COVID Money Tracker: Policies Enacted Through August 14

This is an archived version of this table last updated on August 14, 2020. For the latest on COVID-related spending, head to our new interactive site at www.COVIDMoneyTracker.org.

See the up-to-date interactive version of this table.

The novel coronavirus (COVID) pandemic and resulting economic crisis has been met with an unprecedented policy response. Through legislative, administrative, and Federal Reserve actions, policymakers are currently working to pour trillions of dollars into the economy. COVID Money Tracker is a new initiative of the Committee for a Responsible Federal Budget focused on identifying these dollars and tracking their disbursement. The project will ultimately feature a state-of-the-art interactive database similar to Stimulus.org, where we tracked stimulus, financial rescue, and extraordinary Federal Reserve measures enacted in response to the 2008 financial crisis.

COVID Money Tracker will ultimately track every major action taken by Congress, the Federal Reserve, the executive branch, and various federal agencies, following how much is disbursed over time, where the funds go, and how much is recovered through loan repayments, dividends, or equity repurchases.

In this analysis, we show the actions taken so far and the status of those actions where possible. So far, enacted legislation has authorized roughly $3.7 trillion of fiscal support, which will ultimately add around $2.5 trillion to the deficit. Around $2.2 trillion of those funds have already been disbursed or committed. Meanwhile, administrative actions from the President are likely to cost another $62 billion. In addition, the Federal Reserve has already undertaken $2.2 trillion in emergency lending, asset purchases, and other activities and has announced plans that could provide $7 trillion in support to the economy.

Summary Table of Responses to COVID

| Response | Allowed | Disbursed/ Committed |

Deficit Impact |

|---|---|---|---|

| Legislative Actions | $3.7 trillion | $2.2 trillion | $2.5 trillion |

| Coronavirus Preparedness & Response Supplemental Appropriations Act | $8 billion | ~$3 billion | $8 billion |

| Families First Coronavirus Response Act | $192 billion | ~$90 billion | $192 billion |

| CARES Act | $2.7 trillion | $1.7 trillion | $1.8 trillion |

| Paycheck Protection Program and Health Care Enhancement Act | $799 billion | $410 billion | $483 billion |

| Student Veteran Coronavirus Response Act of 2020 | Unknown | Unknown | Unknown |

| Paycheck Protection Program Flexibility Act | *0 | *0 | *0 |

| Paycheck Protection Program extension | $0 | $2 billion | $0 |

| Emergency Aid for Returning Americans Affected by Coronavirus Act | $9 million | Unknown | $9 million |

| Administrative Actions | ~$584 billion | ~$413 billion | ~$62 billion |

| Declare national emergency | N/A | N/A | N/A |

| Defer income and payroll tax payments | ~$400 billion | ~$300 billion | ~$5 billion |

| Offer advanced payments to Medicare providers | ~$100 billion | $100 billion | $0 |

| Fund ¾ of $400 unemployment supplement with disaster funds | $44 billion | $0 billion | $44 billion |

| Defer student loan payments and waive interest | ~$30 billion | $10 billion | ~$10 billion |

| Other executive actions | ~$10 billion | $3 billion | ~$3 billion |

| Federal Reserve Actions | >$7.0 trillion | $2.2 trillion | N/A |

| Interest rate changes | N/A | N/A | N/A |

| Asset purchases | >$2.1 trillion1 | $2.0 trillion | N/A |

| Liquidity measures | >$1.9 trillion | $106 billion | N/A |

| Emergency lending programs and facilities | >$2.7 trillion | $97 billion | N/A |

Deficit impact is from 2020-2030.

The tables below offer more detail on the actions taken to date. We will continue to track these actions and follow the money as it is disbursed at www.COVIDMoneyTracker.org.

Legislative Actions

In March 2020, Congress enacted three pieces of legislation related to the current pandemic and economic crisis. In total, these bills will allow roughly $2.9 trillion of spending, tax cuts and tax deferrals, loans, and other measures. In April, a fourth bill, the Paycheck Protection Program and Health Care Enhancement Act was enacted which provides around $733 billion in fiscal support. Four smaller bills have also been passed, mostly with small fiscal impacts. Based on scores from the Congressional Budget Office (CBO), these eight bills will add about $2.5 trillion to the deficit, on net, over the next decade. So far, we have identified around $2 trillion that has been disbursed or committed, though only some of that has been actually disbursed so far, and this number does not capture programs that have no publicly available data or announcements about disbursements.

