OBBBA Dynamic Score Comes In at $4.7 Trillion

The “One Big Beautiful Bill Act” (OBBBA) will add $4.2 trillion to the national debt through Fiscal Year (FY) 2034 or $4.7 trillion through 2035 after taking into account its dynamic effect on the economy, according to new estimates included in the Congressional Budget Office’s (CBO) latest Budget and Economic Outlook. Dynamic effects alone account for $125 billion of the cost of the bill through 2034 (and roughly $160 billion through 2035), with the fiscal effect of higher interest rates outweighing the impact of stronger economic growth.

Before its passage, CBO scored OBBBA as adding $4.1 trillion to the national debt from FY 2025 through 2034 – including roughly $5.9 trillion of tax cuts and spending increases, $2.5 trillion of offsets, and over $700 billion in interest costs. This ‘conventional’ score took into account behavioral changes caused by the law’s provisions but not its effect on the overall economy, as would be done under ‘dynamic’ scoring.

CBO’s newest estimates are consistent with their previous score, finding the law will reduce net revenues by nearly $4.5 trillion through FY 2034, reduce net spending by nearly $1.1 trillion, and increase interest payments by over $700 billion, bringing the conventional score to $4.1 trillion. From 2026 through 2035 – a full 10-year budget window1 – CBO projects the law will reduce revenue by $4.9 trillion, reduce spending by $1.2 trillion, and increase interest costs by over $850 billion, for a total conventional deficit impact of $4.5 trillion.

On a dynamic basis, CBO projects the law will further increase deficits – by $4.2 trillion from FY 2025 through 2034 and by $4.7 trillion from 2026 through 2035. While the positive economic impact will boost revenue and thus reduce primary deficits by $280 billion from 2025 through 2034 (about $315 billion from 2026 through 2035), it would also boost interest rates and thus increase interest costs by $405 billion (roughly $475 billion from 2026 through 2035).

CBO’s Conventional and Dynamic Score of the One Big Beautiful Bill Act

| FY 2025-2034 | FY 2026-2035 | |

|---|---|---|

| Revenue Effects | -$4.5 trillion | -$4.9 trillion |

| Spending Effects | +$1.1 trillion | +$1.2 trillion |

| Interest Effects | -$720 billion | -$860 billion* |

| Conventional Score | -$4.1 trillion | -$4.5 trillion* |

| Dynamic Primary Deficit Effects | +$280 billion | +$315 billion* |

| Dynamic Interest Effects | -$405 billion | -$475 billion* |

| Dynamic Score | -$4.2 trillion | -$4.7 trillion |

* Figures reflect CRFB calculations based on CBO data, rounded to nearest $5 billion

Sources: Congressional Budget Office, Committee for a Responsible Federal Budget. Negative values increase deficits.

