An Overview of the President's FY 2027 Budget

The Trump Administration released its Fiscal Year (FY) 2027 budget request today. While the President’s budget typically presents a comprehensive plan for addressing discretionary spending, mandatory spending, and revenue for the next decade, this year’s budget includes mainly a discretionary spending request and assumptions about how the economy will grow over that period.

In summary, under the President’s budget:

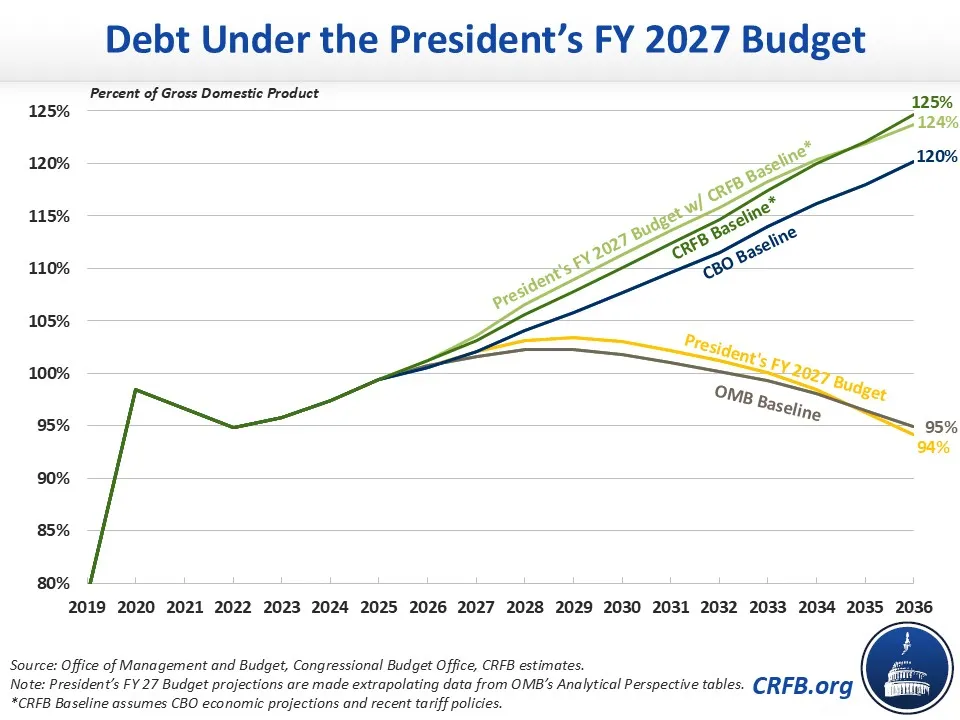

- We estimate that debt held by the public would rise from 100% of Gross Domestic Product (GDP) in FY 2025 to a peak of 103% by 2029 before falling to 94% by 2036 – largely driven by the budget’s economic assumptions.

- Deficits would be $6.7 trillion lower than projected under the Congressional Budget Office’s (CBO) February 2026 baseline from FY 2026 through 2036, largely due to $6.3 trillion of baseline and economic differences as well as about $435 billion of net policy savings.

- Total defense funding would rise to $1.5 trillion in FY 2027, including $350 billion of new reconciliation funding and $251 billion of increases in base defense discretionary funding. This would be somewhat offset by a purported $73 billion reduction in base nondefense discretionary funding.

