Q&A: Everything You Should Know About the Debt Ceiling

This paper has been updated.

The federal debt ceiling was raised in December of 2021 by $2.5 trillion to $31.381 trillion, which is expected to last until at least January of 2023. At that point, the Treasury Department may begin using accounting tools at their disposal, called “extraordinary measures,” to avoid defaulting on the government’s obligations, which should allow for continued borrowing through at least June. At the point of exhaustion of those measures, absent a new agreement to either raise or suspend the debt ceiling, the Treasury will be unable to continue paying the nation’s bills. Congress could address the debt ceiling through reconciliation, which provides for passage of legislation with a simple majority vote in the Senate.

- What is the debt ceiling?

- When was the debt ceiling established?

- How much has the debt ceiling grown?

- Why is Congress debating this now?

- What are extraordinary measures?

- Can hitting the debt ceiling be avoided without Congressional action?

- What happens if the debt ceiling is hit?

- How bad are the consequences of a default?

- How does a shutdown differ from a default?

- Have policymakers used the debt ceiling to pursue deficit reduction in the past?

- What should policymakers do?

- What are the options for improving the debt ceiling?

- Where can I learn more?

- Appendix: Examples of How the Debt Ceiling Has Been Used in the Past

What is the debt ceiling?

The debt ceiling is the legal limit on the total amount of federal debt the government can accrue. The limit applies to almost all federal debt, including the roughly $24.3 trillion of debt held by the public and the roughly $6.9 trillion the government owes itself as a result of borrowing from various government accounts, like the Social Security and Medicare trust funds. As a result, the debt continues to rise due to both annual budget deficits financed by borrowing from the public and from trust fund surpluses, which are invested in Treasury bills with the promise to be repaid later with interest.

When was the debt ceiling established?

Prior to establishing the debt ceiling, Congress was required to approve each issuance of debt in a separate piece of legislation. The debt ceiling was first enacted in 1917 through the Second Liberty Bond Act and was set at $11.5 billion to simplify the process and enhance borrowing flexibility. In 1939, Congress created the first aggregate debt limit covering nearly all government debt and set it at $45 billion, about 10 percent above total debt at the time.

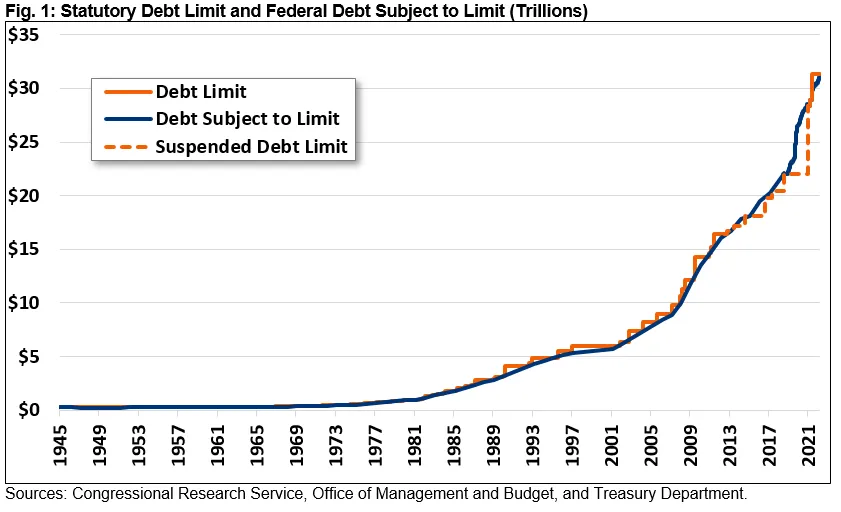

How much has the debt ceiling grown?

Since the end of World War II, Congress and the President have modified the debt ceiling roughly 100 times. During the 1980s, the debt ceiling was increased from less than $1 trillion to nearly $3 trillion. Over the course of the 1990s, it was doubled to nearly $6 trillion, and in the 2000s it was again doubled to over $12 trillion. The Budget Control Act of 2011 automatically raised the debt ceiling by $900 billion and gave the President authority to increase the limit by an additional $1.2 trillion (for a total of $2.1 trillion) to $16.39 trillion. Lawmakers have suspended the debt limit, rather than raising it by a specific dollar amount, seven times since February 2013. The debt limit was increased – not suspended – twice in 2021, mostly recently in a December 2021 bill that formally increased the limit to $31.381 trillion.

