The Case for a 3% of GDP Deficit Target

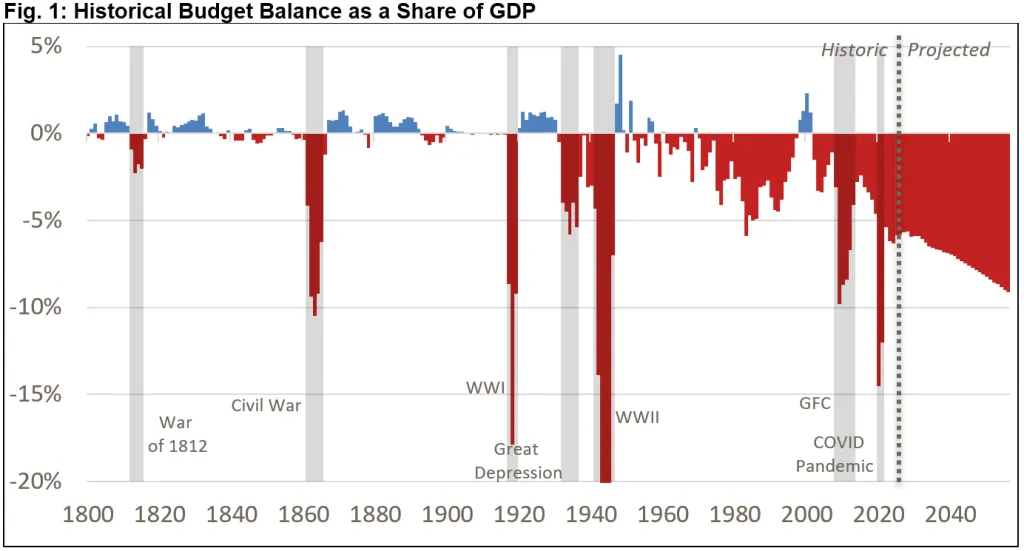

As the debt approaches record levels as a share of the economy, the United States government continues to run the highest peacetime deficits in the nation’s history, outside of a recession or emergency. With the budget deficit approaching 6% of Gross Domestic Product (GDP) this year and growing toward 7% of GDP by the end of the decade, the national debt is projected to rise from about 100% of GDP today to 120% by 2036 and to 175% within 30 years. Such high and rising debt would have damaging economic, fiscal, and geopolitical consequences.

Lawmakers should adopt and then work to achieve a fiscal target to put the nation on a more sustainable fiscal path. A reasonable target called for by the Board of Directors of the Committee for a Responsible Federal Budget would reduce annual deficits to 3% of GDP, cutting deficits in half relative to current level.

The case for a 3% deficit-to-GDP target is strong. In this piece, we explain:

- A Fiscal Target Can Support Fiscal Discipline: Regardless of the specific target, establishing a fiscal goal can create a “guiding light” for budgetary and fiscal policy decisions as well as a benchmark for evaluating progress.

- A 3% Deficit Target Would Put Debt on a Sustainable Path: A sustainable fiscal outlook requires debt to grow slower than the economy. With nominal economic growth projected to total 3.5% to 3.8% per year, 3% deficits would put the debt-to-GDP ratio on a downward path with a bit of wiggle room.

- A 3% Deficit Target is Ambitious but Achievable: Reducing deficits to 3% of GDP would target a metric largely in Congress’s control and requires only about half as much savings as balancing the budget.

- A 3% Deficit Target Has Bipartisan Support and International Precedent: The 3% target is supported by policymakers, business leaders, and experts across the political spectrum. Dozens of countries, including those in the European Union, target 3%; many more countries have similar or lower targets.

- Policymakers Should Set and Enforce Interim Targets: Deficit reduction should begin immediately and phase in gradually, with annual targets and a meaningful process to facilitate and enforce the needed deficit reduction.

A 3% of GDP deficit target offers a credible and achievable path forward to stabilizing the debt, growing the economy, preserving fiscal flexibility, and bolstering market confidence in the nation’s finances. Adopting such a target must not be a replacement for enacting necessary and long-overdue tax and spending adjustments. It should instead be viewed as an important step toward enacting these policies and putting the budget on a sustainable course.

