Making Trust Funds Solvent Would Substantially Reduce Debt Growth

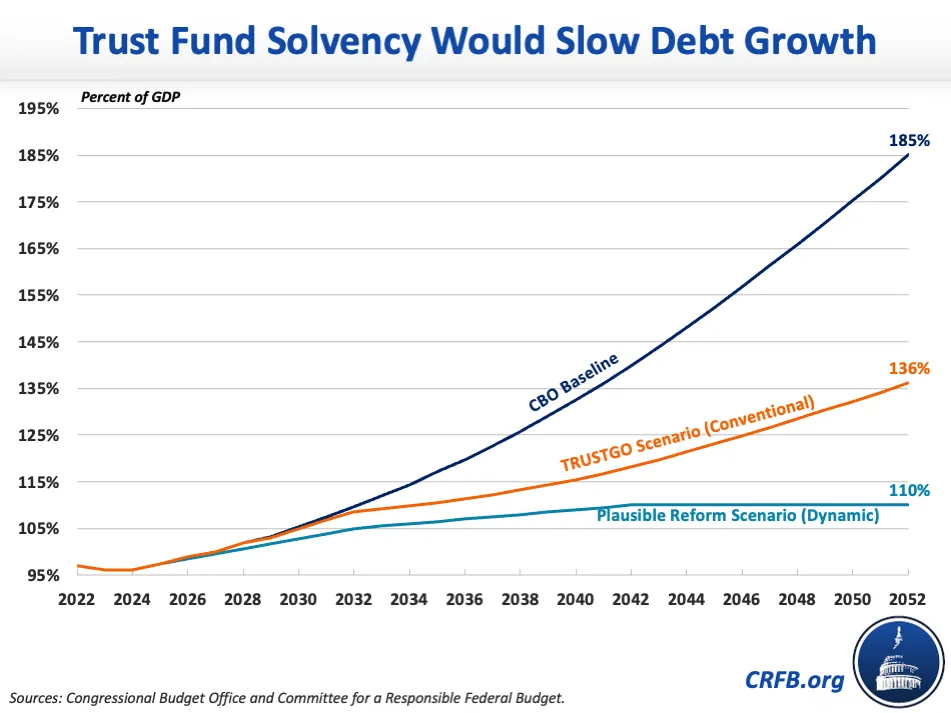

In July, the Congressional Budget Office (CBO) projected that federal debt held by the public would nearly double as a share of the economy over three decades, from a near-record 96 percent of Gross Domestic Product (GDP) in 2023 to 185 percent of GDP by 2052. These projections assume current law spending on Social Security, Medicare, and highways continue after the programs' trust funds deplete their reserves. Restoring solvency to these trust funds would substantially improve the long-term fiscal outlook.

We estimate that a TRUSTGO baseline – which assumes no trust fund borrowing is allowed – would slow the growth of debt held by the public to 136 percent of GDP by 2052 on a conventional basis. Were policymakers to enact thoughtful pro-growth reform measures to trust fund programs well before their insolvency dates, debt would be much lower. Although we have not formally estimated the effects of such reforms, they could plausibly stabilize the debt at as low as 110 percent of GDP on a dynamic basis, which accounts for faster economic growth. Importantly, none of these estimates account for the worsened fiscal outlook since CBO's July report, which would increase debt in both the baseline and trust-fund solvency scenario.

In its baseline, CBO projected the Highway Trust Fund would become insolvent in Fiscal Year (FY) 2027 (after a general revenue transfer authorized in the bipartisan infrastructure law), the Medicare Hospital Insurance trust fund would become insolvent in FY 2030, and the combined Social Security trust funds would reach insolvency in calendar year (CY) 2033. Though current law would require automatic cuts to bring trust fund spending in line with revenue, CBO essentially assumes that lawmakers will transfer general revenue as needed to prevent any cuts. Therefore, making changes to reduce trust fund spending or increase revenue directly would reduce debt relative to CBO's baseline.

| Trust Fund | Insolvency Date | Deficit at Insolvency Date |

|---|---|---|

| Highway Trust Fund | FY 2027 | $37 billion (0.1% of GDP) |

| Hospital Insurance Trust Fund | FY 2030 | $50 billion (0.1% of GDP) |

| Social Security Trust Funds | CY 2033 | ~$500 billion (1.3% of GDP) |

Source: Congressional Budget Office.

Our TRUSTGO scenario assumes lawmakers act to bring trust fund spending in line with revenue the year each trust fund is expected to become insolvent. On a conventional basis that does not account for economic effects, debt would continue to increase as a share of GDP under this scenario but much more slowly than under current law. By 2032, debt would reach 109 percent of GDP instead of 110 percent. By 2042, it would reach 118 percent of GDP instead of 140 percent. And by 2052, it would reach 136 percent of GDP as opposed to 185 percent under current law. In other words, more than half of the projected debt accumulation over the next 30 years would be erased under the TRUSTGO scenario.

Accounting for economic impacts and assuming actual reform packages are implemented, debt could be even lower in 2052. Earlier action on Social Security and Medicare, which is important in its own right to allow people time to plan and adjust, would lead debt growth to slow sooner and allow the economic and fiscal benefits to accrue more quickly. Moreover, pro-growth reforms that lower debt, support work, encourage savings, improve taxes, and lower health costs can lead to higher federal revenue and a larger GDP. Although we have not modeled recent reform packages, we believe it's possible to stabilize debt at about 110 percent of GDP with the right set of trust fund program reforms.

Making trust funds solvent would significantly improve the budget outlook while providing certainty for the beneficiaries who rely on these programs. Lawmakers should work on solutions to make these trust funds solvent over the long term rather than papering over shortfalls as they did with the infrastructure law.