Why is Congress debating this now?

The debt ceiling increase enacted in late 2021 is expected to sustain federal borrowing authority into the first quarter of 2023. Given that the 117th Congress is coming to an end, it is unclear when and how the 118th Congress – no matter which party controls either chamber – decides to address the debt ceiling in 2023.

Once the debt ceiling reaches $31.381 trillion, the U.S. government will not be able to issue any new debt. In the past, the government has been able to continue to meet its obligations in the short term using so-called “extraordinary measures,” which provide for shifting certain funds around such as suspending the sale of certain government securities.

Neither the Treasury nor the Congressional Budget Office (CBO) has issued a formal report on when Congress must enact debt limit legislation in 2023 to avoid wide-reaching consequences of not being able to meet its obligations in full and on time, often known as the “X date.” Outside groups that closely track the debt ceiling, however, have estimated that the X date could arrive no earlier than the third quarter of 2023, which would begin in July.

What are extraordinary measures?

When the debt limit is reached, the Treasury Department uses a variety of accounting maneuvers, known as extraordinary measures, to avoid defaulting on the government’s obligations. For example, the Treasury has prematurely redeemed Treasury bonds held in federal employee retirement savings accounts (and replaced them later with interest), halted contributions to certain government pension funds, suspended state and local government series securities, and borrowed from money set aside to manage exchange rate fluctuations. The Treasury Department first used these measures in 1985, and they have been used on at least 16 occasions since then.

Can hitting the debt ceiling be avoided without Congressional action?

The Treasury Department’s use of extraordinary measures simply delays when the debt will reach the statutory limit. Spending in excess of incoming receipts has already been legally obligated; that spending will push debt beyond the ceiling. There is no plausible set of changes that could generate the instant surplus necessary to avoid having to raise or suspend the debt ceiling.

Some believe the Treasury Department could buy more time by engaging in other unprecedented actions such as selling large amounts of gold, minting a special large-denomination coin, or invoking the Fourteenth Amendment to override the statutory debt limit. Whether any of these tools is truly available is in question, and the potential economic and political consequences of each of these options are unknown. Realistically, once extraordinary measures are exhausted, the only option to avoid defaulting on our nation’s obligations is for Congress to change the law to raise or suspend the debt ceiling.

What happens if the debt ceiling is hit?

Once the government hits the debt ceiling and exhausts all available extraordinary measures, it is no longer allowed to issue debt and soon after will run out of cash-on-hand. At that point, given annual deficits, incoming receipts would be insufficient to pay millions of daily obligations as they come due. Therefore, the federal government would have to at least temporarily default on many of its obligations, from Social Security payments and salaries for federal civilian employees and the military to veterans’ benefits and utility bills, among others.

So-called “prioritization” of payments, or making sure certain obligations among the more than 80 million that get paid per month are paid before others – such as servicing debts to bondholders before making other payments in order to avoid technical default – has been criticized as unrealistic by Treasury officials and economists. A Treasury Inspector General report from 2012 outlined scenarios that were considered during the 2011 debt ceiling run-up and found that delay of payments, which suspended all government payments until they could all be paid on a day-to-day basis, was the least harmful scenario.

A default, or even the perceived threat of one, could have serious negative economic implications. An actual default would roil global financial markets and create chaos, since both domestic and international markets depend on the relative economic and political stability of U.S. debt instruments and the U.S. economy. Interest rates would rise, and demand for Treasuries would drop as investors stop or scale back investments in Treasury securities if they are no longer considered perfectly safe, thereby increasing the risk of default. Even the threat of default during a standoff increases borrowing costs. The Government Accountability Office (GAO) estimated that the 2011 debt ceiling standoff raised borrowing costs by a total of $1.3 billion in Fiscal Year (FY) 2011, and the 2013 debt limit impasse led to additional costs over a one-year period of between $38 million and more than $70 million.

If interest rates for Treasuries increase substantially, interest rates across the economy would follow, affecting car loans, credit cards, home mortgages, business investments, and other costs of borrowing and investment. The balance sheets of banks and other institutions with large holdings of Treasuries would decline as the value of Treasuries dropped, potentially tightening the availability of credit as seen most recently in the Great Recession.

How bad are the consequences of default?

