JCT Projects Tax Expenditures Will Be $2.3T in 2026

The Joint Committee on Taxation (JCT) recently published their latest estimates of individual and corporate tax expenditures. In total, JCT projects individual and corporate tax expenditures will equal $2.3 trillion in Fiscal Year (FY) 2026 – up from $2.2 trillion in 2025 – or $11.7 trillion over the five-year period from 2025 through 2029.

Tax expenditures are provisions in the tax code – such as credits or deductions – that either reduce tax liability, increase tax refunds, or both. While they do not technically qualify as outlays, they increase deficits by reducing federal tax revenues and can be generally thought of as spending via the tax code.

The largest tax expenditures are the exclusions for pension contributions and earnings, reduced tax rates on dividends and long-term capital gains, and exclusions for employer-sponsored health insurance. The ten biggest tax expenditures alone will total more than $1.4 trillion in FY 2026, accounting for nearly two-thirds of the cost of all tax expenditures. Importantly, these estimates do not include the revenue effects of tax expenditures on payroll taxes, which can be significant in certain instances, for example with the exclusion for employer-sponsored health benefits.

Largest Tax Expenditures

| Description | 2026 Cost |

|---|---|

| Exclusion for Retirement Savings and Pension Contributions | $355 billion |

| Lower Rates for Dividends and Long-Term Capital Gains | $252 billion |

| Exclusion for Employer-Sponsored Health Insurance | $240 billion |

| Child Tax Credit and Credit for Other Dependents | $128 billion |

| ACA Health Insurance Subsidies | $105 billion |

| Charitable Contributions Deduction | $78 billion |

| Pass-Through Business Income Deduction | $76 billion |

| "Stepped- Up Basis" for Capital Gains at Death | $73 billion |

| Earned Income Tax Credit | $67 billion |

| State and Local Tax Deduction | $60 billion |

Source: Joint Committee on Taxation

JCT’s latest report includes several new tax expenditures that were included in the One Big Beautiful Bill Act (OBBBA), such as the exemptions for tip and overtime income, an additional standard deduction for seniors, and expensing of factories, among others. Many of these expenditures are set to expire after 2028 and therefore have a much smaller revenue impact in 2029.

New Tax Expenditures from the One Big Beautiful Bill Act (OBBBA)

| Description | One-Year Cost (FY 2026) | Five-Year Cost (FY '25- '29) |

|---|---|---|

| Additional Senior Standard Deduction | $22 billion | $91 billion |

| No Taxes on Overtime | $22 billion | $90 billion |

| Expensing of Factories | $14 billion | $80 billion |

| No Taxes on Tips | $7 billion | $29 billion |

| Trump Accounts | $7 billion | $14 billion |

| Deduction for Car Loan Interest | $6 billion | $31 billion |

| Exclusion for Employer Payments of Student Loans | $2 billion | $11 billion |

| Scholarship Tax Credit | $2 billion* | $8 billion |

* Since the new tax credit for contributions to scholarship granting organizations doesn’t take effect until 2027, this figure reflects the FY 2027 cost.

Source: Joint Committee on Taxation

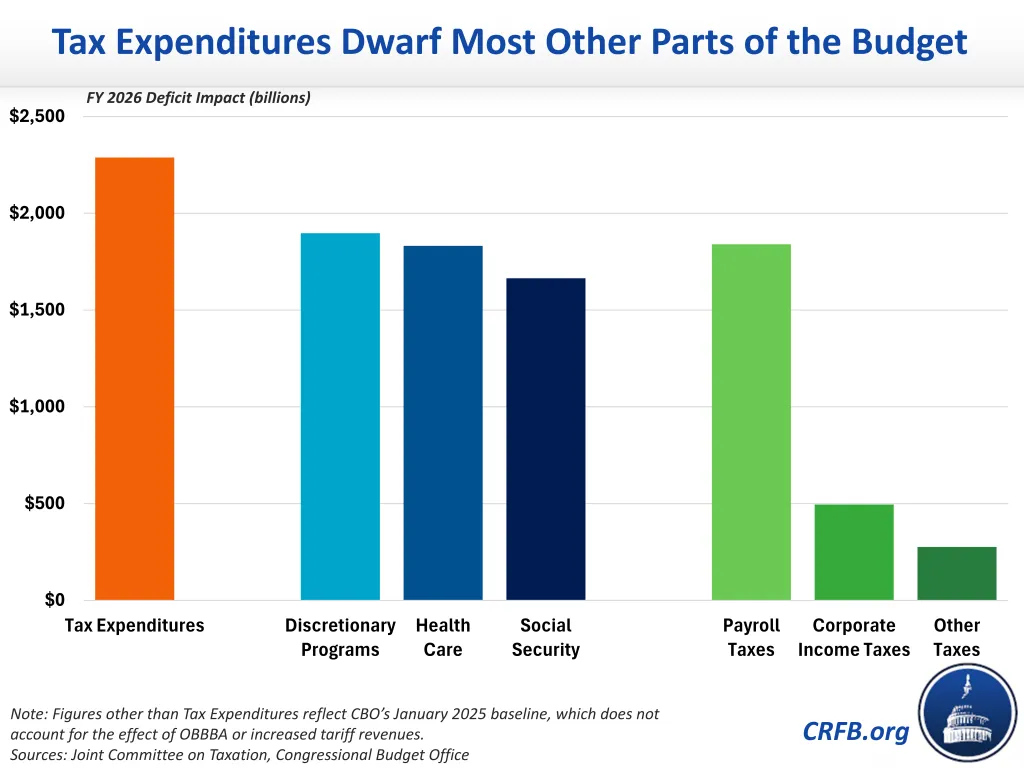

At $2.3 trillion of net deficit impact in FY 2026, tax expenditures are far larger than almost all other parts of the federal budget. They are larger than all discretionary spending programs, all health care programs combined, and Social Security. If they were a line item in the budget, they would be the largest by more than $600 billion.

By comparison on the revenue side, tax expenditures exceed all payroll tax revenues and are more than four-times larger than corporate tax revenues.

Given their outsized impact on the federal deficit, significant deficit reduction could be achieved through reforming and/or eliminating tax expenditures. In many cases, doing so would also reduce market distortions and simplify the tax code. Policymakers should look to tax expenditures for ways to reduce deficits.