Student Debt Cancellation is Not Financially Justified

The White House has justified the unilateral implementation of its $400 billion student debt cancellation plan based on authority the Secretary of Education has to prevent borrowers from being “placed in a worse position financially” as a result of a national emergency. The majority of those who will benefit from debt cancellation, however, are not currently in a worse position financially as a result of the COVID-19 pandemic.

The Biden Administration has based its legal argument on an interpretation of the HEROES Act of 2003 that targeted service members for debt relief in the wake of the September 11th attacks and subsequent war, although it now faces challenges over whether this is a legal use of the Administration’s authority. A recently released memo from the Department of Education argues that many student loan borrowers remain in a financially worse position as a result of the pandemic, that delinquency and default will rise substantially above pre-pandemic levels without debt cancellation, and that elevated inflation has further worsened conditions for borrowers. However, these claims are largely based on selectively reading and misreading the relevant data.

In this analysis, we show that:

- Most borrowers are financially better off as a result of the response to the pandemic.

- There is little evidence that delinquencies will spike due to the pandemic.

- High inflation erodes student debt, making it easier – not harder – to repay.

- Only a small share of debt cancellation helps those hurt by the pandemic.

Most Borrowers Are Financially Better Off

While the Department of Education argues that “many student loan borrowers remain at risk of being placed in a worse position financially as a result of the COVID-19 pandemic and its associated economic effects,” the data tell a different story. In fact, household balance sheets remain stronger than before the pandemic.

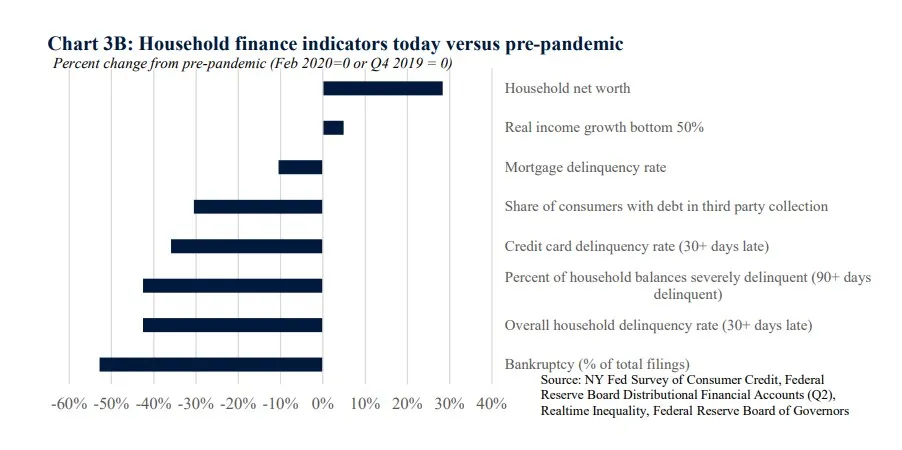

Indeed, the Biden Administration acknowledges this. In a recent report, the White House states that “household finances are stronger than pre-pandemic, putting families in a better position to navigate the economic challenges flowing from disruptions to the global economy,” pointing to huge increases in household net wealth, modest increases in real income for the bottom half, and substantial reductions in delinquency and bankruptcies.

Source: White House

It is important to understand that while Americans did suffer financially as a result of the pandemic, they also benefited from roughly $6 trillion in authorized COVID relief. Since the pandemic began, a typical borrower with $35,000 of debt has benefited from over $6,000 in cancelled interest under the pause, along with $3,200 of recovery rebates ($11,400 for a family of four). Borrowers may have also received thousands or tens of thousands of dollars more from an expanded child tax credit, generous unemployment benefits, expanded SNAP benefits, health care subsidies, housing support, Paycheck Protection Program funding, payments from state governments, or other forms of aid.

Thanks in large part to these measures, household income spiked throughout the pandemic. As we’ve shown, personal disposable income was more than $4 trillion (13 percent) higher in 2020 and 2021 than in the prior two years. As a result, checking account balances are 30 to 35 percent higher than before the pandemic, with median cash balances well above pre-pandemic levels at all income levels.