The first bill, the Coronavirus Preparedness and Response Supplemental Appropriations Act, authorized $8.3 billion in emergency funding to help mitigate the coronavirus outbreak. The emergency appropriations in this bill were directed toward the immediate health response to the virus, including increased funding for vaccine development, health preparedness, Community Health Centers, and overseas efforts to combat the outbreak.

The second bill, the Families First Coronavirus Response Act established a new tax credit for COVID-related sick leave; increased federal support for existing automatic stabilizers; waived Medicare, Medicaid, and Children's Health Insurance Program (CHIP) cost-sharing for COVID-related treatment; and approved more funding for agencies to spend on COVID-related needs. CBO estimates the bill will increase deficits by $192 billion over ten years.

The third bill, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, included one-time direct payments to households, an expansion of unemployment benefits, forgivable loans to small businesses, support for new Federal Reserve lending facilities, additional federally-backed loans and grants to businesses, expansions of safety net programs, tax breaks and increased federal support for individuals and businesses, funding for health providers, grants to states, and a variety of other changes. The CARES Act authorized roughly $2.7 trillion of fiscal support, which CBO estimates will ultimately add $1.8 trillion to the deficit.

The fourth bill, the Paycheck Protection Program and Health Care Enhancement Act mostly builds on programs established in the CARES Act, appropriating $321 billion more for the small business Paycheck Protection Program (PPP), increasing funding for Emergency Injury Disaster loans and grants by $60 billion, and adding $100 billion to the Public Health and Social Services Emergency Fund. The bill provides roughly $800 billion in fiscal support, which per CBO estimates will add $483 billion to the deficit.

The fifth bill, the Student Veteran Coronavirus Response Act of 2020, extends some veterans’ and GI bill benefits during emergencies. CBO has not estimated the cost of this bill, but it would be small compared to the major legislation.

The sixth bill, the Paycheck Protection Program Flexibility Act, was signed into law on June 5. It also reforms the Paycheck Protection Program (PPP) established under the CARES Act in order to provide greater flexibility to PPP loan recipients. This bill has not yet been estimated by CBO. The bill likely increases the usage of the PPP program somewhat but because CBO already assumed the PPP program would be fully subscribed, it is not clear if costs would increase beyond the CBO estimates.

A seventh bill extending the Paycheck Protection Program was signed into law on July 4. The bill extends the PPP application period through August 8 and does not authorize any additional PPP funding. As of the original June 30 deadline, $132 billion in funding remains available.

The eighth bill, the Emergency Aid for Returning Americans Affected by Coronavirus Act, was signed into law on July 13. The bill increases the amount of money available for the Department of Health and Human Services to provide assistance to repatriated U.S. citizens, from $1 million to $10 million for Fiscal Year 2020.

More details on these bills is available in the appendix of this piece and in our summaries of the CPRSA, FFCRA, CARES Act, the Paycheck Protection Program and Health Care Enhancement Act, and the Paycheck Protection Program Flexibility Act.

Legislative Responses

| Policy | Allowed | Disbursed/ Committed | Deficit Impact |

|---|---|---|---|

| Fund R&D for vaccines, testing, and other treatments | $3 billion | <$1 billion | $3 billion |

| Increase funding for Centers for Disease Control | $2 billion | $1 billion | $2 billion |

| Increase funding for preparedness and supplies, and for Community Health Centers | $1 billion | <$1 billion | $1 billion |

| Fund the State Department health response overseas | $1 billion | $1 billion | $1 billion |

| Waive restrictions for Medicare telehealth and other spending | $1 billion | <$1 billion | $1 billion |

| Coronavirus Preparedness & Response Supplemental Appropriations Act (March 4, 2020) | $8 billion | ~$3 billion | $8 billion |

| Mandate and subsidize emergency paid leave | $105 billion | ~$66 billion | $105 billion |

| Increase Medicaid matching funds to states | $50 billion | ~$14 billion | $50 billion |

