Break Glass: A Plan for the Next Economic Shock

The U.S. has never experienced an economic shock as indebted as we are today.

Recessions and other economic shocks are inevitable. Although the timing and particulars of the next downturn or emergency are hard to anticipate, one can predict with certainty that another will occur eventually. In almost any case, the shock and response will worsen the nation’s already unsustainable fiscal situation.

Unfortunately, the U.S. has far less capacity to address the next shock than it has previously. The national debt increased by a combined 65% of Gross Domestic Product (GDP) over the past two recessions and recoveries, with the federal government entering them with debt at 35% and 80% of GDP, respectively. Today, debt totals 100% of GDP – only a few percentage points from the previous record set after World War II. This situation leaves the U.S. immensely vulnerable.

In light of this precarious fiscal situation, policymakers should act carefully and judiciously when the next shock occurs. Too often, lawmakers wait for the emergency to happen before thinking through how they might react. Then, once the economy recovers, they move on. These crisis-driven responses can be costly and haphazard and, in some cases, may solve one problem while creating another.

To help guide thinking in the moment, lawmakers should prepare a Break Glass Plan that is ready to deploy when the time comes. Such a plan could include:

- A Highly Targeted, Near-Term Policy Response tailored to the specific nature of the shock, borrowing only if it is necessary to support a recovery.

- A longer-term package of Bipartisan Offsets that would generate $2 of medium-term savings for every $1 of near-term deficit increase.

- A Default Deficit Reduction Mechanism to freeze the indexing of most spending and tax parameters, hold appropriations levels flat, and phase in a “Deficit Reduction Surtax” to put the deficit on a glide path to 3% of GDP.

- A Bipartisan Fiscal Commission charged with replacing the default deficit reduction mechanism with more carefully thought-out and tailored measures that achieve at least as much long-term deficit reduction.

Whether rising debt is the source or symptom of the next shock, a thoughtful response should include solutions that reduce deficits and stabilize the debt to reassure markets and buttress economic resilience for households.

The Next Economic Shock Could Come at Any Time

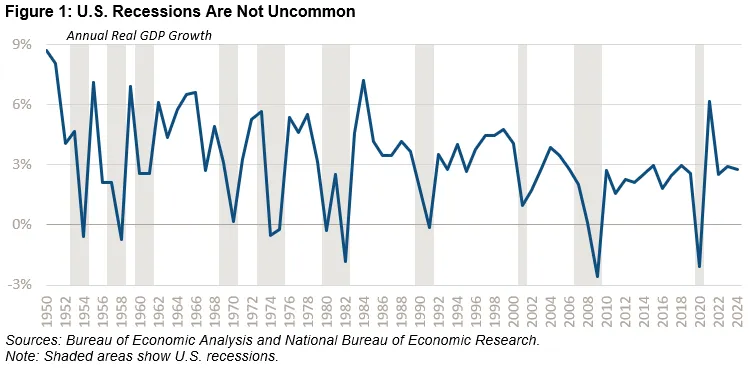

An economic shock, such as a recession, could be sparked by any number of factors. Since 1950, the United States has experienced 11 recessions of various depths and durations – an average of one every 7 years. While predicting when the next one will happen is nearly impossible, we can and should be better prepared. Some events that could spark an economic shock include:

- The popping of an asset “bubble,” such as real estate, equities, AI, or digital assets

- An unexpected loss of consumer confidence and fall in demand

- A supply shock caused by policy choices or external issues

- Fiscal or monetary policy error, especially in trying to manage a “stagflation” scenario

- Failure of financial institutions, as we saw notably in 2008 and to a lesser degree in 2023

- De-anchoring of inflation expectations and loss of confidence in the Federal Reserve

- A fiscal crisis caused by Treasury market turmoil, panic over high levels of debt, a decline in the dollar, or underlying structural risks (see our recent paper here)

- Other black swan events, such as a natural disaster, war, or collapse of a major industry

The appropriate response to the next crisis will depend heavily on the nature of the crisis. It is important to consider whether an economic shock is demand- or supply-driven, whether the cause is exogenous or endogenous, whether interest rates are high or low, whether the labor market is weak or strong, whether prices are stable or rising, and whether the U.S. government is viewed as a credible borrower.

At the same time, even very different economic shocks have historically had many commonalities. For instance, most are accompanied by contractions in real GDP, high joblessness, losses in real income, damage across several sectors of the economy, increased poverty, and reduced standards of living for many ordinary households.

