Analysis of CBO's February 2023 Budget and Economic Outlook

The Congressional Budget Office (CBO) released its latest Budget and Economic Outlook today, projecting the nation’s fiscal and economic future over the next decade. CBO’s new projections update its May 2022 baseline to account for subsequent enacted legislation, executive actions, higher inflation, rising interest rates, slowing economic growth, and other legislative and economic factors. CBO’s new baseline shows:

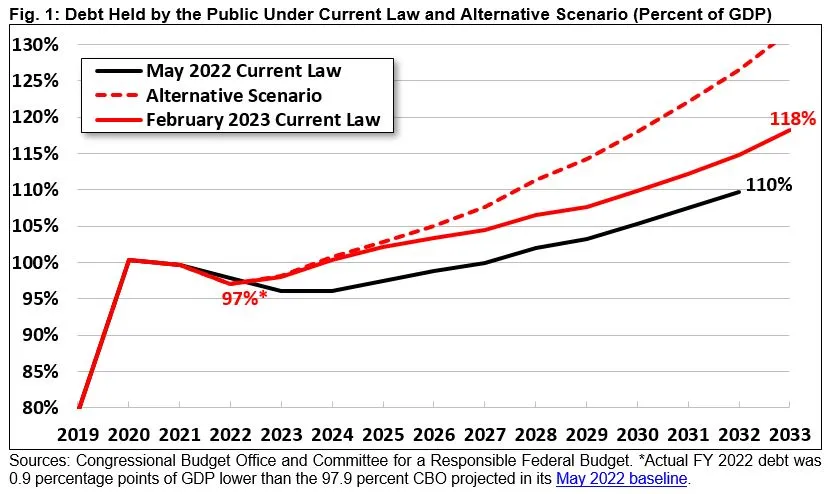

- Debt is on course to reach a record 118 percent of GDP by 2033. CBO projects debt held by the public will grow $22 trillion over the next decade, breaching $46 trillion by the end of Fiscal Year (FY) 2033. Debt will grow from 97 percent of Gross Domestic Product (GDP) in 2022 to 118 percent by 2033; it could grow to over 130 percent of GDP if policymakers extend various expiring policies.

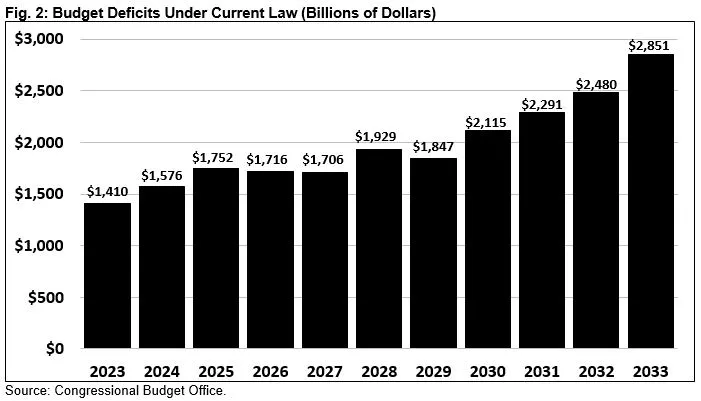

- Deficits will double from $1.4 trillion today to almost $2.9 trillion by 2033. Deficits will total 6.1 percent of GDP ($20.3 trillion) over a decade and reach 7.3 percent of GDP by 2033 – the highest ever outside of a national emergency.

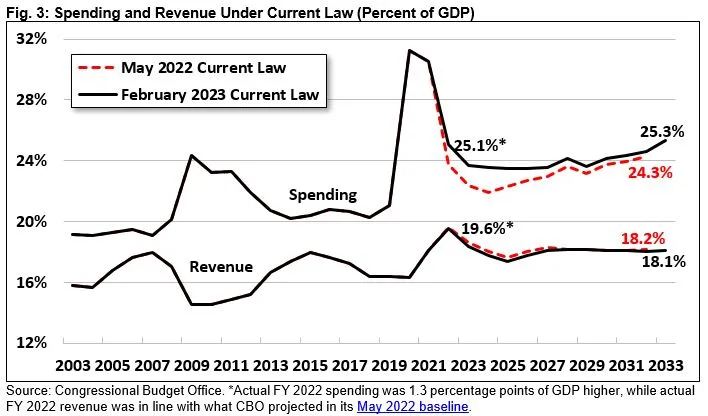

- Spending on health, retirement, and interest will grow rapidly while revenue fails to keep up. Spending will grow from 23.7 percent of GDP in 2023 to 25.3 percent by 2033, while revenue will fall to a low of 17.4 percent of GDP in 2025 before rising to 18.1 percent in 2030 and beyond. Interest costs alone will reach a record 3.6 percent of GDP – $1.4 trillion – by 2033.

