Even Fiscal Doves Now Worry About the Debt

The national debt is on an unsustainable path and represents a growing threat to the budget and economy. Increasingly, even former “fiscal doves” are raising concern.

Last week, Center for American Progress Senior Fellow and former Council of Economic Advisers Chair Jared Bernstein and Senior Director of Federal Budget Policy Bobby Kogan warned that “federal debt is larger and more expensive than in previous generations” and “matters more than it used to.” Bernstein had previously declared that “if you’re not worried about this country’s fiscal outlook, you’re not paying attention.”

Also in recent weeks, economist Justin Wolfers has said that “debt is worrying now” while former Biden Administration economist Martha Gimbel of the Yale Budget Lab asserted “the consequences of debt are…already here.” Meanwhile, commentators Derek Thompson, Noah Smith, and Matthew Yglesias have explained that “it’s not just conservatives who are starting to worry about the trajectory of American taxing and spending” and argued that we’re “headed for a debtpocalypse” and so it is now “time to freak out about the national debt.”

Kogan and Bernstein, in their recent piece, point out that the combination of large primary deficits, high levels of debt, and rising interest rates relative to economic growth rates (R versus G) put the U.S. in a particularly precarious position. “At a minimum,” they remark, the underlying dynamics suggest “that ever-rising debt entails more downside risk than economists and budgeteers previously thought.”

In a prior piece, Bernstein, who recently testified in front of the House Budget Committee and endorsed a 3% of Gross Domestic Product (GDP) deficit target, remarks that he was previously a fiscal “dove.” Within his work, he notes that “the combination of higher deficits and climbing interest rates raises the risk that borrowing will become more expensive and will push government debt levels to climb relentlessly. This is a debt spiral.”

And Bernstein is not the only one. On Derek Thompson’s podcast, Plain English, and in a subsequent Substack post, both Thompson and Justin Wolfers, economist at the University of Michigan, expressed similar concern. After spending “years arguing against debt scolds,” Wolfers explains that both he and Thompson pointed to high debt, large deficits, and inattentiveness of the political system as reasons to accept the “very real possibility that … [a fiscal] reckoning is just around the corner.”

As Wolfers explained: “Derek wanted to say: even center-left economics professor Justin Wolfers is worried about the debt. I kept trying to say: even center-left economics journalist Derek Thompson is worried about the debt.” Thompson echoes many of Wolfers’s concerns, with the rising risk of a debt crisis due to high interest rates and rising inflation. He notes that his younger self believed in high deficits due to the situation the U.S. was in but that current deficits in the current economic setting are high risk and low reward.

