Lowering the Bar for "Revenue Neutral" Tax Reform

One of the key questions of comprehensive tax reform will be its budgetary target. Congressional leaders have set a revenue-neutral target, raising as much money as the current tax code. However, they may be modifying the baseline in order to redefine “neutral” as more than $400 billion lower.

We estimated the campaign plans put forward by President-elect Trump would reduce revenues by $5.8 trillion over ten years, but Congressional leaders have indicated that tax reform should not lower federal revenues. The House Republican Better Way blueprint “envisions tax reform that is revenue neutral.” Revenue neutrality was also reiterated by Senate Majority Leader Mitch McConnell, House Ways and Means Committee Chairman Kevin Brady, and others.

That goal raises the question of how the baseline is defined: a technical but consequential decision. The Congressional Budget Office current law baseline uses longstanding budget rules, generally assuming laws are unchanged. That baseline shows total revenues are projected to be $42.7 trillion over the next ten years.

That current law revenue projection was reduced significantly by the 2015 tax extenders deal, which cost $680 billion over ten years. But the baseline for determining revenue neutrality may be reduced even further.

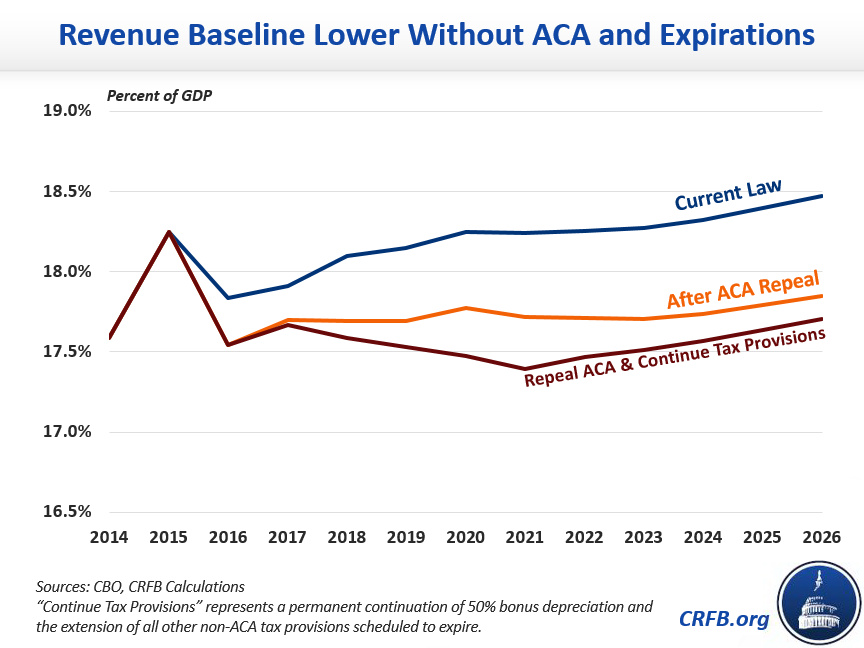

First, tax reform is likely to be considered after action on repealing parts of the Affordable Care Act (ACA). Repealing the ACA, including all the taxes used to finance it, would lower the current law revenue baseline by another $1 trillion, based on the most recent repeal bill scored. This reduction in revenues would not increase the deficit because it would be accompanied by a larger reduction in spending from repeal of ACA coverage provisions (assuming the law's reductions in Medicare spending are retained).

Second, the House Better Way proposal suggests deviating from the normal current law baseline used to score legislation. It would use a “current policy” baseline which assumes expiring tax breaks are permanently extended. In particular, the baseline suggested in the Better Way plan would assume bonus depreciation—which is scheduled to be reduced from 50 percent today to 30 percent by 2019 and then expire—would continue at 50 percent, and other expired and expiring tax provisions would continue indefinitely. Assuming these tax breaks continue instead of expire would lower the revenue baseline by another $419 billion over ten years.

As a share of GDP, revenue would be more than three-quarters of a point lower in 2026 under a baseline that reflected ACA repeal and the continuation of expiring tax provisions.

The use of a current policy baseline is troubling for several reasons. It’s essentially saying tax reform will reduce revenue, but by no more than this future set of tax cuts.

- The costs would disappear from the budget process. As we have previously explained, these expiring provisions were scored as temporary provisions when they were enacted. Congress never accounted for permanent costs of these provisions, and simply assuming they are continued in the baseline would hide those costs from the budget process.

- Congress has indicated these provisions should expire. The tax agreement enacted in 2015 was intended to provide greater certainty in the tax code by permanently extending many of the temporary provisions, but it did not extend all of them. The provisions that expired at the end of 2016 and those still scheduled to expire reflect an affirmative decision that they should not be permanent.

- Congress would raise revenue from letting provisions expire on schedule. Under a current policy baseline, Congress could claim savings from removing a provision that was going to expire anyway or already expired at the end of 2016, improperly using that money to pay for a tax cut elsewhere.

- It will increase the deficit. Tax reform which is scored as revenue neutral under a current policy baseline will increase the deficit relative to current law. Using a current policy baseline, the debt will be almost 2 percent of GDP higher in 2026, reaching 87.3 percent instead of 85.5 percent.

The Budget Act gives Congress flexibility to choose which baseline will be used to enforce the budget resolution, an important question when trying to use reconciliation to pass tax reform without a 60-vote margin in the Senate.

Changing the baseline would allow a reconciliation bill for tax reform to reduce revenues by more than $400 billion below current law – and increase the deficit by approximately $480 billion above current law with interest – but still comply with reconciliation instructions requiring the bill to nominally reduce the deficit.

However, there are many different enforcement mechanisms. While such a revenue-losing reconciliation bill would be considered neutral for enforcement of the budget resolution, it would still be negative under the Senate PAYGO rule and the Statutory Pay-As-You-Go Act, which are enforced using a current law baseline.

The choice of baseline would also affect a bill’s dynamic estimate. If the Joint Committee on Taxation estimated legislation against a current policy baseline, the dynamic effects would likely be smaller for a plan like the House Better Way that moved to full expensing, where businesses can immediately their capital purchases, instead of depreciating them over time.

A current policy baseline would assume continuation of bonus depreciation, so many investments could already be 50 percent expensed. Full expensing would provide a smaller marginal benefit than it would relative to current law where bonus depreciation expires.

The revenue-neutral standard for tax reform is a useful fiscal goal which imposes some budget discipline. However, crucial details remain about how revenue neutrality is measured. We hope that Congress chooses to follow the long-established budget scoring rules to enforce revenue neutrality against current law. They should not use current policy to lower the bar, claim deficit neutrality, and obscure an increase in the deficit.