A Moody’s Analytics report released in September 2021 estimated that a default could have similar macroeonomic consequences to the Great Recession: a 4 percent Gross Domestic Product (GDP) decline, nearly 6 million lost jobs, and an unemployment rate of 9 percent. In addition, Moody’s predicted a $15 trillion loss in household wealth, with stocks dropping by as much as one-third at the depths of the selloff.

The White House Council of Economic Advisers (CEA) has warned that the macroeconomic effects stemming from default – or even getting too close to one – can last months or even years. A CEA report found that following the debt limit run-up in 2011, mortgage rates rose 0.7 to 0.8 percentage points for two months following the crisis and rates for auto and other consumer loans also remained elevated for months. In the event of an actual default, increased unemployment rates could persist for two to four years, the report warned.

How does a shutdown differ from a default?

A shutdown occurs when Congress fails to pass appropriations bills that allow agencies to obligate new spending. As a result, the government temporarily stops paying employees and contractors who perform government services (see Q&A: Everything You Should Know About Government Shutdowns). However, many more parties are not paid in a default. A default occurs when the Treasury does not have enough cash available to pay for obligations that have already been made. In the debt ceiling context, a default would be precipitated by the government exceeding the statutory debt limit and being unable to pay all its obligations to its citizens and creditors. Without enough money to pay its bills, any of the payments are at risk, including all government spending, mandatory payments, interest on our debt, and payments to U.S. bondholders. While a government shutdown would be disruptive, a government default could be disastrous.

Have policymakers used the debt ceiling to pursue deficit reduction in the past?

Although policymakers have often enacted “clean” debt ceiling increases, Congress has also coupled increases with other legislative priorities. In several cases, Congress has attached debt ceiling increases to budget reconciliation legislation and other deficit reduction policies or processes.

Indeed, most of the major deficit reduction agreements made since 1980 have been accompanied by a debt ceiling increase, although causality has moved in both directions. On some occasions, the debt limit has been used successfully to help prompt deficit reduction, and in other cases, Congress has tacked on debt ceiling increases to deficit reduction efforts. For example, the 2011 Budget Control Act was enacted along with a debt ceiling increase, as was the Gramm-Rudman-Hollings Balanced Budget and Emergency Deficit Control Act of 1985.

In nearly all instances in which a debt limit increase was either accompanied by deficit reduction measures or included in a deficit reduction package, lawmakers have generally approved temporary increases in the debt limit to allow time for negotiations to be completed without the risk of default. For example, Congress approved a modest increase in the debt limit in December of 2009 while negotiations over Statutory Pay-As-You-Go (PAYGO) and the establishment of the National Commission on Fiscal Responsibility and Reform were ongoing. Similarly, during the negotiations and consideration of the 1990 budget agreement, Congress approved six temporary increases in the debt limit before approving a long-term increase as part of the reconciliation bill implementing the deficit reduction agreement.

The Appendix contains further discussion of provisions attached to debt ceiling legislation, including bills in 1993, 1997, 2013, 2015, 2018, and 2019.

What should policymakers do?

Policymakers should work promptly to raise or suspend the debt ceiling by the deadline. Failing to raise the debt ceiling would be disastrous. It would result in severe negative consequences that experts are not capable of predicting in advance. Even threatening a default or taking the country to the brink of default could have serious implications. Importantly, though, failing to control the national debt would also have negative consequences; rising debt could ultimately stunt economic growth, reduce fiscal flexibility, and increase the cost burden on future generations. Thus, lawmakers should consider accompanying a debt ceiling increase with measures to begin addressing the debt.

To be sure, political advantage should not be sought by threatening default, and the debt ceiling must be raised or suspended. Lawmakers must not jeopardize the full faith and credit of the U.S. government. At the same time, the need to raise the debt ceiling can serve as a useful moment for taking stock of our fiscal state and for pursuing revenue increases, entitlement reform, and/or spending reductions.

What are the options for improving the debt ceiling?

Increasing the debt ceiling requires frequent and often contentious legislative action. While several increases have been used to enact fiscal reforms, many increases are not necessarily tied to fiscal health. For instance, debates regarding the debt ceiling often take place after the policies producing the debt have already been put in place. The debt ceiling also measures gross debt, which means that even if the budget was balanced, the debt ceiling would still have to be raised if surpluses accumulated in government trust funds like Social Security.