The U.S. Is Not Prepared for the Next Economic Shock

Crafting the appropriate policy response for the next shock is challenging in the best of times and made especially difficult in the context of large structural deficits, high levels of debt, elevated interest rates, and ongoing inflationary pressure – all of which we have now.

In the past, the government’s responses to economic downturns have left us in a worse fiscal position. For instance, debt held by the public rose by roughly 20% of GDP during the COVID-19 pandemic and by roughly 35% over the course of the Great Recession.

While increased borrowing in response to an economic shock is often justified, it should be followed by an effort to reduce borrowing and debt levels after the shock has subsided. Unfortunately, policymakers have tended to do the opposite and have simply continued borrowing at elevated levels. As a result, our nation is in a worse fiscal position today than it has ever been going into any kind of economic downturn or emergency.

When the COVID-19 pandemic hit, debt was 79% of GDP and the deficit was 4.6% of GDP. Entering the Great Recession, debt totaled 35% of GDP and deficits 1.1%. Before the dot-com bubble burst, debt was a similar 34% of GDP and the country was running annual surpluses. In all three cases, interest consumed about one-tenth of all federal revenue.

Today, debt is roughly 100% of GDP, deficits are near 6% of GDP, and interest consumes almost one-fifth of federal revenue. Inflation also remains elevated above target at around 3%, and long-term Treasury yields remain high by recent standards – over 4% for ten-year notes and approaching 5% for the 30-year bond.

The U.S. has never entered an economic downturn or other emergency as indebted as it is today, with deficits as large as they are today, or with as little fiscal space as we have today.

Our dismal fiscal outlook, in combination with lingering inflationary pressures and ongoing Treasury market volatility, makes crafting any response to a potential future economic shock extremely difficult. Not only must such a response be robust enough to sufficiently address the shock, it must also be designed in such a way as to make clear the U.S. will not go ever deeper into debt as a consequence. Policymakers should therefore include measures to improve the long-term fiscal outlook in any emergency response in order to make near-term borrowing easier and less costly, keep interest rates lower, and strengthen long-term economic growth.

A Four-Part Break Glass Plan for the Next Economic Shock

In advance of the next economic shock, lawmakers should have a Break Glass Plan ready to go. That plan should include a fiscally responsible reaction to the shock and should also address the underlying growth in the national debt. The emergency response will likely need to be implemented quickly, while debt solutions could be implemented more gradually in most cases, with a credible plan for implementation. We suggest a four-part plan that achieves these goals in tandem and can be customized at the time of the emergency to match the specific needs of the economy and budget.

|

A Four-Part Break Glass Plan A four-part Break Glass Plan to address the next economic shock and lower our debt:

|

Part 1: A Targeted Near-Term Policy Response

The nature and scope of any policy response to a potential future economic shock should depend on the nature and scope of the economic shock itself. In general, a response should address the proximate cause of the shock and should be timely, targeted, temporary, and right-sized to avoid overcorrecting. The response should not be used as an opportunity to enact unrelated policies or provide political handouts.

Under a garden-variety demand-driven recession, the primary goal of any policy response should be to help close the output gap – the shortfall between actual and potential economic activity – in the most cost-efficient way possible. When short-term interest rates are higher and recessions are smaller, this can and in many cases should be achieved mainly or perhaps entirely through monetary policy changes. By lowering interest rates, the Federal Reserve can boost economic activity and in turn reduce federal interest payments.

If the output gap is too large to close with interest rate cuts alone, fiscal policy can provide additional support through temporary tax cuts or spending increases focused on boosting aggregate demand. Lawmakers should specifically focus on policies with high multipliers – meaning they produce a large amount of economic activity per dollar of federal borrowing – to deliver the most stimulus at the lowest relative cost. This could include narrow relief such as expanded unemployment benefits or broad-based relief such as one-time tax rebates.

If a recession is partially or largely driven by a supply shock, the response becomes more complicated. Since supply shocks tend to reduce output and increase prices, attempts to address one of these concerns through fiscal and monetary policy could exacerbate the other. In this case, policy should focus to the extent possible on repairing the cause of the shock itself – fiscal stimulus may be unneeded and in many cases counterproductive. If demand has fallen along with supply, stimulus measures may still be called for to support a recovery, but it may be appropriate to limit their size and to couple them with reforms that help lower prices or boost labor and capital supply.

In either of these cases, lawmakers should take care to avoid providing more stimulus than is necessary to close the output gap. As the experience in the early 2020s showed, excessive stimulus can ultimately lead to surging inflation and interest rates, particularly if supply is constrained.