| Allow states to increase SNAP benefits, waive work requirements | $21 billion | $9 billion | $21 billion |

| Require and partially fund free COVID-19 testing | $10 billion | <$1 billion | $10 billion |

| Fund extended unemployment benefits past 26 weeks | $5 billion | <$1 billion | $5 billion |

| Increase funding for nutrition programs | $1 billion | <$1 billion | $1 billion |

| Families First Coronavirus Response Act (March 18, 2020) | $192 billion | ~$90 billion | $192 billion |

| Increase UI benefits by $600/week | ~$200 billion2 | ~$200 billion | ~$200 billion2 |

| Pandemic Emergency Unemployment Compensation | $51 billion | $5 billion | $51 billion |

| Pandemic Unemployment Assistance | $60 billion3 | ~$33 billion3 | $60 billion3 |

| Additional unemployment provisions and UI revenue effects | $6 billion | <$1 billion | $6 billion |

| Provide tax rebates of $1,200/adult and $500/child | $293 billion | $272 billion | $293 billion |

| Support $4.5 trillion of Federal Reserve loans | $454 billion | $195 billion4 | $0 billion |

| Provide forgivable small business loans (Paycheck Protection Program) | $349 billion | $328 billion5 | $349 billion |

| Subsidize loan payments for existing SBA loans for 6 months | $17 billion | ~$13 billion | $17 billion |

| Provide aid to states for pandemic-related costs | $150 billion | $149 billion | $150 billion |

| Provide payments to hospitals (Provider Relief Fund) | $100 billion | $100 billion | $100 billion |

| Loosen TCJA-imposed caps on interest deductibility & operating losses | $239 billion6 | ~$5 billion | $174 billion |

| Offer payroll tax credits for some businesses who retain workers at a loss | $55 billion | ~$38 billion | $55 billion |

| Delay employer payroll tax payments for some businesses | $352 billion6 | ~$158 billion | $12 billion |

| Provide loans to airlines and firms vital to national security | $46 billion | $18 billion7 | $1 billion |

| Expand FEMA Disaster Assistance Fund | $45 billion | $10 billion | $44 billion |

| Increase preparedness and health agency funding | $37 billion | $18 billion | $37 billion |

| Provide grants to airlines to avoid furloughs & pay cuts | $32 billion | $27 billion | $24 billion |

| Establish Education Stabilization Fund for states | $31 billion | $30 billion | $31 billion |

| Defer student loan payments for 6 months and preserve student aid | $30 billion | $23 billion | $9 billion |

| Increase Medicare payments and repeal sequester, expand telehealth & home services, fund community health centers | $28 billion | $5 billion | -$1 billion |

| Issue infrastructure grants to transit providers, including state & local governments | $25 billion | $25 billion | $25 billion |

| Increase SNAP & child nutrition funding | $25 billion | Unknown | $25 billion |

| Increase funding toward veterans & defense health | $20 billion | <$1 billion | $19 billion |

| Boost housing support | $12 billion | $8 billion | $12 billion |

| Provide emergency grants (EIDL) for small businesses | $10 billion | $10 billion | $10 billion |

| Provide grants to publicly-owned commercial airports | $10 billion | $10 billion | $10 billion |

| Provide loan to postal service | $10 billion | $10 billion | $10 billion |

| Allow use of health savings accounts for over-the-counter medication and menstrual products | $9 billion | Unknown | $9 billion |

| Allow emergency retirement account withdrawals | $8 billion | Unknown | $8 billion |

| Increase child & family services funding | $5 billion | $4 billion | $5 billion |

| Suspend aviation taxes | $4 billion | Unknown | $4 billion |

| Let nonitemizers deduct up to $300 of charitable donations and loosen caps on charitable deduction | $3 billion | $0 | $3 billion |

| Help states prepare and respond to COVID-19 for the 2020 election | $0.4 billion | $0.4 billion | $0.4 billion |

| Other policies | $19 billion | $13 billion | $19 billion |

| CARES Act (March 27, 2020) | $2.7 trillion | $1.7 trillion | $1.8 trillion |

| Increase funding for forgivable small business loans (Paycheck Protection Program) | $321 billion | $204 billion5 | $321 billion |