A Fiscal Target Can Support Budget Discipline

In the U.S. and around the world, governments have set fiscal targets to help guide budgetary choices. Although simply setting a fiscal target cannot force the policy changes necessary to achieve the fiscal metric, it can anchor fiscal discussions by providing a clear benchmark against which lawmakers can weigh policy decisions and assess progress. A fiscal goal also narrows the parameters of political discussion, shifting focus from whether and how much to reduce deficits to how and how urgently such deficit reduction should occur.

Through most of U.S. history up until the early 2000s, the country had an unofficial fiscal target of balancing the budget.1 Outside of major wars or recessions, policymakers generally worked to bring spending and revenue in line. Although the budget regularly fell short of balance, deficits through the 19th and 20th centuries averaged only 1.4% of GDP outside of major wars and the Great Depression. Meanwhile, nearly every Presidential and Congressional budget included a plan to return to balance.2

Sources: Committee for a Responsible Federal Budget, Congressional Budget Office, Office of Management & Budget.3

That unofficial fiscal target was abandoned in the early 2000s, and so too was any semblance of fiscal responsibility. Between 2001 and 2025, debt tripled as a share of the economy from 32% of GDP to roughly 100%. The 1% of GDP surplus in 2001 turned into a 6% of GDP deficit last year.

Simply restoring a fiscal target – any reasonable fiscal target – could help policymakers pursue efforts to reduce deficits and resist calls to expand them. Around the world, over 100 countries have adopted some form of fiscal target; in the U.S., 49 states have. Once lawmakers agree to set a fiscal target, the next step is to determine which one. A 3% deficit target is a reasonable choice.

A 3% Deficit Target Would Put Debt on a Sustainable Path

In setting a fiscal target, policymakers could focus on annual deficits, primary (non-interest) deficits, spending, revenue, and/or overall debt. Regardless of that choice, they should select a target that is credible, realistic, and sufficient to meaningfully improve the fiscal outlook.

Reducing deficits to 3% of GDP would achieve the goal of putting the national debt on a sustainable course. With the current debt-to-GDP ratio of 100%, stabilizing the debt requires running annual deficits-to-GDP below the nominal rate of economic growth – which the Congressional Budget Office (CBO) projects at 3.5% to 3.8% per year in the coming decades.4

A deficit target of 3% of GDP holds annual borrowing comfortably below this expected economic growth rate, putting debt on a slow downward path and leaving space for economic downturns or other external shocks that could temporarily lower GDP growth and/or boost deficits.

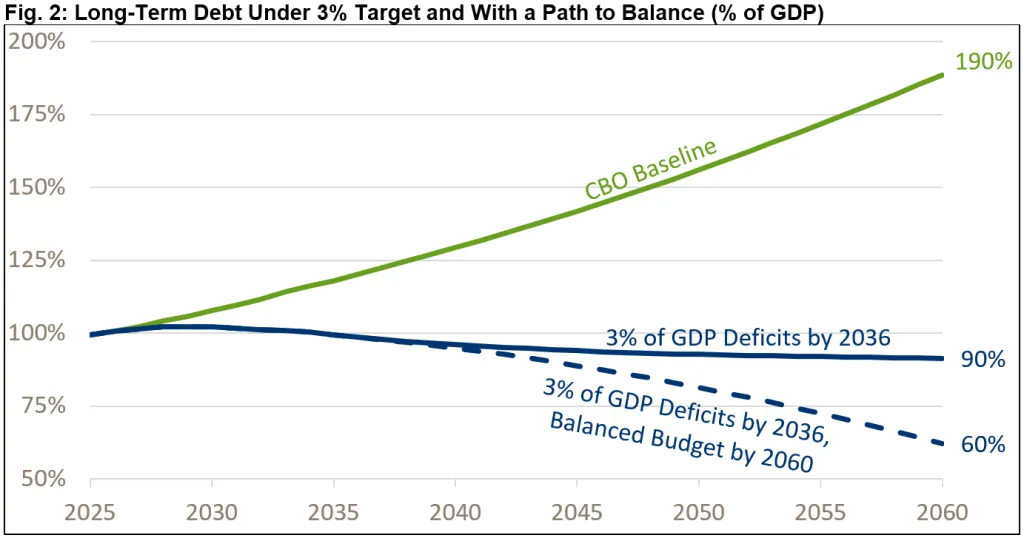

Assuming lawmakers gradually reduce deficits to 3% of GDP by 2036 and beyond, we estimate debt would remain around its current level over the next decade and fall to about 90% of GDP by 2060. If lawmakers continue to reduce deficits beyond 2036, reaching balance by 2060, debt would fall to 60% of GDP. By comparison, debt is projected to rise to 190% of GDP under CBO’s baseline.