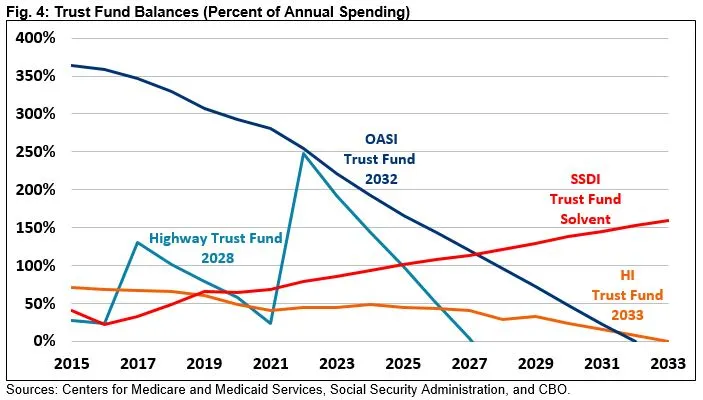

- Three major trust funds will be insolvent this decade, with the Highway Trust Fund running out of money in 2028 and both the Social Security Old-Age and Medicare Hospital Insurance (HI) trust funds running out of reserves in 2033. Upon insolvency, CBO estimates that Social Security benefits will be cut abruptly by about one-quarter.

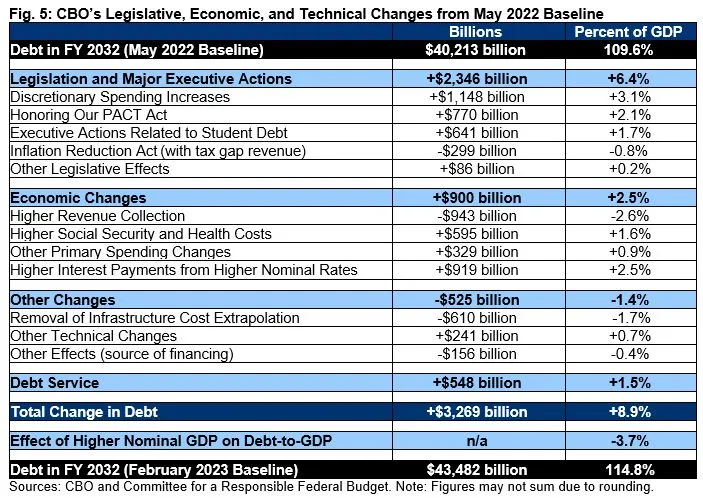

- The fiscal outlook is far worse than last year due to legislation, executive actions, and economic changes. CBO now projects $3.3 trillion more debt in 2032 than it did last May, with roughly $2.3 trillion of the increase due to legislation and executive actions, $900 billion from changes in the economic outlook such as rising interest rates, and $550 billion from higher resulting debt service costs, partially offset by $525 billion of technical and other changes.

- Surging inflation will slowly normalize while interest rates remain high and economic growth weakens. CBO projects Consumer Price Index inflation will be 4.0 percent in 2023 and normalize around 2.2 percent per year beyond that. The economy will stagnate in 2023 as unemployment temporarily rises above 5 percent before falling to 4.5 percent by 2026. Meanwhile, CBO projects the ten-year treasury yield will remain around its current level of 3.8 percent, having risen from less than 1 percent in late 2020 to 2 percent in early 2022.

Debt Will Hit a New Record by 2028, and Continue to Grow Thereafter

CBO projects debt will grow by $22 trillion over the next decade, nearly doubling from about $24 trillion at the end of FY 2022 to above $46 trillion by 2033.

As a share of GDP, debt will grow from 97 percent at the end of FY 2022 – already more than twice the historic average of 47 percent seen over the last half-century – to a record 107 percent of GDP by 2028. It will continue to grow thereafter, topping 118 percent of GDP by the end of 2033. This is substantially higher than predicted in CBO’s May 2022 baseline, which had debt reaching 110 percent of GDP by the end of 2032. Over the longer run, CBO projects debt will reach 195 percent of GDP by 2053.

If policymakers choose to extend policies that are scheduled to expire over the coming years – most significantly, the 2017 tax cuts and the Inflation Reduction Act’s enhanced insurance subsidies, both of which will expire at the end of 2025 – and grow discretionary spending with the economy rather than inflation, debt could be much higher. Our preliminary estimates of such an alternative scenario project debt would exceed 130 percent of GDP by the end of FY 2033.

Rising deficits and debt carry significant risks and threats to the economy and the nation as a whole. Continued fiscal pressures could make it more difficult for the Federal Reserve to wrestle down inflation without causing a recession. High debt levels also stunt economic growth, threaten economic vitality, place a strain on the budget through rising interest payments, create geopolitical challenges and risks, make responding to new emergencies more challenging, and impose intergenerational unfairness between today’s Americans and future generations.

