Maya MacGuineas: The Time to Start Voting About Social Security is Now

Maya MacGuineas is president of the Committee for a Responsible Federal Budget. She recently wrote an opinion piece for the Dallas Morning News, the first in a four-part series about the Social Security program and its long-term financial issues. The full text can be found below.

Social Security is the world’s largest and arguably most important retirement program. It keeps millions of seniors out of poverty and helps support the retirement of tens of millions more. It offers a lifeline to widows and other survivors. It reassures workers that no matter what happens in the stock market, they’ll have some floor of income as they age. And for the past 90 years, Social Security has never missed a full payment. Yet without congressional action, that streak will soon come to an end.

Before Americans go to the polls this election year, it’s more important than ever that they understand the facts about Social Security and the costs they will soon face.

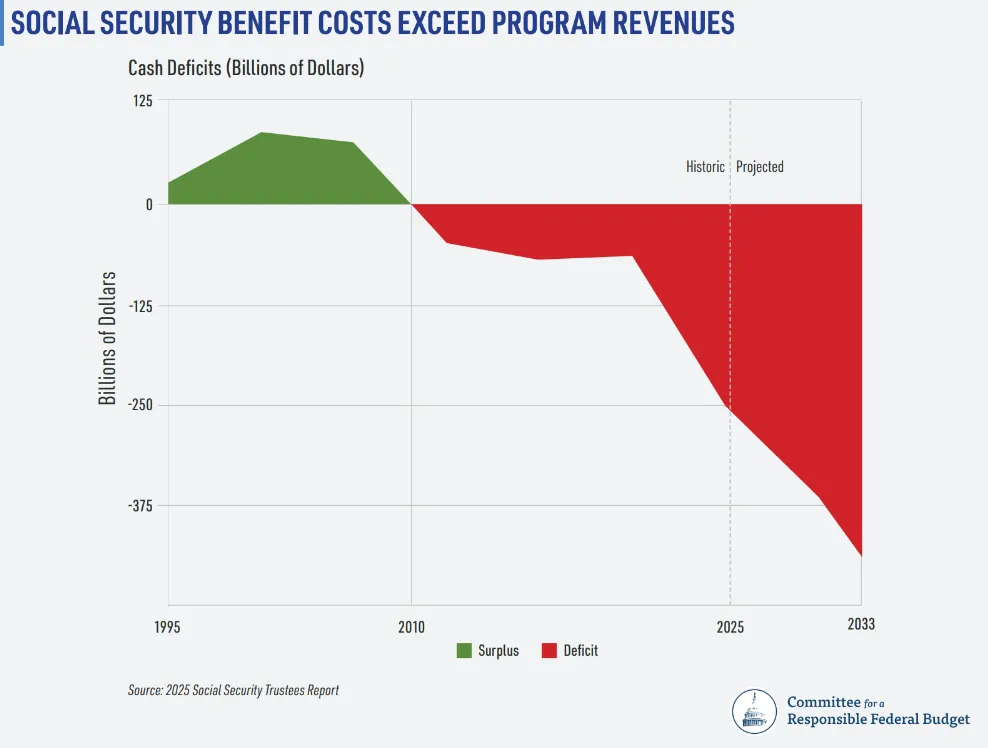

Since 2010, the cost of Social Security benefits has exceeded the revenue coming in from payroll taxes and other sources. This year alone, the retirement program will face a $270 billion cash deficit. The trust fund built from surpluses in the late 1980s, 1990s and early 2000s is waning fast and soon will disappear altogether.

As a result, Social Security is projected to be insolvent in less than seven years. By the end of 2032 — within the term of whoever wins this year’s Texas Senate race — the Social Security trustees project the program will be out of reserves.

At that point, more than 70 million beneficiaries will face a 24% benefit cut, as the law limits benefit payments to the money coming in. For a typical newly retired couple, that’s an $18,400 annual benefit cut.

Upon insolvency, all beneficiaries — even the oldest and the poorest seniors — would face an abrupt cut in benefits. While this would be a shock to those who have come to rely on benefits, it should be of no surprise to those lawmakers who have known this date was coming for four decades now.

So what’s driving the program’s imbalance?

First, and most significantly, the population is aging as a result of growing life expectancy and declining birth rates. Since 1990, the number of Americans over 65 has more than doubled, from 32 million to 65 million, while the rest of the adult population has grown by less than one-third. The senior population is projected to grow nearly another 50% over the next four decades, while the remaining adult population will grow by only about 10%. As the retiree population grows while the payroll tax-paying population stagnates, Social Security is being pushed deeper into deficit.

Social Security’s tax and benefit structure also contributes to the system’s insolvency. Because the benefit formula is wage indexed and the retirement age is fixed, benefits become increasingly generous over time. Meanwhile, payroll taxes have failed to keep up, as a growing share of worker compensation has been paid in non-wage benefits like health insurance, or in wages above the $184,500 tax cap.

Finally, Social Security’s looming insolvency has been driven by the unwillingness of our elected officials to take corrective action. When the program faced financial challenges in the past — notably in 1977 and 1983 — policymakers came together to enact the necessary fixes. But members of both parties have spent the past 40 years ignoring the problem and weaponizing the program by attacking any attempt to fix it from the other side of the aisle.

A pledge not to touch Social Security may be good near-term politics, but it’s an implicit endorsement of a 24% — or $18,400 per-couple — benefit cut. Waiting until the last moment to avoid that cut will leave policymakers with limited options and less ability to phase in changes or give workers time to plan. Plus, waiting will only serve to unnecessarily increase the anxiety of current and future beneficiaries who know what’s coming.

Finding solutions to Social Security’s problems isn’t hard. Many options exist to balance costs and revenue. Thoughtful solutions can strengthen retirement security, accelerate economic growth and improve fairness and efficiency in the process.

The hard part is persuading our leaders to act. False promises, mythical solutions and an unwillingness to confront the problem head-on has made reform impossible to date, but that does not absolve our leaders of their responsibility to act.

Six years is not a long way off — it’s when today’s 61-year-olds reach the normal retirement age and today’s youngest retirees turn 68. That is why, as Texans begin considering who they want to send to Congress next year and to the White House in 2028, candidates should put forward real plans to save Social Security — plans as dependable as the program itself.

Read the entire piece here.

Published works by members or staff of the Committee for a Responsible Federal Budget do not necessarily represent the views of all members or staff of the Committee.