What Does Student Debt Cancellation Mean for Federal Finances?

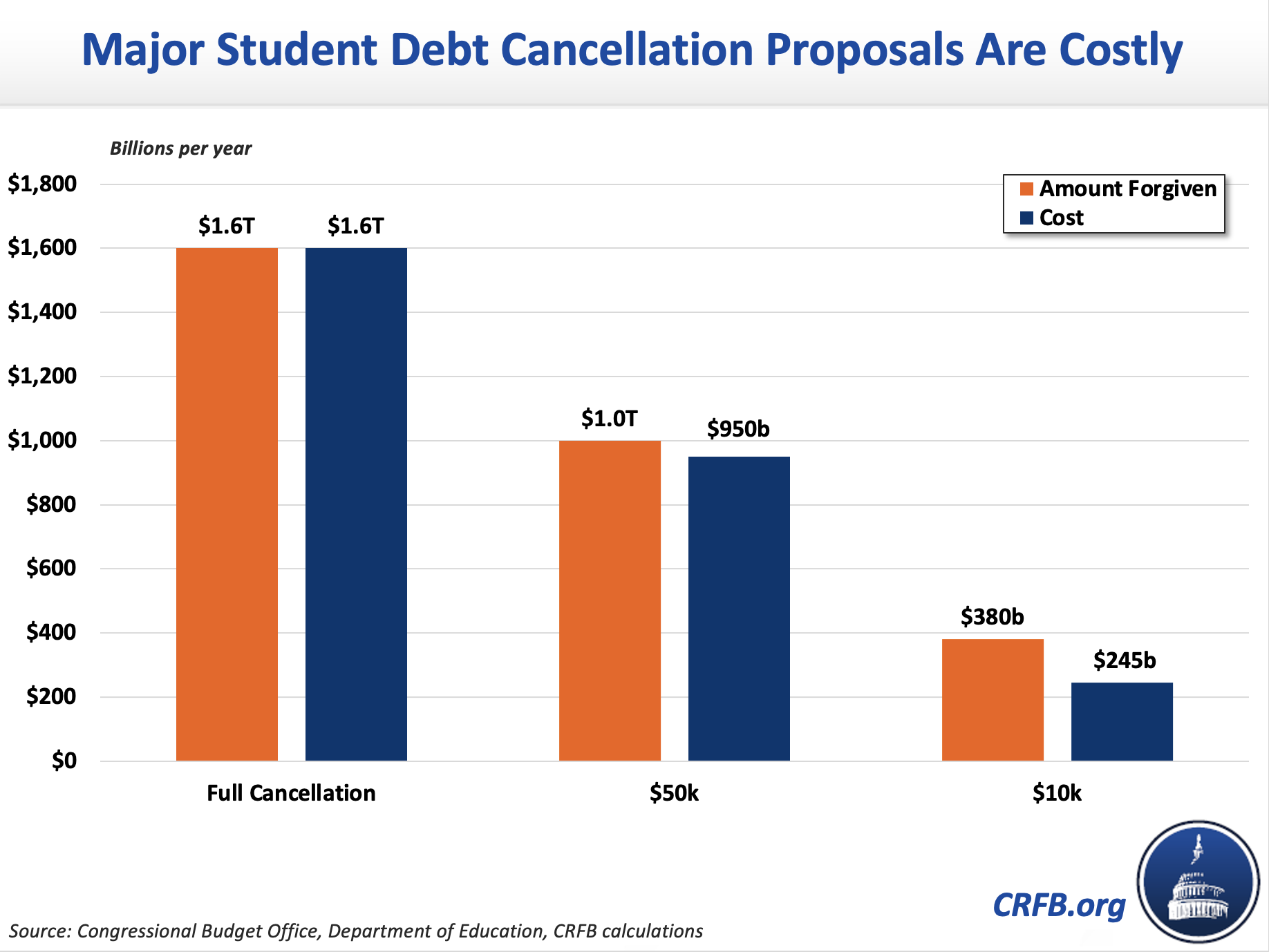

We've previously estimated that cancelling all federal student debt would cost the same as the outstanding value of the loans, which is currently $1.6 trillion. Cancelling up to $50,000 of debt per borrower would cost around $950 billion and cancelling up to $10,000 would cost roughly $245 billion. What “cost” actually means is confusing and often misunderstood, however, since the government has already lent out these dollars and the deficit and debt impacts are calculated using different accounting standards. This piece explains why and how it costs the government money to cancel federal student loan debt.

In short, forgiving student debt would be very costly for the federal government. Those costs are recorded as deficit impact immediately and would immediately reduce the value of government asset holdings. They would also be reflected in higher future debt levels, but this debt accumulation would occur only gradually.

The total cost of student debt forgiveness is similar but not equal to the amount of outstanding debt that is cancelled. From a financial perspective, debt forgiveness would immediately increases federal debt net of financial assets. From a cash flow perspective, it cuts off a source of government receipts by reducing the amount of loan principal and interest paid to the federal government on a monthly basis. In no scenario is debt cancellation costless for the federal government.

How Does the Government Calculate the Cost of Student Loans?

Most federal spending is effectively accounted for on a “cash basis” – meaning each new dollar that goes out the door without an equivalent offset increases deficits and debt by one dollar, and each dollar received by the federal government and not used to finance new spending reduces deficits and debt by that same amount.

Loans are treated differently. While each dollar lent by the federal government does add to the near-term debt, the deficit impact is calculated on an accrual basis. Specifically, the government records the loan based on the expected lifetime cost to the government on a present-value basis. If the government expects a loan to be paid back in full with interest, the cost of the loan would be recorded as zero (or potentially even as a source of savings). On the other hand, if the government offers a more favorable interest rate or expects some portion of the loan will not paid back, it records the difference as a cost.