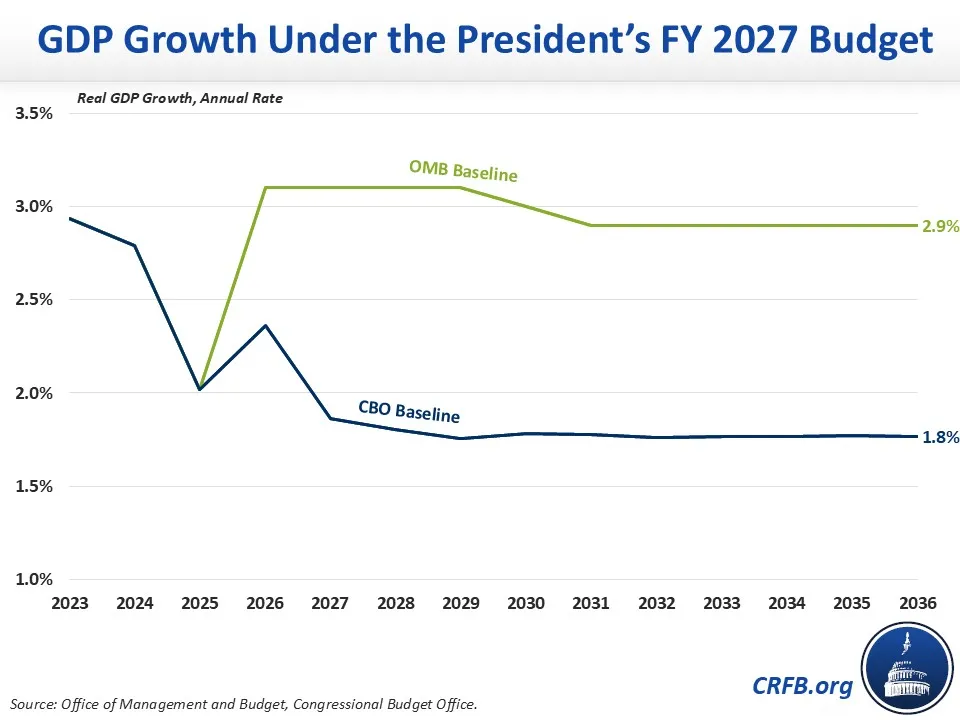

- It is assumed that real GDP would grow at 3% annually on average over the next decade – far above the 1.8% projected by CBO or the 2.0% in the Federal Reserve’s long-run estimates.

- Compared against a baseline assuming CBO’s growth projections, the removal of tariff revenue ruled illegal by the Supreme Court, and the Administration’s recent tariff policies, we estimate debt held by the public would rise to 124% of GDP by FY 2036 under the President’s budget versus 125% under our baseline.

Debt and Deficits Under the President’s Budget

The budget presents no summary figures for debt or deficits; instead, it provides a summary of its discretionary spending request alongside a reconciliation request for further defense funding. However, the various tables in the Analytical Perspectives section allow us to impute debt, deficits, spending, and revenue in both the Office of Management and Budget’s (OMB) baseline and the President’s budget. We find that the budget assumes debt held by the public would grow from 100% of GDP in FY 2025 to a peak of 103% of GDP by 2029 before falling to 94% by 2036.

Many of the fiscal improvements in the budget arise from the generous assumption of 3% average annual real GDP growth over the next decade. As a result of that growth, the budget’s own baseline shows debt peaking at 102% of GDP by FY 2029 and then falling to 95% by 2036.

Budget deficits under the President’s budget would be on a path to the important 3% of GDP target, but again only because of overly optimistic economic assumptions. Specifically, deficits would fall from 6.4% of GDP in FY 2026 and 2027 to 3.2% by 2034 and 2.6% by 2036. In dollar terms, the deficit would grow from $2.1 trillion in FY 2026 to $2.2 trillion in 2027 then fall to $2.0 trillion in 2029 and $1.3 trillion by 2036. The decrease in deficits is primarily driven by the budget’s rosy economic assumptions and some net policy savings achieved largely through reductions in nondefense discretionary spending.

It is also important to note that the budget assumes tariff revenue continues to come in at the pace prior to the Supreme Court ruling that tariffs imposed under the International Emergency Economic Powers Act (IEEPA) are illegal, which we estimated would reduce revenue by $1.7 trillion through 2036. The President has since implemented additional temporary tariffs.

Under a baseline incorporating CBO’s growth projections and changes in tariff policy over the past few months, the budget’s net policy savings would result in debt increasing to 107% of GDP by FY 2028, 116% by 2032, and 124% by 2036. Deficits would rise to a high of 7.0% of GDP by 2028 before falling to 6.4% in 2032 and remaining there by 2036.

Comparing the President’s Budget to CBO’s Baseline

Although the President’s budget does not include standard summaries of its fiscal metrics, using the supplemental information in the Analytical Perspectives and historical tables we estimate that the President’s budget projects deficits that are $6.7 trillion lower than CBO’s February 2026 baseline from FY 2026 through 2036.

Comparing Deficits Under CBO's Baseline and The President’s Budget

| FY 2026 – FY 2036 | |

|---|---|

| Deficits in CBO’s February 2026 Baseline | $26,260 billion |

| Baseline/Economic Differences | -$6,295 billion |

| Revenues | -$7,770 billion |

| Discretionary Outlays | +$805 billion |

| Mandatory Outlays | +$3,210 billion |

| Interest Outlays | -$2,540 billion |

| Budget Net Savings | -$435 billion |

| Revenues | n/a |

| Discretionary Outlays | -$880 billion |

| Mandatory Outlays | +$365 billion |

| Interest Outlays | +$80 billion |

| Deficits in the President’s FY 2027 Budget | $19,540 billion |

Note: figures are rounded to the nearest $5 billion and may not sum due to rounding.

