Extending the Student Loan Payment Pause is Bad Policy

Note: (8/30/2022): Since the publication of this blog the Biden Administration announced another four-month extension to the student loan pause through December 2022. We released a new blog, available here, with the estimated cost of the pause and distributional effects through December 2022.

A new report in Bloomberg suggests that President Biden is nearing a decision that could extend the student loan payment pause through the end of the year or even to next summer. Doing so would be costly, regressive, and inflationary, adding up to $60 billion to the deficit, boosting the inflation rate by up to 20 basis points, and delivering most of the benefits to high-income households and individuals with advanced degrees.

Extending the Student Debt Pause is Costly

Through a combination of executive and legislative action, most borrowers have not been required to make payments on their student debt for the past 28 months, and no interest has accrued over that time.

Between the repayment pause through August 2022, targeted debt cancellation, and changes to income-driven repayment rules, increases in student debt relief have cost the federal government nearly $300 billion over the past two-and-a-half years. Most of those costs are from executive actions under the Biden Administration.

We estimate that extending the student loan payment pause through the end of the year would cost $20 billion and extending through August 2023 would cost $60 billion. This would bring the total cost of the student loan pause alone to nearly $200 billion and total debt relief to close to $350 billion. By comparison, cancelling $10,000 per borrower of debt outright would cost $250 billion.

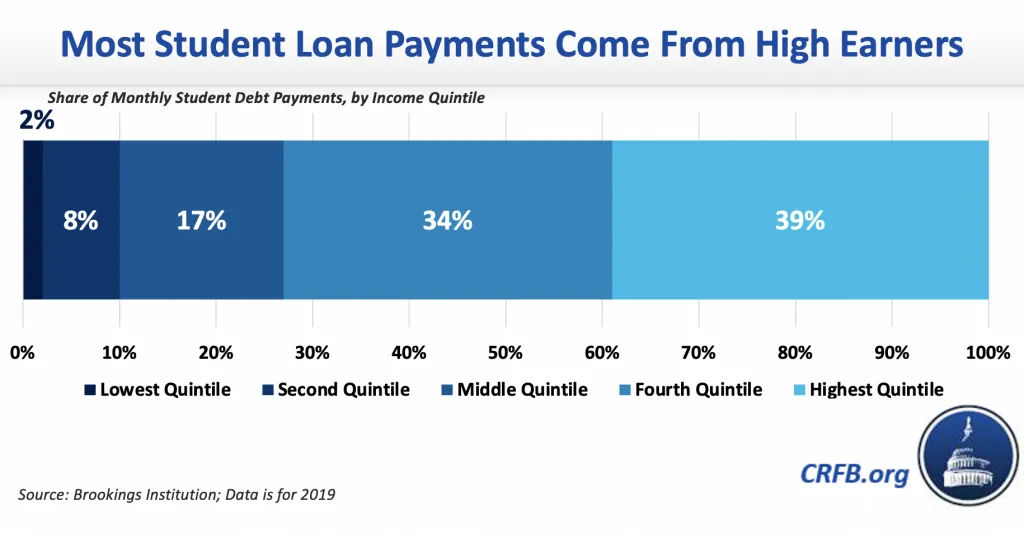

Continuing the Pause is Regressive

The student debt pause continues to be an extremely regressive policy, and each month the pause is extended the policy becomes more cumulatively regressive. The vast majority of the benefit goes to those with college degrees, who currently have an unemployment rate of 2.1 percent. In a typical year, about two-fifths of payments are made by households in the top quintile and only 2 percent by those in the bottom quintile. Of course, many people who don’t make any payments are likely towards the bottom of the income distribution, and they still benefit from not having interest accrue on their loans. However, they receive a relatively small benefit compared to a graduate school student with a high level of debt who was making active payments, making the policy as a whole regressive.