Sources: Committee for a Responsible Federal Budget, Congressional Budget Office.5

Because declining debt would significantly reduce interest payments (both by reducing debt and putting downward pressure on interest rates) and boost economic growth, successfully achieving the target would leave more room in the future for further deficit reduction – or alternatively, spending or tax relief – and in all cases support an even further decline in debt-to-GDP.6

3% Deficits are Achievable

A 3% of GDP deficit target would maintain fiscal sustainability and is more achievable than other desirable targets such as balancing the budget or significantly reducing the debt-to-GDP ratio.

Deficit targets can be achieved with changes to outputs largely under policymakers’ control. Future budget deficits are determined mainly by future revenue collection and primary spending levels, both of which can be set by Congress.7 Future debt levels, by comparison, are determined largely by past debt levels. A one-time temporary surge in borrowing (for example, to fight a war) would only modestly boost future deficits due to higher interest costs – but it would significantly increase future debt levels in a way that could make returning to a debt target challenging.

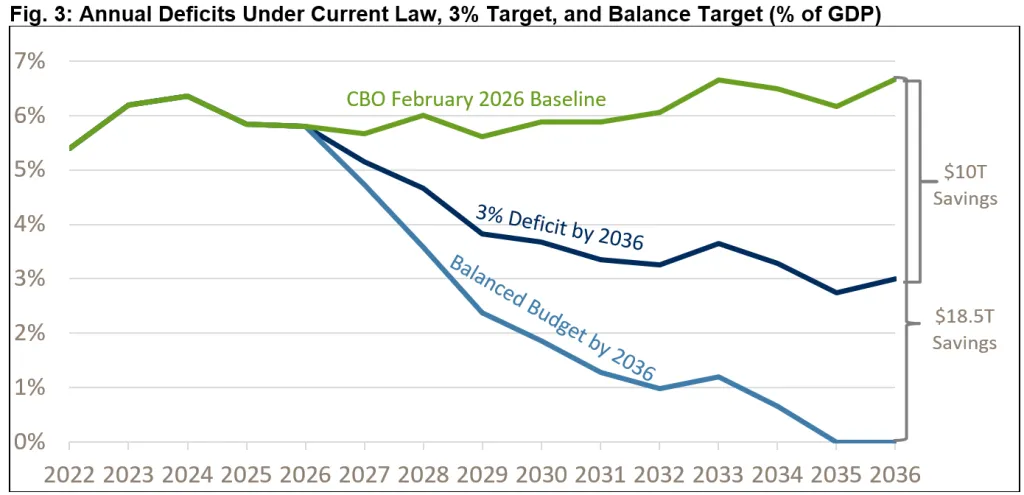

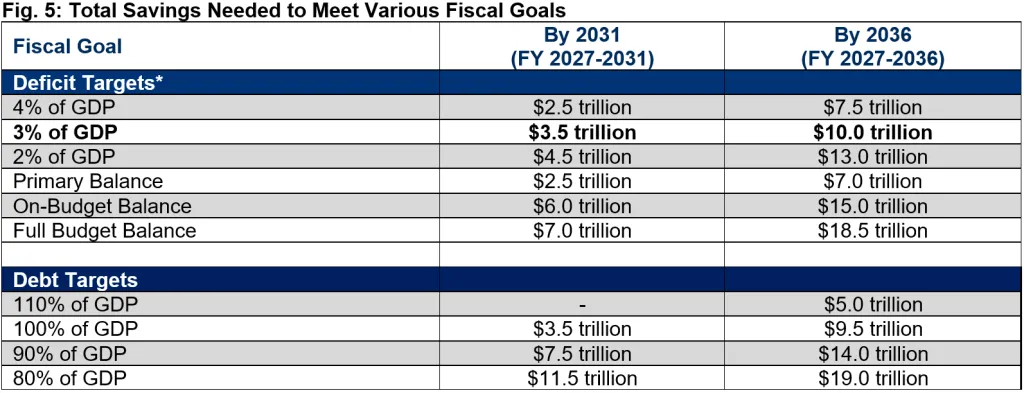

Targeting 3% of GDP deficits is also far more achievable than balancing the budget. A 3% of GDP deficit would require cutting today’s deficit in half rather than eliminating it. The country ran deficits of less than 3% as recently as 2015, whereas the budget has not been balanced since 2001.