Labor markets also remain strong. The current unemployment rate of 3.5 percent is tied for the lowest in the last fifty years. Americans with a college degree have especially benefited from the strong economy, with the September unemployment rate for those with a bachelor’s degree or higher at 1.8 percent.

Little Evidence Delinquencies Will Spike

The Department of Education argues that student debt delinquencies will spike to well above pre-pandemic levels if payments are restarted without cancellation. However, this claim is largely based on a mathematical error in reading survey data.

The Department claims that “of those with income under $40,000, only 26 percent reported never or occasionally making full payments in 2019, but 51 percent in this group expect to have difficulty making full or even any payments in the future,” and makes similar claims of other income groups. However, the 26 percent figure they cite is of all borrowers, while the 51 percent figure is only as a share of the two-thirds of borrowers who were required to make payments in 2019.

On an apples-to-apples basis, we find the percent of those required to make payments in 2019 who don’t expect to make full payments in 2023 rose only modestly, from 26 percent to 33 percent, based on the cited data. The actual rise in delinquency is almost certainly much smaller, since some of those borrowers won’t be required to make payments in 2023 and since people tend to be more pessimistic in survey data.

It is especially likely to be smaller in light of recent administrative actions. For example, the Biden Administration cancelled at least $32 billion in targeted cancellations that will mainly help those at high risk of delinquency – including those who attended fraudulent institutions and those on permanent disability. The Administration also has initiatives to move most defaulted debt out of collection or into an income-driven repayment program and to make it easier to get debt discharged from attending a fraudulent institution. Along with 2.5 years of interest cancellation, these actions should lead to a lower delinquency rate.

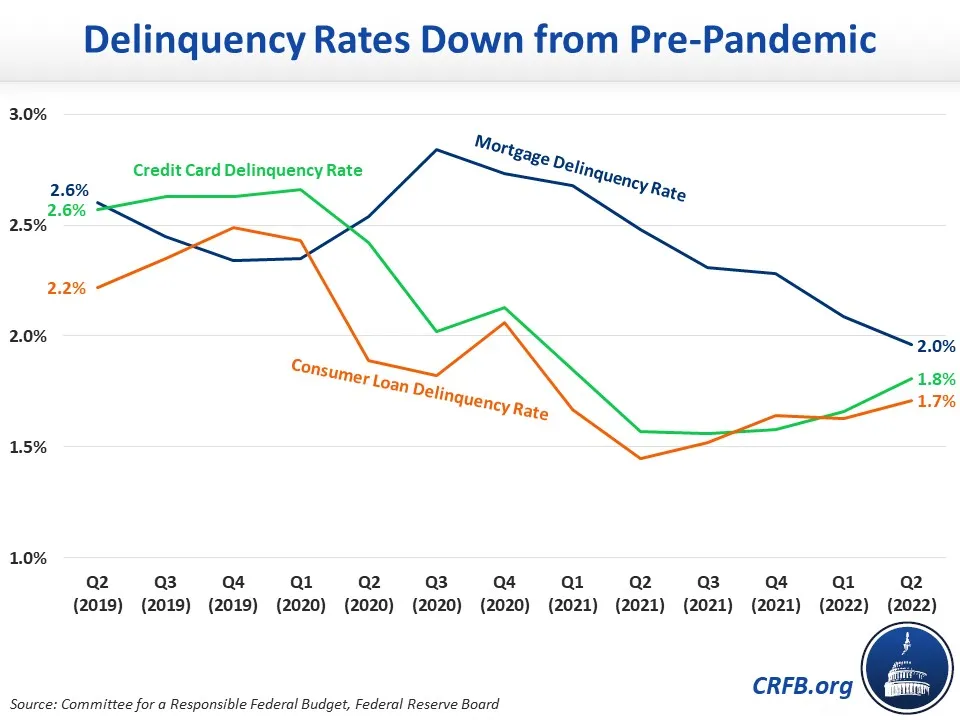

Other data and studies similarly suggest delinquency rates will be at or below pre-pandemic levels. For example, a study by the New York Federal Reserve found that the commercially-held federal loans returned to about the same rate of delinquency as before the pandemic after forbearance ended, suggesting delinquency rates on government-held student loans may do the same.