Sources: CRFB estimates based on OMB figures and CBO projections.

The bulk of this difference is driven by differing baseline and economic assumptions. OMB estimates that revenues will be about $7.8 trillion higher from FY 2026 through 2036; most of this difference is likely due to OMB's substantially more optimistic economic growth assumptions, described further below. Another $1.5 trillion of baseline differences offsets some of the higher revenue, resulting in baseline and economic differences of roughly $6.3 trillion through 2036.

The budget achieves about $435 billion of net savings against its own baseline. Most of this comes from its reductions to nondefense discretionary spending (described below), somewhat canceled out by the increase in defense discretionary spending over the next five years. Finally, the budget includes about $365 billion of mandatory spending increases – $350 billion from defense reconciliation resources and a net $15 billion from other mandatory spending proposals – and $80 billion from increases in net interest outlays above baseline.

In total, using OMB’s figures, we estimate the President’s budget purports to result in deficits of $19.5 trillion from FY 2026 through 2036 compared to $26.3 trillion in CBO’s February 2026 baseline.

Discretionary Spending Under the President’s Budget

While the budget lacks most details on mandatory spending proposals, it includes a discretionary spending request for FY 2027 and proposes discretionary levels for the next decade.

Specifically, the budget calls for boosting total defense funding to $1.5 trillion in FY 2027; OMB claims this would be a 42% increase ($445 billion) above FY 2026 enacted levels, but that figure inappropriately assumes that $155 billion of defense funding from the One Big Beautiful Bill Act is part of the baseline and an additional $350 billion of funding is provided in a new reconciliation law. In actuality, the budget requests $251 billion (28%) more base defense funding along with the $350 billion of new reconciliation funding.

Proposed Discretionary Spending in the President’s FY 2027 Budget

| FY 2026 Enacted | FY 2027 Request | % Change | |

|---|---|---|---|

| Base Discretionary Funding | $1,636 billion | $1,814 billion | +10.9% |

| Defense | $903 billion | $1,154 billion | +27.8% |

| Nondefense | $733 billion | $660 billion | -10.0% |

| Defense Reconciliation Resources | $155 billion | $350 billion | n/a |

| Total Defense Funding | $1,058 billion | $1,504 billion | +42.2% |

Sources: Office of Management and Budget.

In total, we estimate that the budget would increase total defense funding (budget authority) by $3.2 trillion over ten years compared to our estimate of CBO’s baseline incorporating final FY 2026 appropriations.

To partially offset these costs, the budget would reduce funding for nondefense discretionary (NDD) programs. It purports to reduce base NDD by 10% – $73 billion – in FY 2027 before enacting a “two-penny” plan where base NDD falls by 2% annually for the rest of the decade. We estimate that this would result in $2.5 trillion of lower NDD budget authority over a decade compared to our estimate of CBO’s baseline incorporating final FY 2026 appropriations.

Economic Assumptions in the President’s Budget

Outside of the budgetary estimates, the President's budget includes a ten-year economic forecast that is significantly more optimistic about the economy than other mainstream forecasters, such as CBO and the Federal Reserve.

OMB expects real GDP growth to average 3.0% throughout the decade, compared to CBO’s estimate of 1.8% average growth and the Federal Reserve’s 2.0% long-run growth estimate.

The President’s budget also forecasts inflation as measured by the GDP price index will fall from 2.8% in calendar year 2025 to 2.7% in 2026 and moderate at 2.0% thereafter. This is compared to CBO’s projection that GDP price index inflation will be 2.7% in 2026, decline to 2.4% in 2027, and moderate at 2.0% starting in 2030.

Regarding interest rates, OMB forecasts that yields on the ten-year Treasury note will drop 0.9 percentage points from 4.3% in 2025 to 3.4% by 2029 and stabilize at 3.3% thereafter, while CBO expects interest rates on ten-year Treasuries to remain high and rise throughout the decade from an average of 4.1% in 2026 to 4.4% by 2031 through 2036.

Labor market projections are also more optimistic under the President’s budget, with the annual average unemployment rate falling to 3.9% in 2026 from a rate of 4.2% in 2025 and to 3.7% by 2027 and onward through the decade. CBO projects an increase in the unemployment rate from 4.3% in 2025 to 4.6% in 2026, falling to 4.4% in 2029 and 4.2% by 2033.

* * * * *

While the budget does propose to reduce nondefense discretionary spending, it fails to give a complete picture of its projected effects on debt and deficits. Worse, the budget relies on wishful thinking and generous economic assumptions for the majority of its fiscal improvements. Unfortunately, this budget provides little guidance on how policymakers should put the national debt on a sustainable path.