Finally, if an economic shock is caused by a fiscal crisis or inflation crisis, the appropriate response is likely to reduce rather than increase near-term deficits. In our recent paper, “What Would a Fiscal Crisis Look Like?“, we discuss how a debt-driven economic crisis could come about and what forms it could take. Depending on its nature, some near-term spending or tax relief may still be called for to help households and businesses through the recession – but on net, lawmakers will need to focus on spending cuts and revenue increases. Similarly, in the case of an inflation crisis, deficit reduction could support the Federal Reserve in fighting inflation, as we outlined in our 2022 paper, "Fiscal Policy in a Time of High Inflation”.

|

You Can’t Stimulate Your Way Out of a Fiscal Crisis One possible cause of an economic shock is a fiscal crisis, where high levels of current or expected public borrowing leads to Treasury market or economic turmoil. We recently illustrated what a fiscal crisis may look like and surveyed several types of fiscal crises, including:

Although a fiscal crisis may be as or more devastating than other economic shocks, efforts to support the economy with fiscal stimulus may prove counterproductive, or at least ineffective. As a fiscal crisis is caused by high and rising levels of sovereign debt, adding even further to that debt to stimulate the economy could make the underlying crisis worse. To be sure, some targeted fiscal support may be called for, even in a fiscal crisis. For example, a financial crisis might warrant banking interventions, an austerity crisis might call for transition support for the economy, and in any type of crisis policymakers may want to offer aid or relief to those most adversely impacted (for example, enhanced unemployment benefits). But overall, a fiscal crisis is likely to call for lower near-term deficits, not more borrowing. In the case of an inflation or currency crisis, near-term deficit reduction can help temper demand, reduce trade deficits, and lower prices. In the case of any fiscal crisis, deficit reduction can help reassure markets that debt will be put on a sustainable path and that the U.S. will fully meet its obligations. Near-term fiscal stimulus is often an appropriate response to a recession or economic shock. But in an environment where high debt fuels panic, debt-increasing fiscal stimulus can backfire. |

Part 2: Medium-Term Bipartisan Offsets to Pay for Near-Term Relief Twice Over

Although responding to an economic shock may merit near-term borrowing, it should not permanently add to the debt and instead should reduce long-term deficits. Indeed, one risk of responding to a demand- or supply-side shock with borrowing alone is that it could transform an economic downturn into a fiscal crisis, either because the borrowing sparks a debt spiral or provokes a market reaction as investors lose confidence in U.S. fiscal policy.

To avoid worsening the long-term debt or sparking a market reaction or debt crisis, lawmakers should couple any near-term borrowing with enough medium-term savings to not only offset the costs but reduce deficits on net. This could be achieved by embracing “Super PAYGO,” which requires that every $1 of near-term support be coupled with at least $2 of ten-year savings.

Adopting two-for-one deficit reduction would send a signal to creditors that our government is serious about controlling the growth of debt, even as we engage in near-term borrowing to support the economy. It would also encourage lawmakers to be more judicious as they engage in near-term borrowing by making the necessary trade-offs more transparent.

To avoid interfering with the economy’s ability to recover, offsets should be phased in (except under a fiscal or inflation crisis) and designed to generate minimal near-term deficit reduction while demand remains low and the country faces a large output gap.

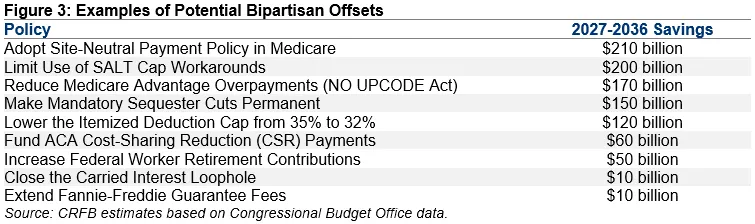

A Break Glass Plan should include a list of agreed-upon offsets in advance and facilitate the enactment of as many as needed to achieve the necessary savings. Fortunately, several bipartisan or potentially bipartisan deficit reduction measures already exist. For example, lawmakers could save roughly $210 billion from requiring Medicare to pay the same rate for care delivered in hospitals as in doctors’ offices (site-neutral payments), raise $200 billion by closing a loophole that states exploit to allow wealthier taxpayers to avoid the state and local tax (SALT) deduction cap, and save $170 billion from modestly reducing Medicare Advantage overpayments.

Our Budget Offsets Bank includes trillions of dollars of potential offsets, many of which have received bipartisan support in the past and would improve the efficiency and efficacy of the budget and tax code.

