which would have decreased the incentive to fund supplemental payments; redefine “unit of government” to apply only to entities with taxing authority; and require providers to retain payments rather than pool and redistribute them to hold entities harmless. However, Congress put a moratorium on the rule through May 2008 which was later extended to April 2009. Furthermore, in 2008, a federal judge vacated the rule in response to a lawsuit brought by a coalition of provider groups, saying that the rule was “improperly promulgated.” Finally, in 2009 Congress issued a “Sense of the Congress” that the Secretary of Health and Human Services should not promulgate a final rule on cost limits on public providers.

23 Medrano, Chris, Brian Blase, and Kip Piper, “The Local Loop: How States Turn Medicaid into a Government Provider Payday Scheme,” Paragon Institute, December 15, 2025, https://paragoninstitute.org/medicaid/the-local-loop-how-states-turn-medicaid-into-a-government-provider-payday-scheme/.

24 Federal laws consider provider taxes to be “general funds” for purposes of these calculations.

25 CMS, April 2026, https://www.medicaid.gov/medicaid/managed-care/downloads/MO_VBP_IPH.OPH3_New_20250701-20260630_0.pdf.

26 Under federal law state general funds must represent at least 40% of the nonfederal share of state Medicaid payments, and funds derived from local governments can represent up to 60% of state Medicaid payments. See CRFB, “Supplemental Payments Drive Up Federal Medicaid Costs,” February 1, 2024, https://www.crfb.org/papers/supplemental-payments-drive-federal-medicaid-costs.

27 Federal Register, HHS, CMS, “Medicaid Program; Medicaid Fiscal Accountability Regulation,” 42 CFR Parts 430, 433, 447, 455, and 457, November 18, 2019, https://www.federalregister.gov/documents/2019/11/18/2019-24763/medicaid-program-medicaid-fiscal-accountability-regulation.

28 CBO, “Medicare, Medicaid, and SCHIP Administrative Actions Reflected In CBO’s Baseline,” March 2008, https://www.cbo.gov/system/files/2018-09/42515_medicaremedicaid.pdf.

29 In 2024 we estimated applying this policy to the nonfederal share of each type of payment would save over $440 billion over a decade. Those estimates would differ significantly today due to changes in the Medicaid law under OBBBA, differences in the budget window, and other differences in the baseline. See CRFB, “Supplemental Payments Drive Up Federal Medicaid Costs,” February 1, 2024, https://www.crfb.org/papers/supplemental-payments-drive-federal-medicaid-costs.

30 Per Utah’s approved Medicaid plan, a nursing home that is owned by NSGE can receive Medicaid supplemental payments made to nonstate government owned nursing homes. Utah Department of Health and Human Services, July 2024, https://medicaid-documents.dhhs.utah.gov/stateplan/spa/A_4-19-D.pdf.

31 Office of the Legislative Auditor General, “Report to the Utah Legislature: A Performance Audit of Beaver Valley Hospital’s Medicaid Upper Payment Limit Program (For Nursing facilities),” October 2017, https://le.utah.gov/interim/2017/pdf/00004449.pdf.

32 The amount sent to the hospital consist of two components: (1) “seed money” which represents the state share of the supplemental payment and (2) amounts to cover an “administrative fee.” In total, the amount of the IGT represents 51% of the total non-DSH supplemental payments. After the nursing homes receive their supplemental payments, they return the “seed money” and “administrative fee” amounts to the county hospital. According to the auditors’ report the amount of the seed money returned to the hospital is used as seed money for future non-DSH supplemental payment and the amount of the administrative fee is used by the community hospital. The state’s arrangement raises concerns about noncompliance with Medicaid policy, including requirements that, IGTs are supposed to be funded with public funds and cannot be funded with federal funds; providers are required retain the payments they receive; and federal Medicaid matching funds are available for Medicaid services provided to Medicaid patients, as such “seed money” and “administrative fees” are not Medicaid benefits. Utah Department of Health & Human Services Office of Reimbursement, Coordinated Care & Audit, “Medicaid Reimbursement Rate Comparative Analysis – Nursing and Intermediate Care Facilities,” May 2025, https://medicaid-documents.dhhs.utah.gov/stateplan%2Fprr%2F2025%2F10+-+NF+and+ICF_FINAL_05.30.2025.pdf and Office of the Legislative Auditor General, “Report to the Utah Legislature: A Performance Audit of Beaver Valley Hospital’s Medicaid Upper Payment Limit Program (For Nursing facilities),” October 2017, https://le.utah.gov/interim/2017/pdf/00004449.pdf.

33 HHS Office of Inspector General (OIG), “Texas’ Quality Incentive Payment Program Raises Questions About Its Ability To Promote Economy and Efficiency in the Medicaid Program,” December 2020, https://oig.hhs.gov/documents/audit/8248/A-06-18-07001-Complete%20Report.pdf. The audit reviewed judgmental sample nursing facilities that received supplemental payment. Eight local government nursing homes were selected—one each from a judgmental sample of 8 non-state government entities that owned 96 individual local government nursing homes.

34 Department of Health and Human Services, Departmental Appeals Board, Appellate Division, “Texas Health and Human Services Commission, Docket No. A-17-51, Decisions No. 28886,” August 7, 2018, https://www.hhs.gov/sites/default/files/board-dab-2886.pdf.

35 HHS OIG, “Texas Relied on Impermissible Provider-Related Donations To fund the State Share of the Medicaid Delivery System Reform Incentive Payment Program,” August 2020, https://oig.hhs.gov/reports/all/2020/texas-relied-on-impermissible-provider-related-donations-to-fund-the-state-share-of-the-medicaid-delivery-system-reform-incentive-payment-program/.

Tags

What's Next

-

Image

-

Image

-

Image