Can Medicare Advantage Reforms Save the Trust Fund?

The Medicare Part A Hospital Insurance (HI) trust fund is only six years from insolvency according to the Congressional Budget Office (CBO) and the Medicare Trustees. We estimate costs will exceed dedicated revenue by about $505 billion over the next decade, leaving a $360 billion solvency gap after accounting for current trust fund holdings. Reducing excessive Medicare Advantage (MA) costs, an idea endorsed in the President’s Budget and proposed in our Health Savers Initiative, could help improve its financial state. Every $1 of general Medicare Advantage savings would strengthen the trust fund by roughly 50 cents.1

The Medicare Advantage (MA) program, which allows Medicare beneficiaries to enroll in federally-funded private health insurance plans, is an increasingly popular alternative to traditional fee-for-service (FFS) Medicare. MA plans offer a single insurance package that covers both hospital and physician insurance benefits (Part A and B), and often cover drug (Part D) benefits as well. Many MA plans also cover additional services such as dental, vision, and hearing. About 24 million seniors are currently enrolled in MA plans, which is about two-fifths of all beneficiaries. CBO expects enrollment to rise to half of all beneficiaries by 2030.

While MA plans are popular, they are also costly. Based on CBO estimates, the federal government is projected to spend about $320 billion in 2021 on payments to MA plans, which will nearly triple to $921 billion in 2031. High and rising costs are in part driven by growing enrollment, but they are also because the government tends to spend more on enrollees in MA plans than it does on similar beneficiaries enrolled in traditional fee-for-service (FFS). Per-enrollee costs are also growing more quickly in MA than in FFS. Driving these higher costs are elevated benchmarks in some areas, rebates and quality bonuses for low-cost and/or high-quality plans, higher administrative costs, and higher payments to plans from aggressive coding of patient diagnoses.

Fortunately, there is room to substantially reduce these costs and in turn reduce the HI trust fund shortfall. For example, increasing diagnosis coding intensity adjustments so that payments to plans more accurately reflect actual enrollee risk could save at least $45 billion (under an Obama proposal) and as much as $355 billion (under a more aggressive option we put forward in our Health Savers Initiative). About half of these savings could accrue to Medicare Part A, which means the larger of these options would reduce Part A spending by over $185 billion, closing more than half of the trust fund's solvency gap and a third of its ten-year deficit.

Medicare Advantage Proposals (Ten-Year Budget Impact)

| Policy | Total Savings | Part A Savings | Percent of Solvency Gap | Percent of Deficit |

|---|---|---|---|---|

| Coding Adjustments | ||||

| Adjust MA payments for coding intensity with DECI method (HSI) | $355b | $185b | 54% | 36% |

| Adjust MA payments for coding intensity with MedPAC method (HSI) | $200b | $100b | 30% | 20% |

| Modify risk adjustment methodology (CBO) | $120b | $60b | 18% | 12% |

| Increase coding intensity adjustment to 8% (CBO) | $85b | $45b | 13% | 8% |

| Gradually increase coding intensity adjustment to 8.8% (Obama) | $45b | $20b | 6% | 4% |

| Conduct risk-adjustment validation audits in MA (Obama) | $15b | $10b | 3% | 2% |

| Quality Benchmark Adjustments | ||||

| Eliminate benchmark increases tied to quality-based-payments (CBO) | $165b | $85b | 26% | 17% |

| Eliminate double bonuses from benchmarks (CBO) | $30b | $15b | 5% | 3% |

| Competitive Bidding Reform | ||||

| Set MA Payments based on Competitive Bidding (Brookings)*2 | $230b | $115b | 35% | 23% |

| Reform MA payments with competitive bidding process (Obama) | $55b | $30b | 9% | 6% |

| Other Reforms | ||||

| Align payments to employer group waiver plans with average MA plan bids (Obama) | $15b | $5b | 2% | 1% |

Sources: CBO Estimates; Presidential Budget proposals from 2012, 2015, and 2016; Brookings; and CRFB's HSI MA Estimates.

Estimates cover 2022-2031 and are adjusted by CRFB to match that window.

*Assumes savings as a constant share of Medicare spending over time, and assumes a 5 percent decline in plan bids because of competitive bidding.

Eliminating benchmark increases and double bonuses tied to quality-based-payments (QBPs) in certain areas would also net large savings. Double bonuses may be exacerbating geographic inequities across MA plans, while benchmark increases may not correlate with plan quality. Removing these provisions would collectively save about $200 billion for Medicare overall and just over $100 billion for Part A, improving the ten-year solvency gap by almost a third and reducing the ten-year deficit by 20 percent.

More comprehensive reform, like creating a competitive bidding process that would further incentivize competition on prices and benefit offerings among MA plans, would also yield substantial savings. We estimate an Obama Administration proposal from 2016 would save about $55 billion over a decade, while a proposal put forward by experts at the Brookings Institution could save $230 billion. In other words, competitive bidding could shrink the Part A solvency gap by 9 to 35 percent while reducing the program's deficit by 6 to 23 percent over the decade.

Other reforms, for example MedPAC's proposals to replace QBPs with a reformed Value Incentive Program and further reform MA benchmarks to be better comparable with local FFS spending, could also generate savings for MA and the Medicare trust fund.