| Expand health provider emergency grant fund program for COVID-19 preparedness and expenses | $75 billion | $16 billion | $75 billion |

| Provide emergency grant fund program for COVID-19 testing | $25 billion | $16 billion | $25 billion |

| Increase small business emergency loan (EIDL) authorization | $366 billion8 | $164 billion | $50 billion |

| Increase funding for small business emergency grants (EIDL) | $10 billion | $10 billion | $10 billion |

| Increase funding for Small Business Administration | $2 billion | Unknown | $2 billion |

| Paycheck Protection Program and Health Care Enhancement Act (April 24, 2020) | $799 billion | $410 billion | $483 billion |

| Extend PPP applications through August 8 | $0 | $2 billion | $0 |

| Paycheck Protection Program extension bill (July 4, 2020) | $0 | $2 billion | $0 |

| Temporary assistance for repatriated Americans | $9 million | Unknown | $9 million |

| Emergency Aid for Returning Americans Affected by Coronavirus Act (July 13, 2020) | $9 million | Unknown | $9 million |

| Total, Legislation | $3.7 trillion | $2.2 trillion | $2.5 trillion |

Source: Congressional Budget Office, Joint Committee on Taxation, legislative summaries, agency reports, Federal Reserve, media reports, CRFB estimates. Deficit impact is from 2020-2030.

Administrative Actions

In addition to Congress, the Trump Administration has taken actions aimed at ameliorating the economic and health effects of the COVID pandemic. These actions include freeing up disaster relief funds, delaying tax filing, expanding advanced payments to health providers, instituting moratoriums on student loan interest payments and Federal Housing Administration (FHA) borrower evictions and foreclosures, allowing high-deductible plans to cover coronavirus costs, and emergency food purchases. We estimate these policies will provide nearly $600 billion of near-term support and liquidity into the economy and ultimately cost about $60 billion.

| Action | Allowed | Disbursed/Committed | Deficit Impact |

|---|---|---|---|

| Declare national emergency (March 13, 2020) | N/A9 | N/A9 | N/A9 |

| Allow high-deductible plans to pay for COVID-19 testing and treatment (March 11, 2020) | Unknown | N/A | Unknown |

| Delay tax deadlines to July 15 (March 17, 2020) | $300 billion | ~$300 billion10 | $0 billion |

| Defense Production Act invocation (March 18, 2020) | N/A | $3 billion | $0 billion |

| Institute 120-day moratorium on evictions and foreclosures for FHA-backed mortgages (March 18, 2020) | $0 billion | $0 billion | $0 billion |

| Institute temporary moratorium on federal student loan interest (March 20, 2020) | ~$10 billion | ~$10 billion | ~$5 billion |

| Disaster area declaration funds for Economic Injury Disaster Loans (March 21, 2020) | $8 billion | Unknown | $1 billion |

| Expansion of advanced payments to health providers (March 28, 2020) | $100 billion | $100 billion | $0 |

| Emergency USDA food purchases (April 17, 2020) | <$1 billion | $0 | <$1 billion |

| Institute 60-day suspension on certain immigrants entering the country (April 22, 2020) | Unknown | N/A | Unknown |

| Relax residency requirements to allow U.S. nationals living abroad to qualify for foreign earned income exclusion (May 11, 2020) | Unknown | $0 | Unknown |

| Allow employees to make mid-year changes to flexible spending accounts and spend them through the end of 2020 (May 12, 2020) | <$1 billion | $0 | <$1 billion |

| Pay interest on late tax refunds (June 24, 2020) | <$1 billion | $0 | <$1 billion |

| Reimburse health providers for self-isolation counseling (July 30, 2020) | Unknown | $0 | Unknown |

| Expansion and extension of Provider Relief Fund deadlines (July 31, 2020) | N/A | N/A | N/A |

| Expansion of telehealth services and changing payments to rural providers (August 3, 2020) | N/A | N/A | N/A |

| Fund ¾ of $400 unemployment supplement with disaster funds (August 8, 2020)11 | $44 billion | $0 | $44 billion |

| Defer certain employee-side Social Security payroll tax collection until December 31 (August 8, 2020) | ~$100 billion | $0 | ~$5 billion |