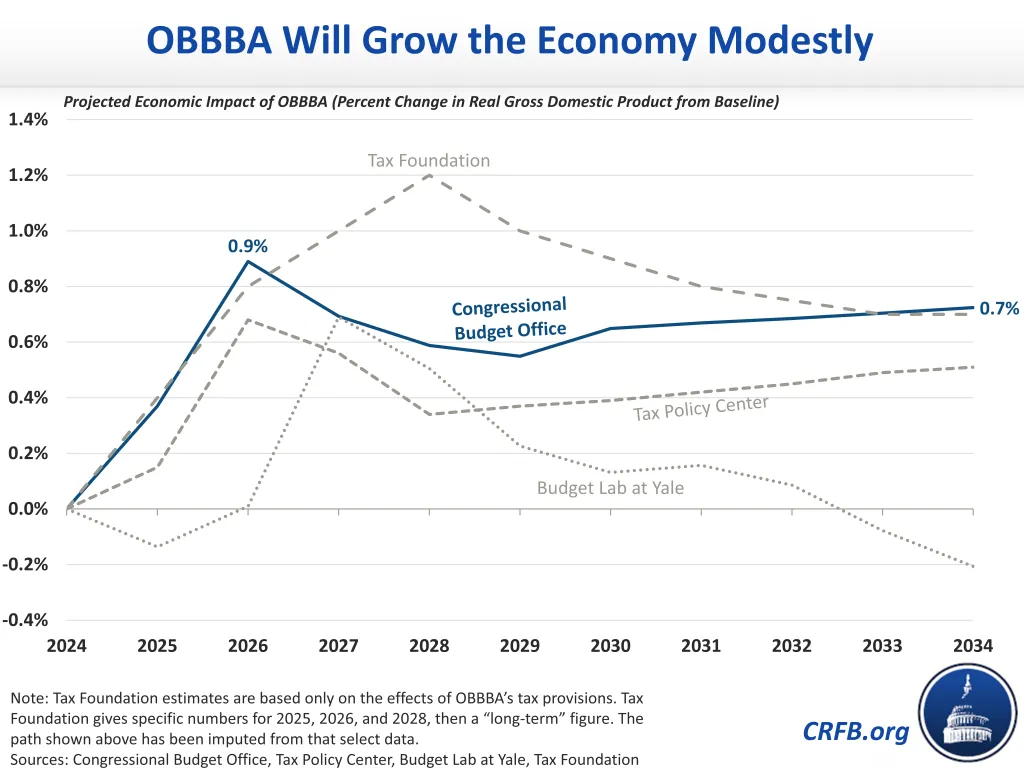

Economic Impact of OBBBA

CBO projects OBBBA will boost both output and interest rates.

CBO estimates the law will raise real Gross Domestic Product (GDP) by an average of 0.7% over the budget window, with a 0.9% increase in real GDP in 2026, declining to 0.5% in 2029 before rebounding and stabilizing at 0.7% through the latter half of the decade. Similarly, the Tax Foundation expects a long-term boost of 0.7%2 and the Tax Policy Center projects a 0.5% boost, while Yale Budget Lab projects a 0.2% reduction in output. These figures represent change in total output relative to baseline, not changes in the growth rate.

In the near-term, CBO attributes much of the improvement in GDP to higher demand for goods and services, as lower taxes and higher spending lead to a temporary boost in economic activity (a stimulative or sugar high effect).

Over time, the law will have a variety of effects on output. Lower tax rates, reduced income and higher education support, new work requirements, and tax breaks for certain activities such as overtime work are projected to boost the overall labor supply, increasing total hours worked and boosting output. Meanwhile, reduced tax rates, pass-through business tax cuts, and investment tax incentives such as full expensing are projected to boost investment and thus increase the stock of factories, equipment, software, and other capital.

Partially countering these effects, new immigration enforcement will reduce labor supply while limits to certain tax breaks – especially related to housing (mortgage interest, property taxes) and energy (IRA tax credits) – will reduce investment and thus capital supply. Furthermore, the increase in federal borrowing attributable to the law will eventually increase interest rates and thus the user cost of capital, resulting in a “crowding out” effect which will grow over time.

Overall, CBO projects OBBBA will increase the labor supply by an average of 0.4% from 2025 through 2034. It will increase private investment by an average of 1.2%, peaking at a 2.3% increase in 2027 before settling at an 0.6% increase by the end of the decade. CBO projects the law will also slightly increase total factor productivity.