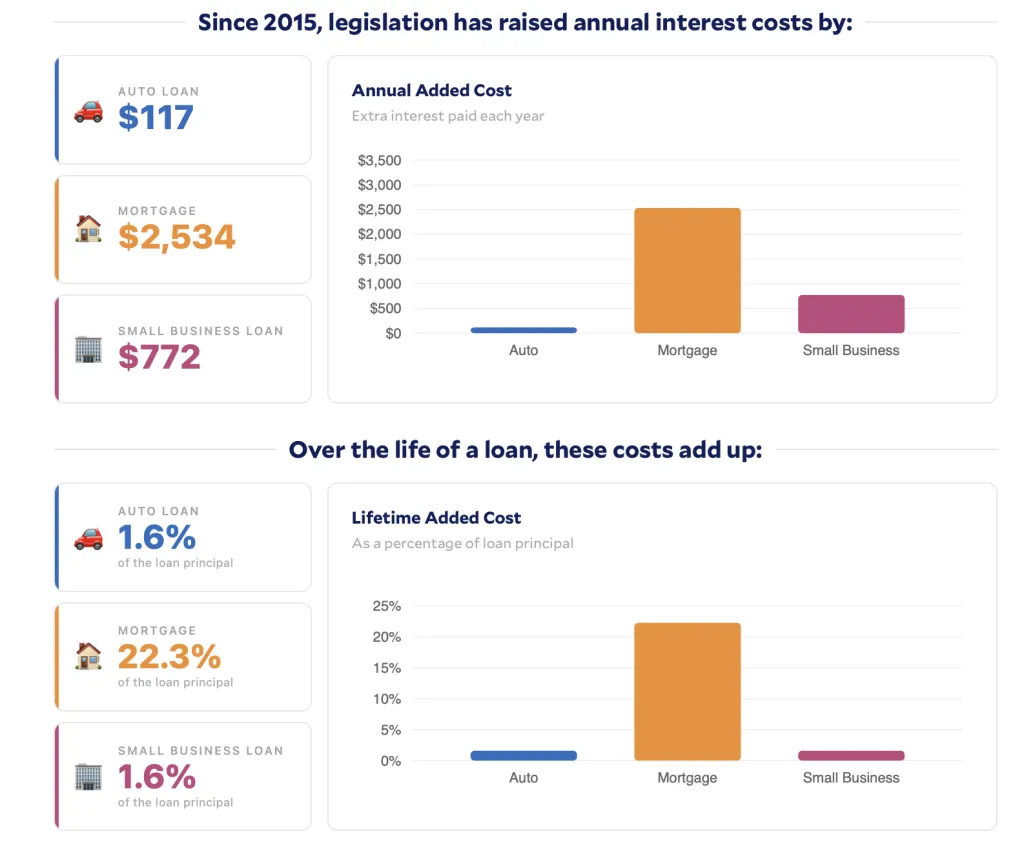

Meanwhile, Gimbel, who was described as a deficit dove as recently as 2024, penned a recent piece in The Atlantic on the detrimental impact of the national debt on household finances. Gimbel pointed to estimates that legislation over the past decade has already boosted interest rates by a full percentage point. “For someone taking out a 30-year mortgage at last year’s median home price” she explains, “this rise in long-term interest rates has increased their borrowing costs by about $2,500 a year, or roughly $76,000 over the life of the loan.”

Deficits and Affordability Tool | The Budget Lab

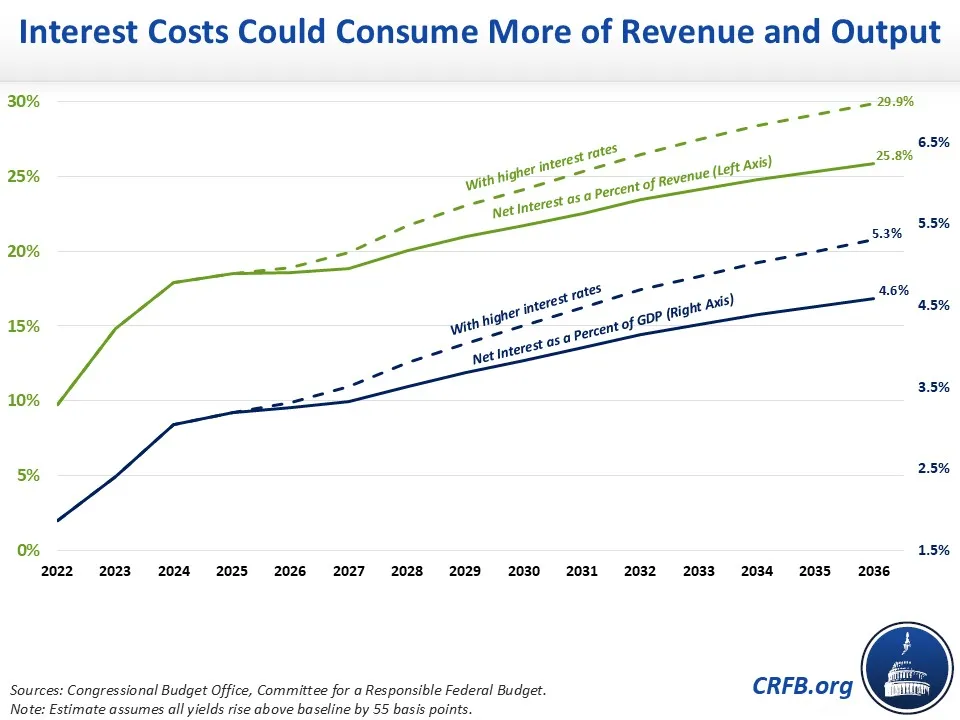

Also recently, economist and commentator Noah Smith has pointed to high interest rates and payments as a reason for debt concern. Although in 2022 Smith thought interest rates would decline, by 2023 he “was starting to worry a lot more” and by 2025 his “mounting alarm turned to full-blown panic.” In his piece, Smith points out that rising interest rates and debt both boost federal interest costs, and cites our work showing that these costs will consume a rising share of output and revenue.