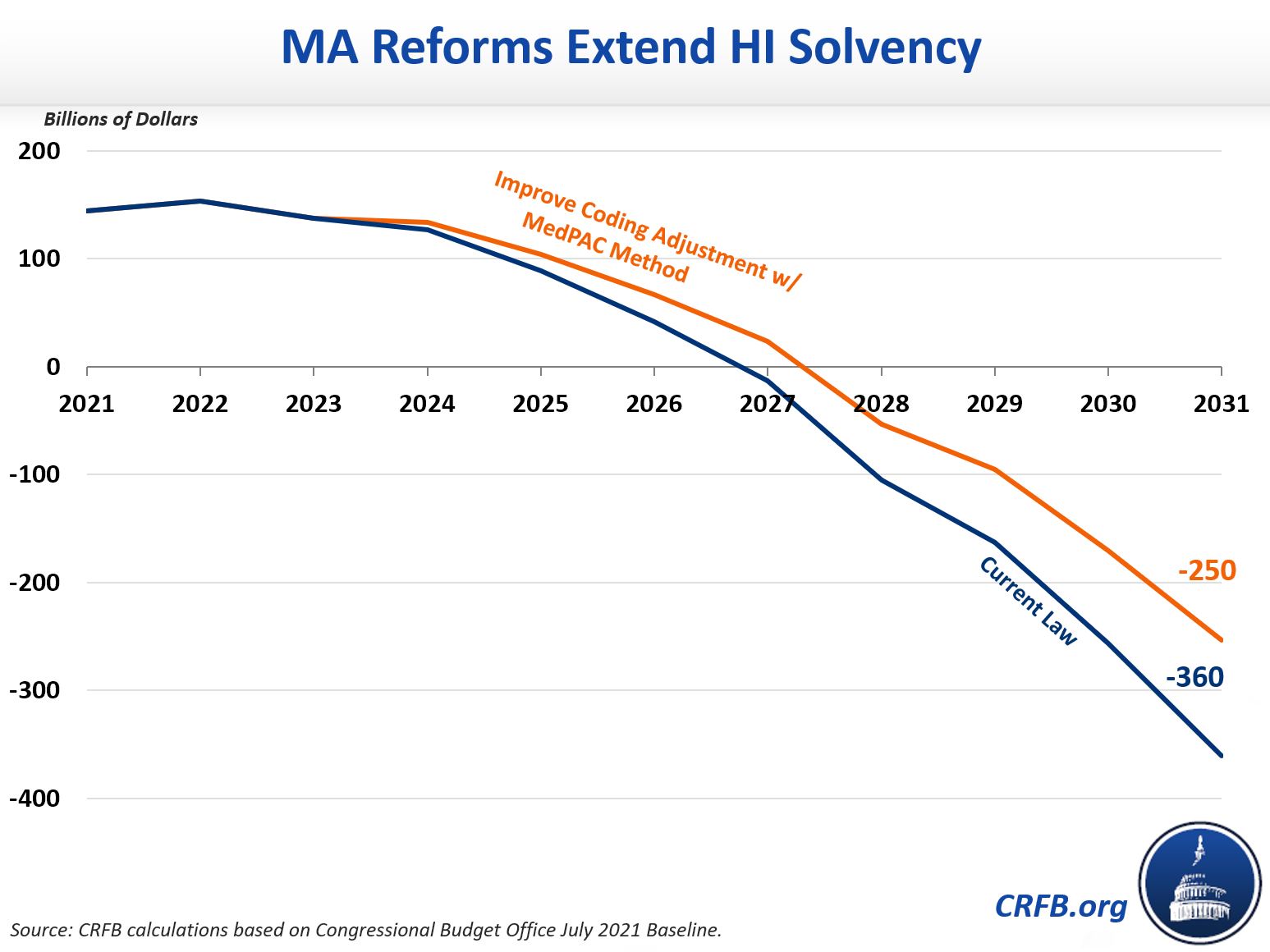

None of these options would ensure long-term HI solvency on their own, but they could delay insolvency and would reduce the remaining hole left to fill. Under current law, based on CBO's latest baseline, we estimate the program would be insolvent by fiscal year 2027, at which point spending would be cut by 18 percent. Funding the program through 2031 would require filling a $360 billion hole.

Adopting our Health Savings Initiative proposal to improve MA coding intensity adjustments using the more modest MedPAC method would extend the HI trust fund's solvency by a year and reduce the automatic cut to 9 percent. It would also shrink the cumulative trust fund deficit in 2031 from $360 billion to $250 billion through 2031. This smaller gap could then be more easily closed with additional revenue and spending adjustments.

Reforms to Medicare Advantage alone are not likely enough to restore solvency, but they can certainly be a significant part of the solution to improve the HI trust fund's financial state.

1 Actual spillover to Medicare Advantage will differ year-to-year. For example, CBO's 8 percent risk adjustment option strengthens the trust fund by 53 cents for every $1 of general annual MA savings from 2022-2024 before falling to 52 cents in 2026.

2 Brookings' option calls for a competitive bidding process where the standard benefit package is set at 105 percent of Medicare FFS's actuarial value.