CBO Releases June 2023 Long-Term Budget Outlook

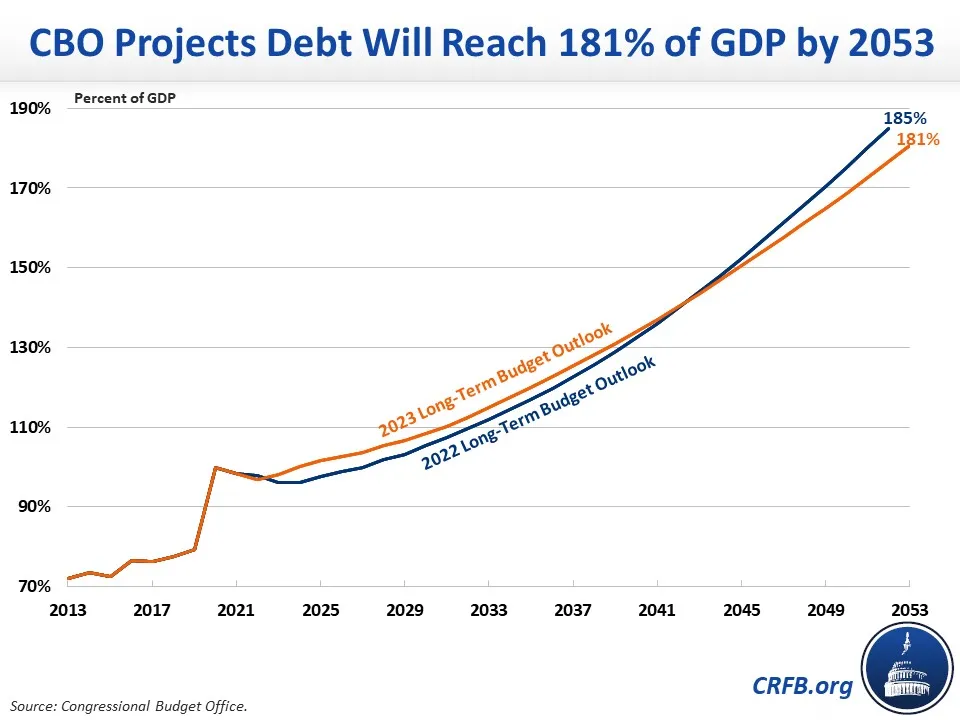

The Congressional Budget Office (CBO) just released its June 2023 Long-Term Budget Outlook that projects the nation's fiscal future over the next three decades. CBO's new extended baseline shows a somewhat improved long-term outlook than in its July 2022 Long-Term Budget Outlook, thanks in large part to the $1.5 trillion of ten-year savings in the recently-enacted Fiscal Responsibility Act. However, debt remains on an unsustainable trajectory. Specifically, CBO projects that under current law federal debt held by the public will nearly double, from 97 percent of Gross Domestic Product (GDP) at the end of Fiscal Year (FY) 2022 to 181 percent of GDP by the end of 2053.

At the same time, budget deficits will maintain an upward trajectory. CBO estimates that under current law, the budget deficit will grow from 5.8 percent of GDP ($1.5 trillion) in 2023 to 6.4 percent of GDP ($2.5 trillion) in 2033, 8.1 percent of GDP ($4.6 trillion) in 2043, and 10.0 percent of GDP ($8.0 trillion) in 2053. As a share of the economy, the 2053 deficit will be nearly 3 times larger than the 50-year historical average of 3.6 percent of GDP.

The projected rise in deficits and debt over the next three decades is driven by a disconnect between spending and revenue. CBO expects spending to rise rapidly over the long-term and revenue to grow much more gradually. Specifically, CBO projects spending will rise from 24.2 percent of GDP in FY 2023 to 29.1 percent in 2053, while revenue will increase from 18.4 percent of GDP to 19.1 percent. The projected long-term growth in spending is more than entirely driven by rising retirement, health care, and net interest costs. CBO expects spending on these three areas to grow from 13.4 percent of GDP in 2023 to 21.5 percent in 2053 – a 60 percent increase. Interest payments on the national debt will be the largest federal program by 2051.

CBO also projects that four major trust funds will become insolvent over the next 30 years. Under CBO's estimates, the Highway Trust Fund will exhaust its reserves by 2028, the Social Security Old-Age and Survivors Insurance (OASI) trust fund will run out by FY 2032, the Medicare Hospital Insurance (Part A) trust fund will become insolvent by 2035, and the Social Security Disability Insurance (SSDI) trust fund will be exhausted by 2052. On a theoretically combined basis, assuming revenue is reallocated in the years between OASI and SSDI insolvency, the Social Security trust funds will become insolvent by 2033.

Importantly, CBO's long-term budget projections assume that various tax and spending provisions expire as scheduled under current law, discretionary spending is limited by the Fiscal Responsibility Act and then grows only at the rate of inflation through 2033, and revenue remains elevated in 2023 – despite weak tax collections in April. An Alternative Scenario that assumes extension of expiring provisions, that discretionary spending grows more quickly, and revenue losses persist over the next few years would add nearly 15 percentage points of GDP to the debt by the end of FY 2033 and even more over the long term.

As CBO notes and we've explained before, rising long-term debt poses a series of risks and threats. High debt levels slow income and wage growth, increase interest payments on the national debt and thus crowd out other priorities, place upward pressure on interest rates, limit the fiscal space available to respond to a recession or other emergency, place an undue burden on future generations, and heighten the risk of a fiscal crisis.

The Committee for a Responsible Federal Budget has put out a press release and will publish our full analysis of CBO's June 2023 Long-Term Budget Outlook later today.