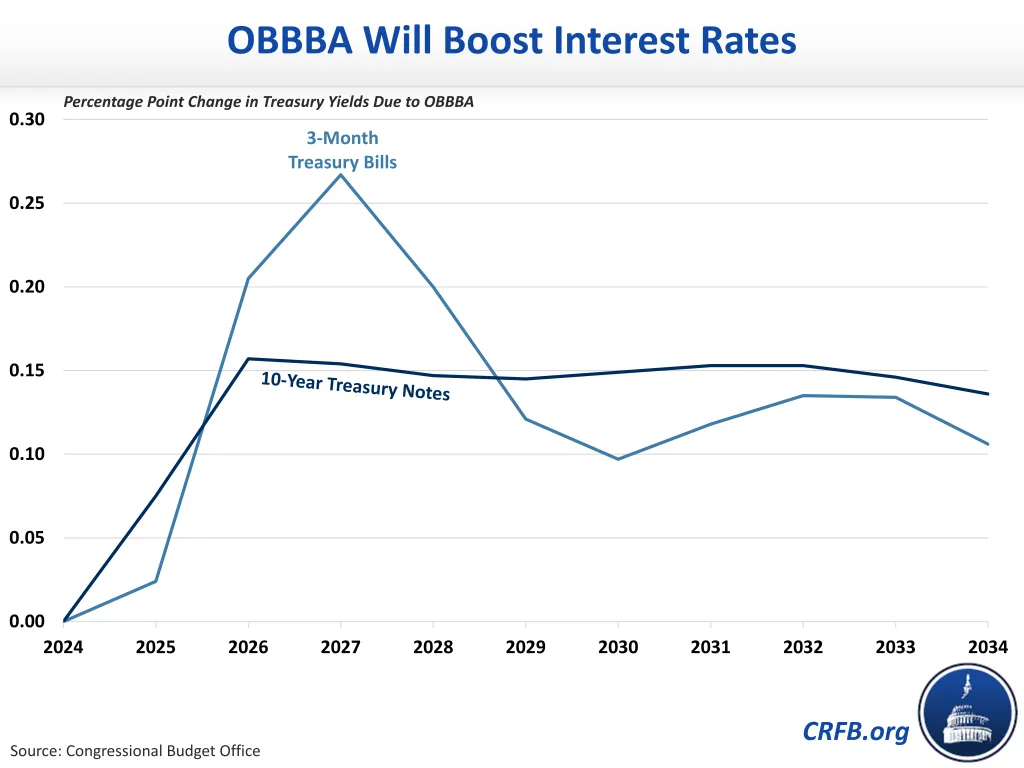

At the same time, CBO projects OBBBA will significantly increase interest rates, both as the Federal Reserve responds to the surge in demand and as rising debt crowds out private investment. Specifically, CBO projects the increase in interest rates on three-month treasuries will peak at 0.27 percentage points above baseline estimates in 2027 before coming back down to an increase between 0.10 and 0.14 percentage points through the latter half of the decade. Meanwhile, the increase in interest rates on ten-year treasuries will peak at 0.16 percentage points in 2026, then decline slightly to a 0.14 percentage point increase by 2034.

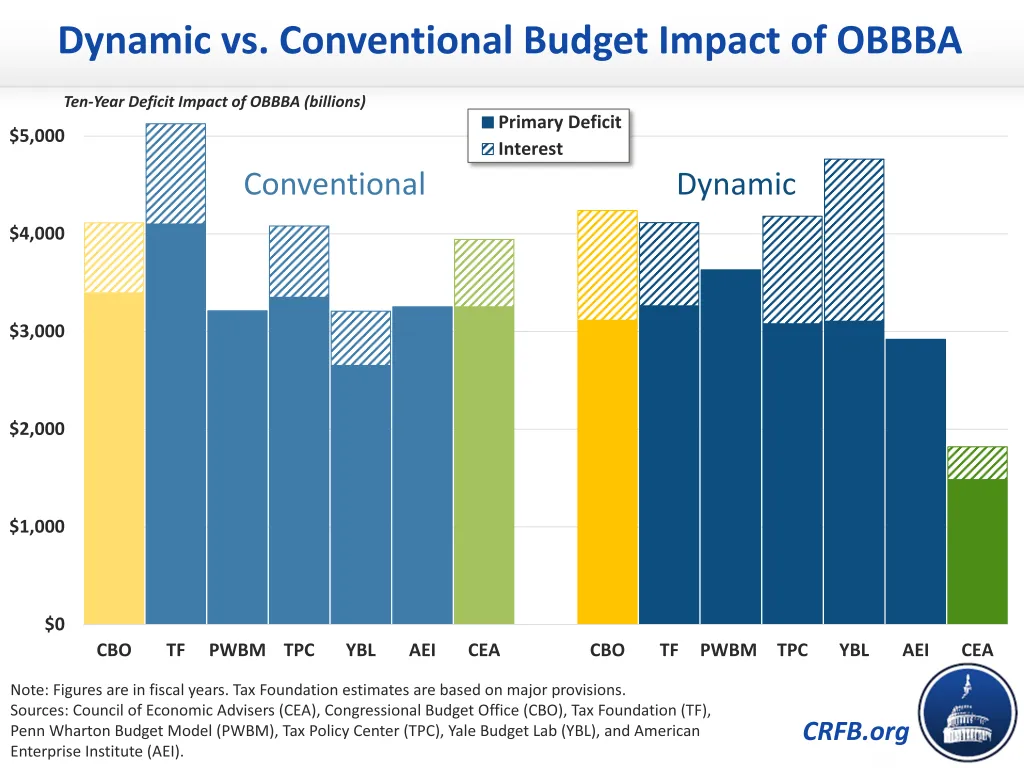

Comparing CBO to Other Estimates

CBO’s dynamic score of OBBBA is similar to that of other forecasters. Through FY 2034, CBO estimates the bill will increase primary deficits by $3.1 trillion and total deficits by $4.2 trillion. Other independent estimates range from $2.9 to $3.6 trillion on a primary basis and $4.1 to $4.8 trillion with interest.

CBO’s estimate of the dynamic effect in particular – a $125 billion cost through FY 2034 – is most similar to Tax Policy Center, which estimates a $100 billion dynamic cost. Penn Wharton Budget Model and the Budget Lab at Yale also estimate additional dynamic costs of $420 billion (excluding interest) and $1.6 trillion (including interest), respectively.

By comparison, the Tax Foundation estimates dynamic effects will reduce deficits by $1 trillion, or one-fifth of conventional cost. However, they do not account for the negative economic impact of debt on interest rates or growth. Finally, the White House’s Council of Economic Advisers finds the law’s dynamic effects will reduce its deficit impact by $2.1 trillion including interest – or by more than half of their conventional estimate – though their estimate is far outside of the mainstream.