Part 3: A Default Deficit Reduction Mechanism Following the Economic Downturn

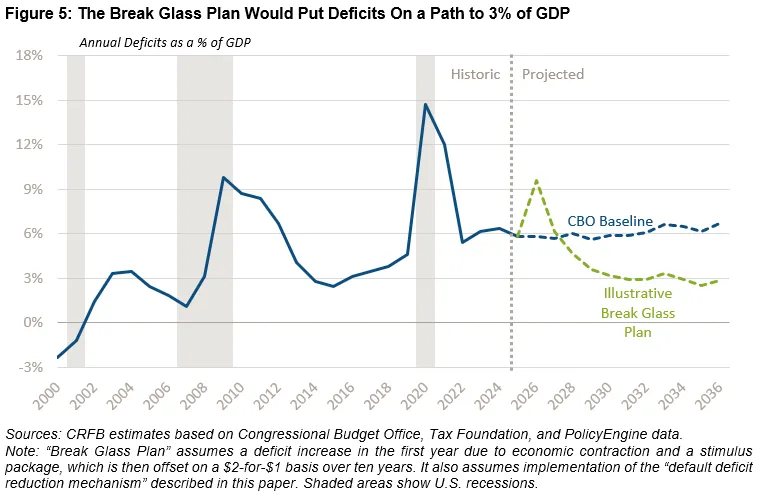

Policymakers should go beyond offsetting the cost of new borrowing and work to stem the growth in deficits and debt projected under current law. By committing to a default deficit reduction mechanism, lawmakers can focus on how to best respond to the emergency in the near-term knowing there will be guardrails in place to put long-term debt on a downward path. This default mechanism would go into effect automatically once the economy has recovered – triggered by a predetermined indicator of economic strength – and would remain in effect until replaced by an act of Congress or until annual deficits fell to 3% of GDP (or an alternative target).

The default deficit reduction mechanism we consider would freeze indexing for most government programs and tax parameters, cap appropriations at flat nominal levels, and phase up a deficit reduction surtax for high-income individuals and corporations.

These changes would be incremental by definition, as they would generally freeze automatic growth in parameters rather than make sharp nominal cuts or increases. This would make them both more manageable for the public and less likely to be discarded by politicians. These modest initial changes would generate compounding – and thus gradually growing – savings over time.

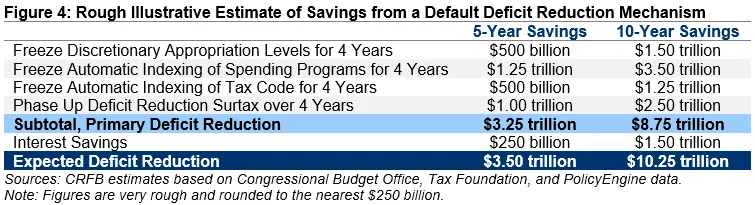

Our very rough, illustrative estimate suggests this mechanism could achieve 3% of GDP deficits if in effect for four years, including a four-year freeze for most parameters and a surtax gradually rising to 2% on income above $100,000 and 4% on corporate and individual income above $1 million. We estimate it could save $3.5 trillion over five years, and $10 trillion over a decade.

Specifically, our very rough estimates suggest that a four-year freeze in the automatic indexing of mandatory spending programs like Social Security, Medicare, and the Supplemental Nutrition Assistance Program (SNAP) could save $3.5 trillion over a decade while a four-year freeze in discretionary appropriations could save another $1.5 trillion.

On the revenue side, estimates from the Tax Policy Center suggest that a four-year freeze in tax parameters would raise more than $1 trillion over a decade.1 And estimates from PolicyEngine and the Congressional Budget Office suggest that a deficit reduction surtax, phased up linearly, would generate $2.5 trillion over a decade.2 Interest savings would generate an additional $1.5 trillion over a decade.

Part 4: A Bipartisan Fiscal Commission

While the automatic default deficit reduction mechanism would put the government on track towards 3% of GDP deficits, it would do so in a somewhat blunt manner. Lawmakers may therefore want to replace these across-the-board cuts with a more thoughtful and targeted tax and spending plan aimed at reducing waste, mitigating distortions, improving efficiency, accelerating economic growth, and addressing the core drivers of rising debt.

To achieve these savings, a Break Glass Plan should establish a bipartisan fiscal commission tasked with developing a bespoke deficit reduction plan to replace the default deficit reduction mechanism, reform the budget and tax code, secure major trust funds, and put the debt on a sustainable long-term path.