Achieving a 3% of GDP deficit by 2036 would require about $10 trillion of deficit reduction over a decade – the equivalent of reducing primary spending by 11% or increasing revenue by 12%. Balancing the budget, by comparison, would require closer to $18.5 trillion in ten-year savings – the equivalent of reducing primary spending by 20% or increasing revenue by 23%.

Sources: Committee for a Responsible Federal Budget, Congressional Budget Office.8

To be sure, even a 3% deficit target would require ambitious policy change to meaningfully boost revenue and reduce spending – but such policy changes are within reach. Policymakers could get half way to the target by securing the Social Security, Medicare, and highway trust funds; discretionary spending caps, health care reforms, new revenues, and other cuts to spending and tax breaks could bring the budget the remainder of the way to the 3% target.9

The 3% of GDP Target Has International Precedent and Bipartisan Support

Dozens of countries around the world target a deficit at or below 3% of GDP, including members of the East African Community (EAC) and Monetary Union (EAMU), the West African Economic and Monetary Union (WAEMU), and the European Union (EU).

Indeed, the 3% target was established by the 1992 Maastricht Treaty, the founding treaty of the European Union. It was most recently reaffirmed by the 2024 updates to the EU’s Stability and Growth Pact. EU countries that breach the 3% threshold, or a parallel 60% of GDP debt target, are subject to “excessive deficit procedures” and required to develop a plan for fiscal correction.

The 3% of GDP deficit target also has broad and significant domestic support. The 3% target was the official medium-term goal of the National Commission on Fiscal Responsibility and Reform (the Simpson-Bowles Commission). It was supported by the Obama Administration in the 2010s. And it has the support of some members of the current Trump Administration, most notably Treasury Secretary Scott Bessent.

Within Congress, resolutions have been introduced in both the House and the Senate stating that Congress should adopt a deficit target of 3% of GDP and Congressional and Presidential budgets should include plans to achieve this target. The House Budget Committee held a hearing on the 3% deficit-to-GDP fiscal target, which it described as “the best metric to reverse the curse.” And although it relies entirely on unspecified savings, the most recent Congressional budget resolution targets 3% annual deficits.

The 3% target also has significant support outside of Congress. Last fall, the 36-member Board of Directors of the Committee for a Responsible Federal Budget issued an open letter calling on lawmakers to adopt a 3% of GDP deficit target. That call has been echoed by a range of former government officials who served in the Reagan, Bush, Clinton, Bush, Obama, Trump, and Biden Administrations; and by numerous policy experts, including from the Progressive Policy Institute, Third Way, the Bipartisan Policy Center, the Economic Policy Innovation Center, the National Taxpayers Union, and elsewhere.

The 3% target also has the support of business and thought leaders, including Ray Dalio, Warren Buffett, and others. And it has been endorsed by the Editorial Boards of the Washington Post, Bloomberg, and the Las Vegas Review Journal.

Support for the 3% deficit target is not political, partisan, or ideological. Because the target could be met by any combination of higher revenue, lower spending, and stronger economic growth (though plausibly, growth on its own will not be sufficient), it has broad support on the left, right, and center. Although there is significant disagreement over how to reduce deficits to sustainable levels, there is broad agreement on the need for this deficit reduction and growing support for the 3% target in particular.