| Extend deferral of student loan payments and cancel interest payments from Sept 30 through Dec 31 (August 8, 2020) | $20 billion | $0 | $5 billion |

| Review of homeowner and renter assistance (August 8, 2020) | N/A | N/A | N/A |

| Total, Administrative Actions | ~$584 billion | ~$413 billion | ~$62 billion |

Source: Trump Administration. Deficit impact is from 2020-2030

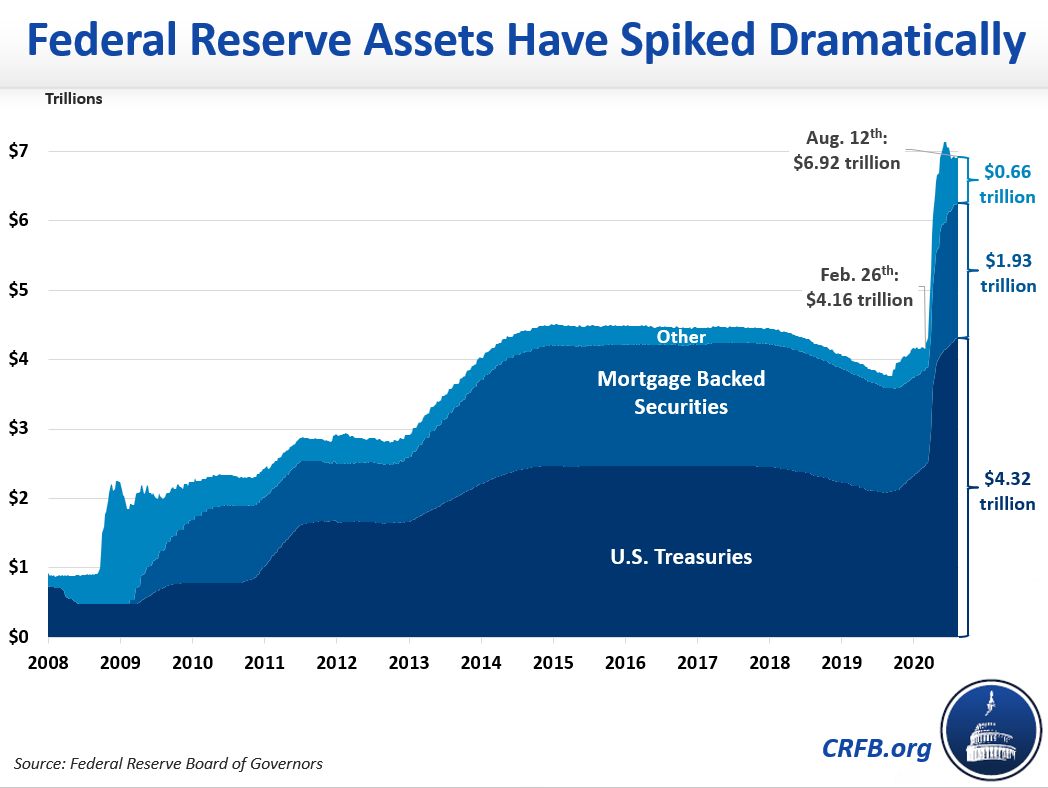

Federal Reserve Actions

The Federal Reserve has taken a number of actions since the pandemic began to promote economic and financial stability, inject liquidity into the economy, and extend available credit. Specifically, the Federal Reserve has reduced interest rates, expanded asset purchases, engaged in liquidity measures, and offered emergency lending. On net, we estimate these measures total $2.2 trillion in economic support so far, including $2 trillion from expanding its holdings of Treasuries and mortgage-backed securities. The total measures the Federal Reserve has announced it will allow itself to undertake could total as much as $7 trillion. Federal Reserve actions have no direct impact of the federal budget deficit.