In The Better Budget Process Initiative: Improving the Debt Limit and subsequent publications, we have suggested reforms to the debt ceiling, grouped in four major categories:

- Linking changes in the debt limit to achieving responsible fiscal targets, so that Congress would not need to increase the debt ceiling if fiscal targets are met.

- Having debate about the debt limit when Congress is making decisions on spending and revenue levels, not after those decisions have been made.

- Applying the debt limit to more economically meaningful measures, such as debt held by the public or debt as a share of GDP.

- Replacing the debt limit with limits on future obligations.

Where can I learn more?

- Committee for a Responsible Federal Budget – Understanding the Debt Limit

- Committee for a Responsible Federal Budget – Improving the Debt Limit

- Bipartisan Policy Center – Debt Limit Analysis

- Bipartisan Policy Center – Debt Limit “X Date” Further Out Than Expected, But Still Looms Ahead

- Government Accountability Office – Debt Limit: Analysis of 2011-2012 Actions Taken and Effect of Delayed Increase on Borrowing Costs

- Government Accountability Office – Debt Limit: Market Response to Recent Impasses Underscores Need to Consider Alternative Approaches

- Congressional Research Service – The Debt Limit

- Congressional Research Service – The Debt Limit Since 2011

- Congressional Research Service – Reaching the Debt Limit

- Congressional Research Service – Debt Limit Suspensions

- Federal Reserve – Possible Macroeconomic Effects of a Temporary Federal Debt Default

- Moody’s Analytics – Playing a Dangerous Game with the Debt Limit

- Treasury Department – Frequently Asked Questions About the Public Debt

- Treasury Department – Description of Extraordinary Measures, August 2021

- Treasury Department – The Potential Macroeconomic Effect of Debt Ceiling Brinkmanship

- Treasury Office of the Inspector General -- Response by the Chair of the Council of Inspectors General on Financial Oversight and Inspector General of the Department of the Treasury, August 2012

- White House Council of Economic Advisers – The Debt Ceiling: An Explainer

- White House Council of Economic Advisers – Life After Default

Appendix: Examples of How the Debt Ceiling Has Been Used in the Past

The Gramm-Rudman-Hollings Act in 1985: The Gramm-Rudman-Hollings Act (GRH) in 1985 raised the debt limit by $175 billion and set a target to have a balanced budget by 1991, with across-the-board cuts in spending by sequestration designed as an enforcement mechanism. Although the deficit reduction goals under GRH were not fully achieved, the experience gained under the act contributed to the development of more workable and effective procedures five years later.

The Balanced Budget and Emergency Deficit Control Reaffirmation Act of 1987: This bill, also known as Gramm-Rudman-Hollings II, was passed to correct constitutional deficiencies in the 1985 Gramm-Rudman-Hollings Act. Like its predecessor, GRH II attached a deficit reduction measure to the increased debt limit, requiring automatic sequester if deficits did not meet annual targets.

Omnibus Budget Reconciliation Act of 1990: The Omnibus Budget Reconciliation Act (OBRA) of 1990 raised the debt limit by $915 billion, the largest increase up until that point, but it also contained nearly $500 billion in deficit reduction over the next five years. Additionally, it created enforcement procedures in the Budget Enforcement Act (BEA), which helped lead to budget surpluses in the late 1990s. The BEA also created adjustable limits for separate categories of discretionary spending and the pay-as-you-go (PAYGO) procedure that required tax cuts or increases in mandatory spending to be offset. Congress approved six temporary increases in the debt limit while negotiations to implement the budget agreement were ongoing.

Omnibus Budget Reconciliation Act of 1993: The Omnibus Budget Reconciliation Act of 1993 raised the debt limit by $600 billion, an increase that lasted for about two and a half years. OBRA '93 was the second major deficit reduction package of the 1990s, also containing nearly $500 billion in deficit reduction over five years. The agreement extended the original spending caps from 1990 and raised taxes on high earners, among other reforms.

Line Item Veto Act of 1996: The Line Item Veto Act of 1996 gave the President authority to veto specific provisions in legislation that increased the federal deficit, increased entitlement spending over the baseline, created tax benefits, or allocated discretionary budget authority. This practice, known as a line-item veto, was ruled unconstitutional by the Supreme Court for violating the separation of powers clause by allowing the President to amend a statute without Congress voting on it. While the 1996 line-item veto was found unconstitutional, other versions of it have been presented, including one by President Bush that would have allowed him to cancel spending obligations using his existing rescission authority.