Policymakers Should Set Interim Targets Toward the 3% Goal

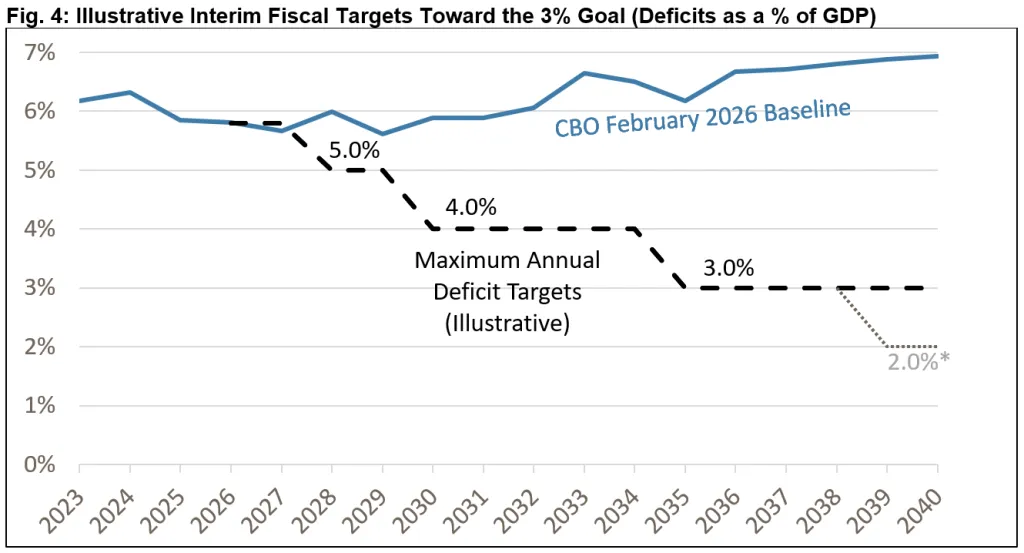

It will likely take several years to reduce deficits to 3% of GDP, so policymakers will need to set the 3% target for some year in the future. To ensure they are on course to achieve the 3% target, lawmakers should set interim targets along the way.

Although deficit reduction can occur gradually, it is important that policymakers begin to make progress toward the goal immediately and continue to make progress over time. Policymakers should put deficits on a downward path toward the 3% target, not rely on cliffs, late policy changes, or heroic assumptions that may never come to pass.

As an illustrative example, policymakers could establish targets limiting deficits to below 6% in 2027, below 5% by 2028, below 4% by 2030, and below 3% by 2035. Actual deficits would likely decline in smaller and more frequent increments than these targets but might rise and fall from year to year due to a variety of economic, policy, and payment timing factors.10

Sources: Committee for a Responsible Federal Budget, Congressional Budget Office. *With path to balance by 2060.

For the 3% of GDP target to be most effective it should be codified into law, have enforcement mechanisms, and use the most credible economic assumptions available. While targets on their own can help to push the fiscal conversation forward, legislative “teeth” are needed to give the targets credibility and ensure they are met.

One option borrowed from our Break Glass plan would put a freeze on indexing throughout the budget and tax code and impose a deficit reduction surtax if targets are not met. A fast-track process could also be established for the development and passage of deficit reduction policies.

Conclusion

The U.S. fiscal situation is on an unsustainable path, which threatens to slow economic growth, increase the cost of living, boost interest payments, reduce fiscal space, compromise national security, and increase the chance of a fiscal crisis. Corrective action should be taken sooner rather than later to slow the growth of the debt and bring spending and revenue more closely in line.

As a step toward addressing the fiscal outlook, lawmakers should establish a fiscal target and then work to enact the necessary policy changes to achieve that target.

Although there is no one “correct” fiscal target, a reasonable goal, endorsed by the Board of Directors of the Committee for a Responsible Federal Budget, would be to gradually reduce deficits to 3% of GDP or lower. A 3% of GDP deficit target would be sufficient to put debt on downward path with policy changes that are ambitious but achievable. It has broad international precedent and domestic support – including from policymakers, business leaders, and experts of all political persuasions. And recently, Members of Congress in both parties and both chambers have been rallying around the 3% of GDP deficit target.

In setting the 3% fiscal target, lawmakers should establish a set of interim targets to ensure that progress begins immediately while changes can phase in fully over time. They should also establish a set of processes and enforcement mechanisms to help lawmakers meet the 3% target.

Reducing deficits to 3% of GDP will require significant deficit reduction – about $10 trillion over a decade if the target is reached by 2036. Fortunately, a wide range of existing policy options offer lawmakers a menu of possibilities for improving the nation’s fiscal outlook. The challenge is not a lack of solutions but the political will to pursue them and to reach bipartisan agreement.

The recent endorsement of a 3% of GDP deficit target by numerous lawmakers is encouraging. Now policymakers should work to codify a target into law. And with that benchmark established, policymakers should act with urgency to enact the necessary deficit reduction as soon as possible.

Appendix I: Potential Fiscal Targets and Savings to Achieve Them

There is no one “correct” fiscal target. Policymakers could target deficits or debt. They could target total debt or annual balances. They could target deficits as a share of GDP, primary (non-interest) or full balance, or debt as a share of the economy. And they could aim to hit those metrics after five years, ten years, or another time frame.