Deficit Will Grow to Nearly $3 Trillion By the End of the Decade

CBO projects deficits will more than double over the next decade, growing from $1.4 trillion in FY 2023 to nearly $2.9 trillion in 2033, and total $20.3 trillion (6.1 percent of GDP) over ten years.

After expiring COVID relief caused deficits to drop from $2.8 trillion to $1.4 trillion between FY 2021 and 2022, CBO projects the deficit in 2023 will remain at $1.4 trillion before rising to nearly $1.6 trillion in 2024. Between 2025 and 2027 – after the 2017 tax cuts expire – deficits will hover around $1.7 trillion before rising to $1.9 trillion in 2028, falling back to $1.8 trillion in 2029, and topping $2 trillion in 2030. By 2033, deficits will approach $2.9 trillion.

As a share of GDP, deficits will steadily rise from 5.4 percent in FY 2023 to 6.1 percent by 2025, fall back to 5.5 percent by 2027, then steadily increase again after 2029. By 2033, deficits will reach 7.3 percent of GDP – more than double the 3.6 percent average over the past 50 years and the highest ever outside of a national emergency.

Importantly, CBO notes that if the Administration’s student debt cancellation plan is ruled illegal by the Supreme Court, the deficit in FY 2023 will be about $379 billion lower than projected.

Under an alternative scenario where expiring tax cuts and spending policies are extended without offsets and discretionary spending grows with the economy instead of inflation, deficits would be much higher. Our preliminary estimates suggest deficits could reach nearly $4 trillion – close to 10 percent of GDP – by FY 2033 under such a scenario.

Spending and Revenue Will Continue to Diverge

Deficits and debt will grow over the next decade as spending growth outpaces flattening revenue. CBO projects spending will total $80 trillion (24.1 percent of GDP) between FY 2024 and 2033, while revenue will total $60 trillion (18.0 percent of GDP), meaning revenue will cover just three-quarters of projected spending.

Total spending will rise from $6.3 trillion in FY 2022 to $9.9 trillion in 2033. As a share of the economy, it will decline from 25.1 percent of GDP in 2022 to 23.5 percent by 2024, before rising to 25.3 percent by 2033. For comparison, the 50-year historical average is 20.9 percent of GDP.

After peaking at 19.6 percent of GDP in FY 2022 – largely due to surging inflation and capital gains realizations – CBO projects revenue will fall to 18.3 percent of GDP in 2023, hit a low of 17.4 percent in 2025, and then rise to 18.1 percent of GDP per year once parts of the 2017 tax cuts expire. Over the past 50 years, revenue has averaged 17.3 percent of GDP.

Rising spending is driven by the growth of health, retirement, and interest costs. CBO projects Social Security and health care spending will nearly double between FY 2022 and 2033, increasing from $1.2 trillion to $2.4 trillion and from $1.4 trillion to $2.7 trillion, respectively. As a share of the economy, each will grow by 1.2 percentage points of GDP.

Meanwhile, interest costs will triple, rising from $475 billion in FY 2022 to $1.4 trillion by 2033 and totaling a record 3.6 percent of GDP in that year.

Major Trust Funds Will be Insolvent This Decade

The Social Security, Medicare, and Highway trust funds will all be insolvent by the end of the decade under CBO’s latest projections. Most imminently, the Highway Trust Fund will run out of reserves in FY 2028, at which point spending will be cut roughly in half absent legislation.

The Medicare Hospital Insurance (HI) trust fund, which funds Part A payments to hospitals, will be exhausted by 2033 under CBO’s projections. At that point, we estimate the program needs to cut spending by more than 10 percent, jeopardizing access to care for 80 million beneficiaries.

And for the first time since the passage of the landmark 1983 reforms, the Social Security trust funds are now projected to be insolvent within a decade – the Old-Age and Survivors Insurance trust fund by 2032 and the theoretically combined old-age and disability trust funds by 2033.

At that point – when today’s 57-year-olds reach the full retirement age and today’s youngest retirees turn 72 – all beneficiaries would face an immediate benefit cut of about one-quarter, regardless of age or income. We previously estimated a typical couple would face a $12,500 to $16,600 cut.

CBO’s baseline assumes these trust funds will continue to spend beyond insolvency and that all three trust funds will run large cash shortfalls over the next decade. Under CBO’s baseline, the Highway Trust Fund will run $375 billion of cash deficits, the Medicare HI trust fund $238 billion of cash deficits, and Social Security trust funds a massive $3.0 trillion of cash deficits.

The Fiscal Outlook Has Worsened Since May 2022

CBO now projects debt in 2032 will be $3.3 trillion higher than projected in May 2022. This is mainly driven by the enactment of fiscally irresponsible legislation and executive actions along with changes in the economy. Importantly, our analysis differs somewhat from CBO’s in that we account for changes in fiscal year 2022 and define technical changes differently.

