Large Benefit Cuts Loom for Social Security

The Social Security retirement program is just six years from insolvency, according to the program’s trustees. At that point, the law requires benefits to be reduced by an estimated 22% to ensure the program’s costs do not exceed its revenues after the retirement fund is exhausted in late 2032. That is when today’s 61-year-olds will reach their normal retirement age and when today’s youngest retirees turn 68.

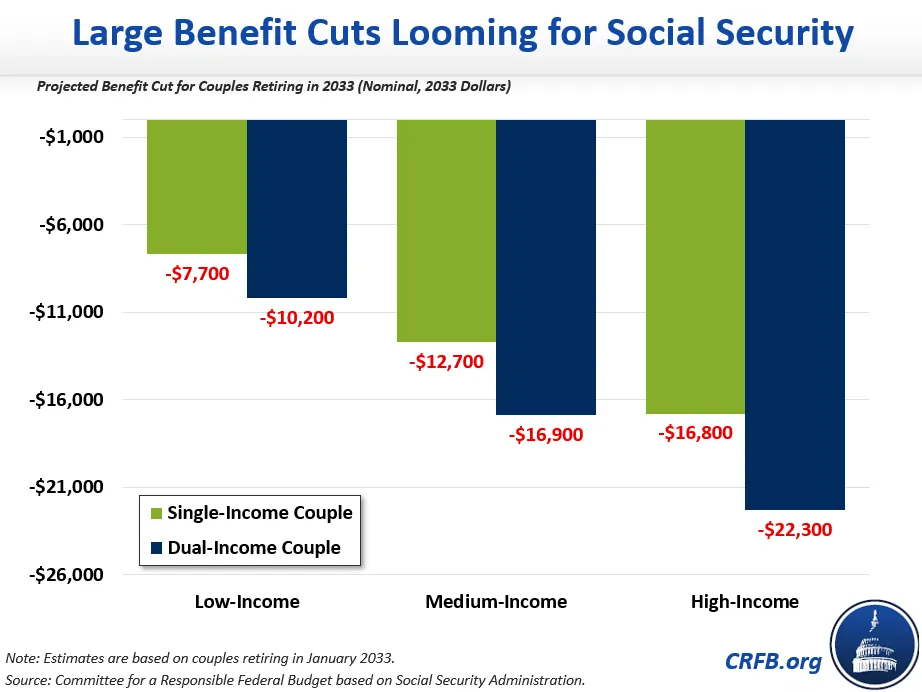

We estimate that a cut of this magnitude will cause a typical, newly retiring dual-earning couple to lose $16,900 in annual benefits at the start of 2033, shortly after trust fund insolvency. Later that year, the Medicare Hospital Insurance trust fund is projected to become insolvent, cutting spending by 11%, which would threaten retirees’ health care access while they experience the Social Security shock to their incomes.

The size of these benefit cuts would vary with a couple’s age, marital status, and work history. For example, a typical single-income couple would face an annual loss of $12,700 while a dual-earning, low-income couple would face a yearly cut equal to $10,200. And high-income couples would see cuts as large as $22,300. While the absolute size of these cuts would be smaller for low-income couples than high-income couples, they would also be a larger share of total incomes for low-income retirees and hence more financially disruptive. These cuts are in nominal dollars and would be about 15% smaller when adjusted for inflation.

These benefit cuts are smaller than we estimated last year – due mainly to the higher near-term revenues and lower near-term costs projected in this year’s Trustees’ report. However, these cuts are projected to grow over time due to the rising gap between Social Security’s costs and dedicated revenues. At the end of the century, annual benefit cuts are expected to reach 35%.

With the insolvency of the Social Security retirement fund just six years away, Social Security’s insolvency is no longer a crisis for future lawmakers to deal with; senators elected this year will be in office when Social Security’s retirement fund is exhausted. Policymakers should urgently begin the work of restoring Social Security’s long-term solvency and preventing a 22% benefit cut. We have proposed several novel solutions over the past year – an Employer Compensation Tax, a Social Security COLA Cap, and a Six Figure Limit on Social Security benefits – to help kickstart that important work of finding trust fund solutions. Absent Congressional action, retirees in every state will be impacted. The time to act is now.