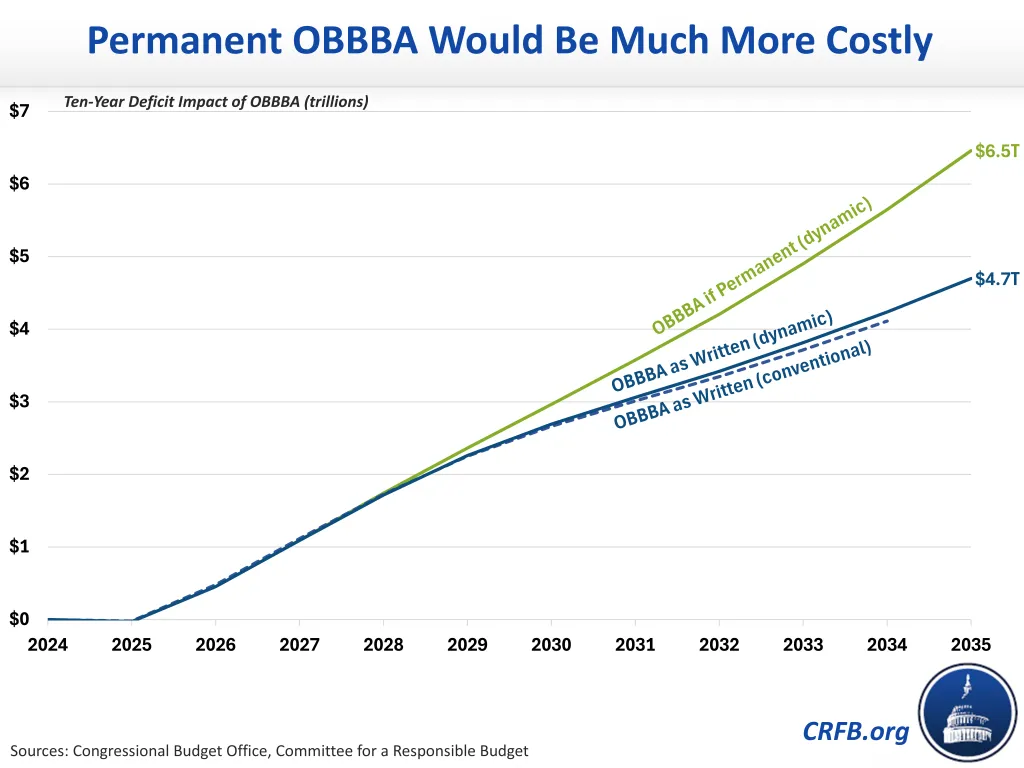

OBBBA Could Cost More If Extended

While CBO projects the law will add $4.7 trillion to debt over the coming decade, that amount could ultimately be much higher if several of the law’s temporary policies are made permanent. The law includes several new individual tax cuts that are set to expire after 2028, including exclusions for tips and overtime income, a larger standard deduction for seniors, an exclusion for car loan interest, and an exclusion for contributions to “Trump Accounts”. The law temporarily increased the deduction for State and Local Taxes (SALT) through 2029, allows for full expensing of factories through 2028, and extended a reformed version of the Clean Fuel Production Credit through 2029. On the spending side, the law included temporary boosts in funding for immigration enforcement, border security, national defense, health care, and other purposes.

If these temporary tax breaks and spending programs were made permanent, we estimate the law will add more than $5.6 trillion to the debt through FY 2034 and nearly $6.5 trillion through 2035. These estimates do not account for the dynamic impact of the extension. Accounting for economic feedback could make the permanent cost even higher, as higher debt would further push up interest rates and temper positive economic effects from lower tax rates.

* * * * *

Our national debt is currently roughly the size of our economy. Prior to the passage of OBBBA, CBO projected that debt would surpass its all-time record as a percentage of the economy in FY 2029. Yet, lawmakers enacted a law that will increase debt by nearly $5 trillion over the coming decade, and potentially by much more if temporary provisions are extended. Within that law, they included approximately $2.5 trillion in offsets that could have gone toward actually reducing the deficit but instead served only to make an expensive law slightly less so. This kind of fiscal irresponsibility simply cannot continue. Going forward, lawmakers must make reducing deficits and putting debt on a sustainable, downward path a major priority. Furthermore, they must not continue to waste potential offsets on deficit increasing bills and instead use them to actually reduce deficits.

Otherwise, our nation’s fiscal outlook will rapidly become even more dire than it already is.

1 Scoring the law using the FY 2025-2034 window – which happened because lawmakers used the FY 2025 Concurrent Budget Resolution to enact it via reconciliation – was unusual at the time given that OBBBA passed with just three months left in FY 2025 and most of its provisions (extensions of the expiring 2017 tax cuts) wouldn’t take effect until FY 2026.

2 Tax Foundation’s analysis applies only to OBBBA’s major tax provisions.