In fact, delinquencies are down across all major categories. The delinquency rate for credit card loans was 1.8 percent in the second quarter of 2022 compared with 2.6 percent in the second quarter of 2019. The mortgage delinquency rate has dropped from 2.6 percent in the second quarter of 2019 to 2.0 percent in 2022. And consumer loan delinquency rates fell from 2.2 percent to 1.7 percent.

High Inflation Erodes Debt, Making Repayment Easier

While the Department of Education is right that “The rise of inflation to levels not seen in 40 years also creates significant pressures on family budgets,” they omit the fact that this inflation also offers a large benefit for fixed-interest debt holders.

By reducing the real (inflation-adjusted) value of student debt, the recent surge in inflation should make it easier for most borrowers to pay back their debt. Thanks to above-target inflation, a typical borrower with $35,000 of student debt has seen nearly $3,000 of that debt erode due to inflation. Because high inflation is feeding – at least in part – into higher wages, that debt is now more affordable.

Indeed, the total value of outstanding student debt declined by 6 percent since the beginning of the pandemic, despite the fact that very little debt has been repaid and new debt continues to be issued. As a share of total compensation, debt has fallen by 9 percent since the beginning of the pandemic. Or described another way, total outstanding student debt has declined from 16 percent of pay to 14.5 percent.

It is also important to note that the debt cancellation itself will likely exacerbate inflation, making it more difficult for households without student debt to afford goods or services and increasing the risk that actions to fight inflation will lead to a recession.

Most Debt Cancelled Won’t Help Pandemic Victims

Although the Administration is justifying their student debt cancellation as protecting borrowers who have been harmed by the pandemic, the majority of beneficiaries do not fit this description.

In a separate analysis, we’ve shown that up to two-thirds of the benefit of debt cancellation will accrue to the those in the top half of the income spectrum. And as we’ve discussed above, households from all parts of the spectrum are largely financially better off as a result of the pandemic response, do not appear to be at elevated risk of delinquency, and have seen their relative debt burden decline as a result of the payment pause and high inflation.

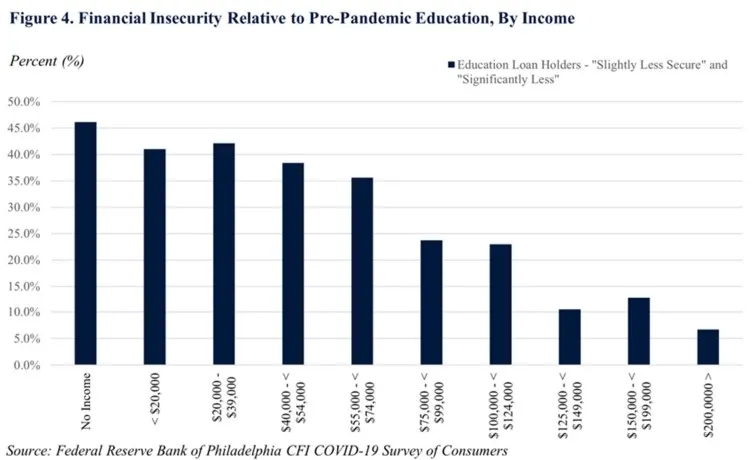

Indeed, the very data presented by the Department of Education to make their case show that the majority of borrowers in all income groups report being at least as financially secure now as they were before the pandemic. Only about two-fifths of those making less $40,000 report being less secure, and less than a quarter of those making $75,000 to $125,000 report being less secure.

Source: Department of Education

Based on the same data source, those at similar income levels without student debt report being far less secure. For example, among those with student debt making $100,000 to $125,000, 57 percent report being more financially secure and 7 percent significantly less secure; among those making $100,000 to $125,000 without student debt, only 12 percent report being more secure and 9 percent report less.

This survey suggests that those most negatively affected by the pandemic are not holders of student debt, but instead those who never went to college in the first place.

Student debt cancellation is a poorly targeted solution that will mostly help borrowers whose finances were not adversely affected by the pandemic and as the data make clear, cancellation is not financially justified.