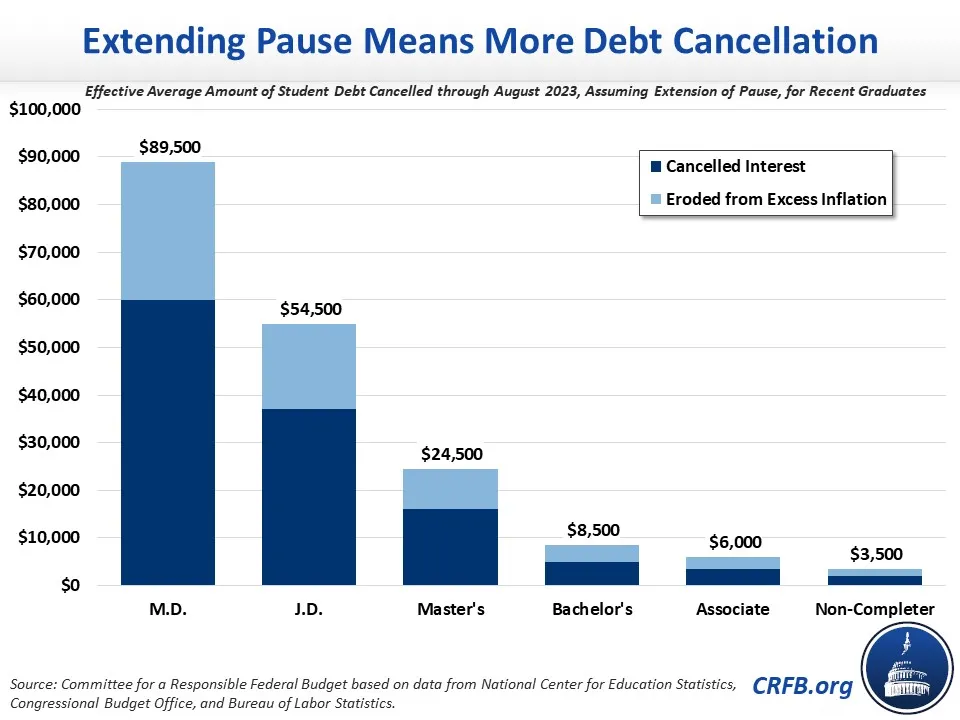

By stopping interest accumulation, the student debt pause effectively cancels some debt. High rates of inflation have further eroded that debt, which is paid at fixed interest rates. Using the same methodology as in our previous analysis, we estimate that since the pause began in March 2020 and should it continue through August 2023, a typical recent medical school graduate will effectively receive nearly $90,000 of debt cancellation (from the pause and inflation), a recent law school graduate will get $55,000 of cancellation, and a recent master’s degree recipient will get $25,000. At the same time, a recent bachelor’s degree recipient will get $8,500 of debt cancellation, someone who just completed an associate degree will receive $6,000, and a person who was unable to complete their undergraduate degree will get $3,500.

Those who have been repaying their debt for several years will have received less debt relief, but we expect the relative comparison to be similar.

Continuing the Repayment Pause is Inflationary

By not requiring about 20 million borrowers to make monthly payments when they likely would be otherwise, the debt pause increases household cash on hand, leading to stronger demand in an already overheated economy.1 As a result, extending the repayment pause will worsen inflation relative to what would otherwise happen.

In a previous analysis, we estimated that continuing all ongoing COVID relief at the time, including the debt pause, Medicare sequester, and enhanced Medicaid payments to states, would boost the Personal Consumption Expenditures (PCE) inflation rate by 14 to 68 basis points. The student debt pause alone could contribute 20 basis points to the PCE inflation rate.

Though this inflationary pressure is relatively modest on its own, it will make the Federal Reserve’s job of preventing persistent inflation without engineering a recession even more challenging. With the inflation rate already at a four-decade high, fiscal policy should be helping the Fed to bring inflation down, not working against the Fed’s efforts.

Time to Get Serious About Student Loans

As we’ve explained before, blanket debt cancellation would be a big mistake. Extending the current student debt pause isn’t a form of inaction; it’s debt cancellation by another name. And as we’ve shown before, it’s even more regressive than cancelling $10,000 per person.

As the Department of Education continues to issue $85 billion a year of new loans, failure to collect on existing loans threatens the integrity of the entire program while adding to federal costs and worsening inflationary pressures.

It’s time to restart loan repayments and get serious about meaningful higher education reform.

1 While there 43 million federal student loan borrowers, only about 20 million were “in repayment” before the pandemic. We expect that will roughly be the same number of people paying after the restart. Due to certain actions by the administration, those “in repayment” may be temporarily higher, but it’s not clear if more people will actually be making payments.

What's Next

-

Image

-

Image

-

Image