Maya MacGuineas: Here's How to Fix Social Security

Maya MacGuineas is president of the Committee for a Responsible Federal Budget. She recently wrote an opinion piece for The Dallas Morning News, the third in a four-part series about the Social Security program and its long-term financial issues. The full text can be found below.

Social Security is a big deal. Its benefits make up the majority of income for more than 40% of seniors, and the tax it imposes is the largest for most Americans. Addressing the retirement program’s pending insolvency therefore poses an immense challenge that requires navigating difficult tradeoffs, but also an enormous opportunity to make the program serve Americans’ needs and hopes even better.

First, let’s clarify what we’re up against. The Social Security retirement program is projected to go insolvent in less than seven years — almost a quarter of the time most retirees have spent paying off their mortgage. Policymakers must act soon to save Social Security, not only to prevent an $18,400 annual benefit cut for a typical couple, but also to secure the program for future generations.

But it’s not too late to act. Thoughtful reforms can strengthen retirement security, improve predictability for seniors, promote healthy and productive aging, bolster economic growth, improve efficiency and reduce income inequality. Even if Social Security wasn’t staring down the barrel of a crisis, these would be good reasons to reform the program.

A solvent Social Security program would allow workers and retirees to rest assured in the knowledge that they will receive Social Security benefits, helping them make better long-term choices about work and savings.

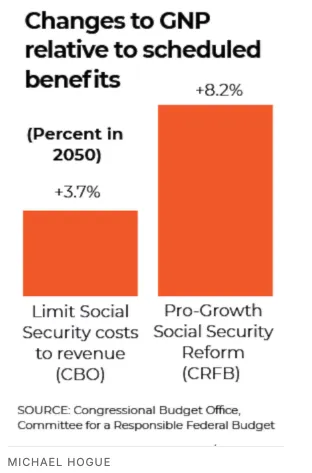

A balanced Social Security program would also make us all collectively richer. According to estimates from the Congressional Budget Office, limiting Social Security’s costs to its revenue would increase per-person incomes by nearly 4% by 2050. If achieved using a pro-growth reform package like one my organization proposed in 2019, per-person incomes could rise by more than 8%.

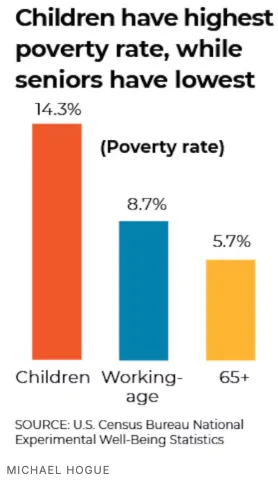

Smart reform would also address income inequality. Today’s seniors represent the wealthiest cohort in the history of the nation. They also have the lowest poverty rate of any age group by far. Yet under current law, Social Security pays the very highest-income retired couples more than $100,000 per year — over five times the senior poverty threshold — paid for in part by taxes on low- and middle-class wage earners.

The current benefit formula pays those with high lifetime earnings more than lower earners. Policymakers could adjust that formula to make it more progressive or flat.

They could also cap Social Security’s cost-of-living adjustments so that the wealthiest seniors get the same benefit increase as less wealthy seniors. And they could increase revenue collection from high-income workers, for example, by lifting the $184,500 cap on income subject to the payroll tax or replacing the employer’s half of the payroll tax with a much broader Employer Compensation Tax (ECT).

Social Security reform could also improve retirement decisions. Policies like raising the retirement age and counting all years of work equally when calculating initial benefits could improve solvency while also facilitating a smoother transition. Those who are able to delay their retirement or seek more flexible alternatives to abruptly exiting the labor force would do so in response to smart incentives.

As life expectancy grows, delayed retirement can help seniors boost their retirement income by increasing their earnings and shrinking the time spent relying on retirement savings. According to one study, the difference could be 10% for every year of delay.

Policymakers can also reform Social Security’s family benefits so that they are fairer and better target the most vulnerable seniors. For example, Social Security’s spousal benefit could be made less generous for spouses of high-income workers while benefits for widows and widowers, who are most at risk of falling into poverty, could be boosted.

My organization’s online Social Security Reformer tool details several potential reform options and shows how they would impact Social Security’s solvency. The problem isn’t a lack of good options; the problem is a lack of political will. In the end, there are many ways that policymakers can fix Social Security. What is most important is that they act, and quickly.

Read the entire piece here.

Published works by members or staff of the Committee for a Responsible Federal Budget do not necessarily represent the views of all members or staff of the Committee.