Smith explains that neither Federal Reserve rate cuts nor artificial intelligence will save us from a debt spiral, and Japan’s experience with high debt offers little comfort. Smith calls for deficit reduction and cites the idea of embracing a 3% of GDP deficit target as a possible way to recenter the political discussion.

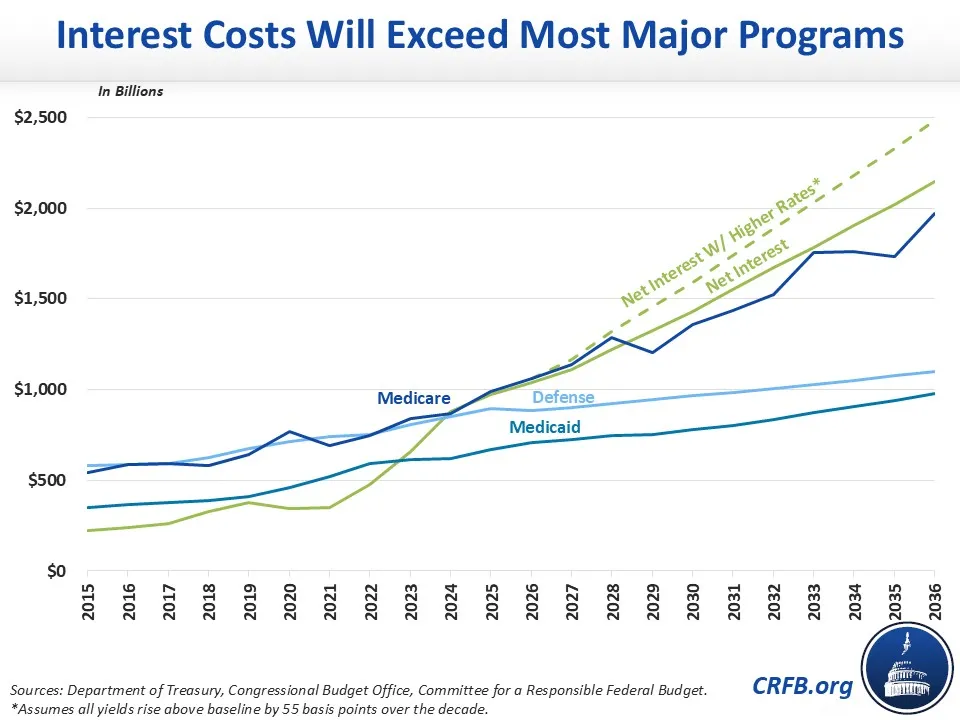

Commentator Matthew Yglesias has similarly expressed concern over rising interest costs in recent months, using CRFB data to show that “interest payments have become larger than Medicaid or the Pentagon and are projected to soar ahead of Medicare.” But Yglesias goes further, sounding the alarm over the impact of deficits and debt on affordability challenges through higher interest rates and inflation in the private sector.

Yglesias also makes the political case for focusing on the debt, explaining how it opens the door for embracing the populist desires to tax the rich and cut wasteful spending while also helping address affordability challenges by reducing inflation and interest rates.

Only a few years ago, all seven of these experts believed deficit concerns were significantly overblown and some even called for larger structural deficits. Today, they recognize that, in combination with higher inflation and interest rates, the fiscal situation has made debt too large to ignore. Evidently, even fiscal doves are now sounding the alarm on the national debt.

As Yglesias puts it, “it’s high time that policymakers start taking this seriously.”