Legislative changes and major executive actions added $2.3 trillion to deficits on net, mainly from $1.1 trillion of discretionary spending increases, $770 billion from the Honoring Our PACT Act, and $640 billion from debt cancellation and other student debt changes. Partially offsetting these costs are roughly $300 billion in net savings from the Inflation Reduction Act.

Economic changes increased projected deficits by another $900 billion, driven more than entirely by higher current and expected interest rates. All other changes, including technical changes and differences in means of financing, reduced projected debt by $525 billion. These legislative, economic, and technical changes resulted in an increase in debt service costs of $550 billion.

The $3.3 trillion change in debt is equivalent to 8.9 percent of GDP. Because higher inflation increases GDP itself, however, total debt-to-GDP is 5.2 percent higher than in May 2022.

Inflation Will Moderate While Growth Slows and Interest Rates Remain High

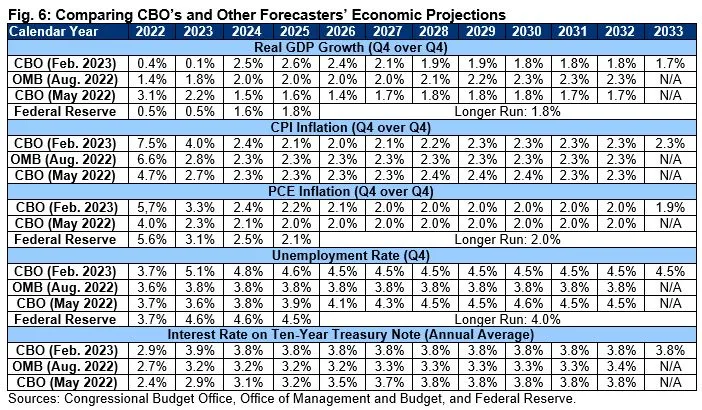

After surging inflation resulted in the Consumer Price Index (CPI) growing 7.1 percent from the fourth quarter of 2021 to 2022, CBO estimates that CPI inflation will grow by 4.0 percent in 2023 and 2.0 to 2.4 percent per year thereafter. Similarly, Personal Consumption Expenditures (PCE) inflation will total 3.3 percent in 2023 and normalize at about 2.0 percent per year by 2025.

CBO expects the inflation slowdown to be accompanied by stagnating growth. After already slow 1.0 percent real GDP growth in 2022, CBO projects growth of only 0.1 percent in 2023, with the unemployment rate rising from 3.4 percent to 5.1 percent by the end of 2023. CBO projects faster growth between 2024 and 2026, with the growth rate stabilizing at about 1.8 percent – and the unemployment rate at 4.5 percent – thereafter.

CBO expects the interest rate on ten-year Treasury notes – which roughly doubled from 2.0 percent to 3.8 percent over the past year – to remain elevated around 3.8 percent through 2033. CBO projects three-month Treasury bills will peak at 4.7 percent in the second quarter of this year before falling gradually to 2.8 percent by the end of 2024 and 2.2 percent by 2026.

CBO’s economic forecast – made in early December 2022 – is more pessimistic than other forecasters. For example, the Federal Reserve estimates that unemployment will hit 4.6 percent and GDP will grow 0.5 percent in 2023, while the Office of Management and Budget estimates a peak unemployment rate of 3.8 percent and growth of 1.8 percent. CBO’s PCE inflation projections of 3.3, 2.4, and 2.2 percent over the next three years, respectively, are closely aligned with the Federal Reserve’s forecast of 3.1, 2.5, and 2.1 percent.

Conclusion

CBO’s latest baseline shows that the fiscal outlook has deteriorated due to new unpaid-for legislative and administrative actions as well as high inflation and interest rates. As a result, deficits are slated to explode and both debt and interest costs are on course to reach new records as shares of the economy. Meanwhile, the Social Security, Medicare, and Highway trust funds will all run out of reserves over the next decade, resulting in automatic across-the-board cuts without changes to prevent them.

Substantial deficit reduction is needed to put the national debt on a sustainable path. A thoughtful fiscal package could help the Federal Reserve tamp down inflation, hold down rising interest rates, restore solvency to our major trust funds, lower health care costs, reduce global and domestic risks, and promote strong and durable economic growth.

Unfortunately, policymakers have focused mostly on worsening the deficit with new spending and tax cuts and promises to take the nation’s largest spending programs off the table for changes. This type of pandering threatens economic prosperity and puts some of the nation’s most important programs at risk.

Lawmakers should put partisan gamesmanship aside and work together on a deficit reduction plan that puts everything on the table. The sooner we act, the better.

Appendix