Balanced Budget Act of 1997: The Balanced Budget Act of 1997 included a $450 billion debt limit increase that, thanks to the surpluses of the late 1990s and early 2000s, was enough to cover debt until 2002. At the time, the legislation called for about $125 billion of net deficit reduction over five years and $425 billion over ten years. It did so mainly through reductions in health care spending via provider payment reductions and increased premiums. The Act also created a few new programs – Medicare+Choice (later renamed Medicare Advantage or Medicare Part C) and the State Children’s Health Insurance Program (CHIP).

Statutory PAYGO Act of 2010: The Statutory PAYGO Act of 2010 contained a debt limit increase of $1.9 trillion, the largest nominal increase ever enacted until that point in time. In exchange for the debt limit increase, this legislation included a budget process reform that reinstituted statutory PAYGO procedures that require tax cuts and mandatory spending increases to be fully offset (with some exemptions). Informally, the agreement to raise the debt ceiling also led to the creation of a National Commission on Fiscal Responsibility and Reform (also known as the Simpson-Bowles commission).

Budget Control Act of 2011: The Budget Control Act (BCA) gave the President the authority to increase the debt limit in tranches – subject to a Congressional motion of disapproval – by a total of $2.1 trillion. The BCA also contained $917 billion in deficit reduction over ten years, primarily through caps on discretionary spending. In addition, the bill established the Joint Committee on Deficit Reduction (“Super Committee”) to produce deficit reduction legislation of at least $1.2 trillion in savings, without which budget sequestration would begin in 2013 as a consequence of the Super Committee failing to succeed. The Super Committee did not produce such legislation, resulting in years of budget sequestration. The bill also required Congress to vote on a Balanced Budget Amendment, which did not pass.

No Budget, No Pay Act of 2013: Lawmakers enacted the No Budget, No Pay Act in early February 2013, which temporarily suspended the debt ceiling through May 18, 2013 and then set an automatic “catch up” on May 19 that allowed for a $300 billion increase in the debt ceiling. The agreement would have also withheld the pay of Members of Congress if no budget resolution was passed in each House (though there was no requirement that the resolution be agreed to jointly, which is necessary to adopt a single Congressional budget.).

Default Prevention Act of 2013: The Default Prevention Act of 2013 ended a 16-day partial shutdown of the federal government by funding the government through January 15, 2014 and suspending the debt ceiling until February 7, 2014. This agreement set up a bicameral budget conference to reconcile budgets for FY 2014 and provided for an automatic “catch up” on February 7. On that date, the debt ceiling was reinstated at the current level of borrowing, resulting in a de facto increase of about $500 billion and bringing the debt ceiling to $17.2 trillion.

Bipartisan Budget Act of 2015: This bill suspended the debt limit through March 15, 2017 and provided an automatic “catch up” to account for borrowing up to that point that will effectively raise the debt limit by $1.8 trillion to its current level of $19.8 trillion. The bill also enacted “sequester relief” by raising the statutory caps on defense and nondefense discretionary spending for FY 2016 and FY 2017 (partially offset by mandatory savings) and averted insolvency of the Social Security Disability Insurance Trust Fund by reallocating payroll tax revenues.

Bipartisan Budget Act of 2018: This bill suspended the debt limit through March 1, 2019 and provided for an automatic “catch up” to account for borrowing up to that point that will effectively raise the debt limit by $1.5 trillion to its anticipated level of approximately $22 trillion. The bill also raised statutory caps on defense and nondefense discretionary spending in 2018 and 2019 beyond the original 2011 caps. Little of the bill’s cost was offset; it ultimately will add $418 billion to the debt after ten years, after accounting for increased interest costs.

Bipartisan Budget Act of 2019: This bill suspended the debt limit through July 31, 2021, and provided for an automatic “catch up” to account for the borrowing up to that point. That will effectively raise the debt limit by $6.5 trillion to its anticipated level of approximately $28.5 trillion. The bill also raised statutory caps on defense and nondefense discretionary spending in 2020 and 2021 by about $320 billion. Only a portion of the bill’s cost was offset; it ultimately will add $1.7 trillion to the debt over ten years after accounting for longer-term increases to baseline discretionary spending levels stemming from the bill.

Note: An earlier version of this analysis mistakenly flagged July as the month the U.S. would hit the debt limit rather than the month extraordinary measures might run out. This was corrected on January 13, 2023.