On average, the government estimates most newly issued student debt will generate a slight net savings – basically enough to cover administrative costs. While the federal government heavily subsidizes undergraduate “subsidized loans,” CBO estimates that loans issued to parents generate substantial revenue.1

While the expected cost of, or savings from, the loan is recorded in the deficit when issued, those costs and savings are not fully realized until the loan term is complete. When loan repayments or underlying variables deviate from initial projections, revisions are incorporated into new deficits estimates. For example, in 2021 the Office of Management and Budget (OMB) updated its assumptions about the incomes of borrowers enrolled in income-driven repayment plans and determined the existing student loan portfolio will end up costing $53 billion more than it originally estimated. This reflects that fewer of the loans will be paid back than originally expected.

What Does Student Debt Cancellation Mean for Federal Finances?

The ultimate cost of debt cancellation to the federal government is equal to the amount of debt that is cancelled plus any expected interest payments to the government, minus the cost of borrowing for the government, and minus any debt that would have been cancelled or not paid back anyway.

When this cost appears on the federal budget depends on what measure one is looking at. Under current Congressional Budget Office (CBO) and OMB accounting rules, the entire cost of cancellation would be added to the deficit in the year that the student loans are cancelled. Scorekeepers would treat cancellation as a one-time revision to the net present value of government loan holdings.

Similarly, debt cancellation would immediately increase debt net of financial assets. While student loans create debt for the borrower, they are an asset for the federal government just as outstanding loans are an asset for a bank. Cancelling $1 trillion of student debt would immediately reduce federally-held financial assets by $1 trillion. The ultimate cost, reflected in future years, might be slightly higher or lower depending on expected repayments.

However, the federal debt itself would barely change in the first year as a result of debt cancellation. The debt itself was already increased to make the student loans. With cancellation, however, those loans would not be paid back. As a result, cancellation would increase the federal debt over time relative to what it otherwise would have been by removing a source of future government receipts – student loan repayment.

Cost of $1 Trillion of Debt Cancellation, Assuming 20% Subsidy Rate (billions of 2022 NPV dollars)

| Accounting Type | When Cost Appears | Cost Upon Cancellation | Total Cost Over Time |

|---|---|---|---|

| Debt Held by the Public | Over Life of Loan | $0 | $800 billion |

| Debt Net of Financial Assets | Mostly in Cancellation Year | $1 trillion | $800 billion |

| Budget Deficit | In Cancellation Year | $800 billion | $800 billion |

How Much Will Debt Cancellation Cost?

As an example, a $10,000 student loan with an interest rate of 4 percent in a standard repayment plan would yield the federal government roughly $1,200 a year for ten years. Without that repayment, the government would lose $1,200 of receipts per year, adding to the debt over time. This oversimplified example does not account for borrowers who are not expected to fully repay their loans nor the time value of money, but it illustrates clearly that cancelling student debt will impose a cost on the federal government.

While it is relatively straightforward to estimate the amount of debt forgiven under different scenarios, it is more challenging to estimate the net cost to the federal government. Knowing the cost requires estimating how much student debt principal and interest would otherwise be paid back to the federal government and how that compares to the government’s borrowing rate.

On one hand, the fact that student loan interest rates are 2.05 to 4.60 percentage points higher than federal borrowing rates means the federal government could actually make money on student debt – in which case forgiving $1 trillion of debt would cost the federal government more than $1 trillion.

On the other hand, not all student debt will be repaid. Some borrowers will take advantage of existing loan forgiveness programs (for example, from income-driven repayment programs) while others may ultimately default and the government is unable to recover the full amount owed. In addition, the government subsidizes student loans in other ways like through the current student loan repayment moratorium and by waiving interest costs when certain borrowers are in school or are unable to make principal payments in certain income-driven repayment plans. These factors increase the current federal cost of the student loan program and thus reduce the net cost of forgiveness.

CBO estimates new loans currently have a slightly positive subsidy rate, suggesting forgiveness could cost more than the loans forgiven. However, since 2015 OMB and CBO have repeatedly increased the expected cost of the income-driven repayment programs, with the latest reestimate this year increasing the cost of the existing loan portfolio by $53 billion. And an independent estimate by consultants hired by the Trump Administration in 2020 estimated the direct loan portfolio would eventually write off $435 billion in its portfolio. If true, that would mean that debt cancellation would cost much less than the amount of debt cancelled; though it would also mean that the cost of the student loan program each year is far more expensive than currently estimated.

In our previous analyses, we estimated cancelling the full $1.6 trillion of student debt would cost roughly $1.6 trillion. On the other hand, we estimated cancelling $1 trillion of debt by forgiving the first $50,000 per borrower would cost between $675 billion to $1 trillion, while cancelling $380 billion by forgiving the first $10,000 per borrower would cost between $210 billion and $280 billion. We use a mix of purported CBO scores and CBO subsidy rate estimates to surmise that full forgiveness would cost more than partial forgiveness, and that’s likely due to the high rates of default and non-repayment among low-debt borrowers.

These are of course just estimates, and it is impossible to know the exact cost of debt cancellation due to the uncertainty associated with future repayment. But whether measured with deficits, debt, or debt net of financial assets, it is undeniable that broad student debt cancelation will be costly to the federal government.

1 By law, official CBO estimates do not account for “market risk,” and there is debate among experts about whether this is the correct way to measure the cost of student loans. Under an alternative measure known as fair-value accounting, student loans cost an average of 21 cents for each dollar lent out, including 32 cents for subsidized loans.