Depending on the path of the savings, reducing deficits to 3% of GDP within five years would require $3.5 trillion over that time period. Reducing them to 3% of GDP within ten years would require $10 trillion. By comparison, it would take $7.0 trillion of ten-year savings to achieve primary balance after a decade, $9.5 trillion to stabilize the debt at 100% of GDP, and $18.5 trillion to balance the budget by 2036.

Sources: Congressional Budget Office and the Committee for a Responsible Federal Budget. *Actual deficit reduction would vary dependent on savings path. Estimates above assume savings path consistent with offsets from the One Big Beautiful Bill Act (OBBBA) through 2032, extrapolated with additional policy extensions and assumptions through 2036. Figures are rounded to the nearest $500 billion.

Appendix II: Letter from the CRFB Board on a 3% of GDP Deficit Target

Endnotes

1 Bill White, America’s Fiscal Constitution: Its Triumph and Collapse, 2014 (New York: Public Affairs) details the limits on federal borrowing that existed for two centuries and how this fiscal constitution collapsed at the turn of the 21st century.

2 Budgets put forward by Presidents Kennedy, Johnson, Nixon, Ford, Reagan, H.W. Bush, Clinton, and W. Bush proposed balancing the budget or running surpluses by the end of the budget window.

3 Deficits prior to 1930 are rough CRFB estimates that assume deficits are equal to changes in debt. See CBO, August 2010, “Historical Data on Federal Debt Held by the Public.”

4 Against CBO’s current ten-year baseline, we estimate annual deficits would need to be about 10 basis points below the annual growth rate to hold debt exactly steady as a share of GDP. Deficits need to be below rather than at the growth rate for two reasons. First, GDP growth is based on prior year output whereas the deficit-to-GDP ratio is measured relative to current year GDP. And secondly, debt is projected to grow most years by slightly more than annual deficits due to the use of “accrual accounting” in some parts of the budget such as the student loan program.

5 The “3% of GDP Deficits” scenario assumes deficits decline to 3% of GDP by 2036 and then stay there through 2060. “3% of GDP Deficits by 2036, On Path Toward Balance” assumes deficits decline to 3% of GDP by 2036 and then decline at a slower, linear rate to 0% by 2060.

6 Higher levels of debt “crowd out” investment, and in the process put upward pressure on interest rates and downward pressure on economic growth. For example, see the CBO, 2024, “How the Expiring Individual Income Tax Provisions in the 2017 Tax Act Affect CBO’s Economic Forecast,” Duygu Yolcu Karadam, 2024, “An Investigation of Nonlinear Effects of Debt on Growth,” Thomas Laubach, 2009, “New Evidence on the Interest Rate Effects of Budget Deficits and Debt,” Yongquan Cao, Vitor Gaspar, and Adrian Peralta-Alva, 2024, “Costly Increases in Public Debt when r < g.” As a corollary, debt reduction puts downward pressure on interest rates and accelerates economic growth. For a given nominal level of deficits and debt, larger GDP means lower deficit-to-GDP and debt-to-GDP levels. And for a given deficit-to-GDP ratio, a higher rate of GDP growth means ultimately lower debt-to-GDP levels.

7 Deficits are also significantly influenced by interest costs and economic output, over which policymakers have much less control.

8 Estimates assume savings begin in FY 2027 and follow a path similar to offsets in the 2025 One Big Beautiful Bill Act, with certain temporary deficit reduction measures extended on a permanent basis. Different assumptions on timing could result in different ten-year savings estimates.

9 In 2022, the Committee for a Responsible Federal Budget released “The CRFB Fiscal Blueprint for Reducing Debt and Inflation“ which provided a comprehensive deficit-reduction framework. At the time, we estimated the Blueprint would reduce the deficit to 3.4% of GDP by 2032 before considering dynamic effects. If enacted today, it is likely this Blueprint would achieve the 3% of GDP deficit target by the end of the decade. See Committee for a Responsible Federal Budget, October 2022, “The CRFB Fiscal Blueprint for Reducing Debt and Inflation.”

10 Deficits in a given fiscal year can be influenced by the precise timing of payments that might occur near the beginning or end of a year. The specific dates of weekends or holidays can shift costs between fiscal years, causing reported deficits to bounce up and down even if experienced deficits are relatively steady. Because timing shifts lower reported deficits in 2035, a plan to achieve the 3% target in 2036 is likely to also achieve or perhaps overachieve the target in 2035.