Commissions have long been a way for policymakers to tackle complex or politically fraught issues, as we explained in our recent paper, “It’s (Still) Time for a Bipartisan Fiscal Commission”. Historically, commissions have helped policymakers to extend the life of Social Security, consolidate military bases, identify government waste, develop frameworks for tax reform, improve homeland security after 9/11, and draw attention to our unsustainable fiscal outlook. Even when commissions fail to result in enacted legislation, they are often still valuable in terms of facilitating bipartisan discussion as well as developing and socializing novel policy solutions.

Any fiscal commission should be bipartisan and bicameral in nature, including Republicans and Democrats from both the House and Senate. It should be empowered to explore deficit reduction options from both the tax and spending side of the ledger, with as few restraints as possible in terms of deficit reduction options it could propose; the commission should be allowed to consider changes to any federal program or tax provision affecting any demographic or income group.

The commission structure could be based on the recently-proposed Fiscal Commission Act, which would establish a 16-member fiscal commission, including six senators and six members of the House of Representatives – evenly split by party – along with four non-voting outside experts appointed by House and Senate leadership. A similar proposal, the Sustainable Budget Act, would establish an 18-member commission with members selected by the President and House and Senate leadership. The commission would be tasked with developing recommendations that would then receive expedited, no-amendment consideration in both chambers, while still preserving the 60-vote threshold for passage in the Senate.

If potential savings from the commission’s recommendations were projected to be at least as large as savings from the default deficit reduction mechanism, they would replace it in full. Otherwise, savings from the commission’s recommendations could be used to reduce the size and scope of the default mechanism. If the commission failed to officially report an alternative plan or if the officially reported plan was not enacted by the full Congress, the default deficit reduction mechanism would remain in effect.

Conclusion

While no one knows when the next economic shock will hit or what it will look like, it is clear that policymakers are woefully underprepared to address it in a fiscally responsible way. The country is almost certain to enter the next shock more indebted than we have ever been before, which may significantly hamper our ability to marshal an appropriate response.

Rather than devise an ad-hoc response to the next economic shock when it arises, policymakers should develop a responsible Break Glass Plan in advance that can be ready to enact when needed. We believe such a plan should include four parts: a tailored and targeted response to the crisis, enough offsets to ultimately pay for new spending or tax relief twice over, a default deficit reduction mechanism to automatically generate incremental savings over time, and a bipartisan fiscal commission to allow policymakers the opportunity to replace the default mechanism with more thoughtful and specific reforms.

Lawmakers should work together to develop the specifics of a Break Glass Plan based on our framework or any alternative framework that achieves the goal of preparing for the next economic shock without the risk of sparking a fiscal crisis.

The sooner such a plan is ready, the better. One never knows when an emergency will arise, and we must be prepared to break the glass.

1 Numbers are based on modeling by the Tax Policy Center, which estimated that a one-year suspension of indexing in the tax code would save $322 billion over ten years, while a ten-year indexing freeze would save $1.8 trillion. We adjusted their model results to reflect a four-year indexing freeze by compounding the effects of a one-year freeze over four years, then adjusted figures so they matched the results of the ten-year freeze in the first four years. Figures assume a baseline of the tax code in place as of July 5, 2025, and assume customs duty levels consistent with the Congressional Budget Office’s January 2025 baseline. Estimates include microdynamic behavioral responses. Proposals would be effective on 01/01/2027. Estimates assume a fiscal split of 65-35 (65% of calendar year revenue is received by the Treasury in the current fiscal year and 35% in the following fiscal year).

2 We assume a surtax beginning at 0.5% for individual income above $100,000 and 1% for corporate income and individual income above $1 million, which further increases by 0.5%/1.0% per year until deficits fall to 3% of GDP. On the individual side, the surtax is applied to a broad definition of income that includes Adjusted Gross Income (AGI) plus retirement contributions, HSA/MSA contributions, deductible student loan interest, Social Security income not counted toward AGI, interest income on tax-free bonds, and the value of employer-provided health insurance. On the corporate side, the surtax applies to the ordinary corporate tax as well as to the Corporate Alternative Minimum Tax (CAMT) – sometimes described as the Book Minimum Tax – and other minimum taxes. When the deficit falls below 3% of GDP, the surtax would automatically decline linearly in the following tax year, disappearing when the budget was in balance. We estimated the effects of the surtax based largely on numbers from PolicyEngine, who estimated a 1% tax on individual AGI between $100,000 and $1 million and a 2% tax on individual AGI above $1 million would generate about $900 billion over a decade. Additional effects of changes in corporate taxation represent our own estimates based on Congressional Budget Office and Joint Committee on Taxation numbers.