Among the measures the Federal Reserve has or will undertake includes the purchase of Treasuries and mortgage-backed securities; expanded repo and dollar swap operations; the revival of emergency lending facilities from the Great Recession for money market mutual funds, commercial paper, primary dealer financial institutions, and asset-backed securities; and new lending facilities creates with support of the CARES Act to support corporate credit, small business loans, and municipal bonds. The Federal Reserve has also agreed to buy forgivable bank loans offered to small businesses under the Paycheck Projection Program.

| Action | Announced | Allowed | Disbursed |

|---|---|---|---|

| Cut federal funds rate by 0.5% to 1-1.25% | March 3 | N/A | N/A |

| Cut federal funds rate by 1% to near-zero | March 15 | N/A | N/A |

| Reduce reserve requirements to zero | March 26 | N/A | N/A |

| Subtotal, Interest Rate and Reserve Requirement Changes | N/A | N/A | |

| Increase long-term Treasury security holdings | March 12-23 | $1.49 trillion12 | $1.44 trillion13 |

| Increase mortgage-backed security holdings | March 12-23 | $624 billion12 | $562 billion13 |

| Subtotal, Asset Purchases | $2.12 trillion13 | $2.00 trillion14 | |

| Increase overnight repo operations | March 9-16 | $500 billion | $0 billion14 |

| Increase one-month term repo operations | March 11-16 | $500 billion | |

| Increase three-month term repo operations | March 12-16 | $500 billion15 | |

| Increase central bank dollar swap line arrangements | March 15 | $447 billion | $106 billion |

| Establish FIMA Repo Facility | March 31 | $193 billion | $0 billion |

| Subtotal, Liquidity Measures | $1.95 trillion | $106 billion | |

| Re-institute Commercial Paper Funding Facility | March 17 | $13 billion | <$1 billion |

| Re-institute Primary Dealer Credit Facility | March 17 | $33 billion | $1 billion |

| Re-institute Money Market Mutual Fund Liquidity Facility | March 18 | $53 billion | $12 billion |

| Re-institute Term Asset-Backed Securities Loan Facility | March 23 | $100 billion | $2 billion |

| Establish Primary and Secondary Market Corporate Credit Facilities16 | March 23 | $750 billion | $12 billion |

| Establish Paycheck Protection Program Loan Facility | April 6 | $659 billion | $68 billion |

| Establish Main Street Business Lending Program16 | April 9 | $600 billion | <$1 billion |

| Establish Municipal Liquidity Facility16 | April 9 | $500 billion | $1 billion |

| Subtotal, Emergency Lending | $2.71 trillion | $97 billion | |

| Total | $7.0 trillion | $2.2 trillion | |

| Memo: Total Federal Reserve Balance Sheet | $6.9 trillion | ||

| Memo: Increase in Balance Sheet Since February 26 | $2.8 trillion |

Source: Federal Reserve, Federal Reserve Bank of New York

Note: Subtotals and total for amount allowed include current disbursed amount for programs without size limits.

In total, the Federal Reserve balance sheet has expanded by $2.8 trillion since February 26 — from $4.2 trillion to $6.9 trillion — and the balance sheet may expand more over the course of the crisis.

*****

Together, these measures will provide a substantial amount of financial support for the economy. The COVID Money Tracker will track these programs dollars are disbursed and in some cases repaid, while also monitoring further executive, legislative, and Federal Reserve action. Visit www.COVIDMoneyTracker.org regularly for more information.

Appendix - Details on Actions Taken

Below are more detailed summaries of each of the actions taken by Congress, the White House, and the Federal Reserve.

Congressional Legislation

Coronavirus Preparedness and Response Supplemental Appropriations Act (H.R. 6074)

The first legislative COVID response was an emergency appropriations bill that was signed into law in early March. The bill includes about $3.1 billion for research and development for COVID vaccines and other treatments, about $3.2 billion for health care preparedness and supplies to the Centers for Disease Control and Prevention (CDC) and other health care entities, $1.2 billion to the State Department to support embassies and provide humanitarian aid and other assistance to other countries, and small amounts of funding for the Food and Drug Administration (FDA) and the Small Business Administration. The bill also waives certain restrictions on telehealth in the Medicare program in emergency areas (now the whole country), allowing more Medicare enrollees to have doctor's visits done remotely.

CBO estimates the bill will cost $8.1 billion over ten years, with $7.6 billion coming from emergency appropriations and $490 million coming from the telehealth changes.

The House and Senate passed the bill nearly unanimously on March 4 and March 5, respectively, and President Trump signed it into law on March 6.

Families First Coronavirus Response Act (H.R. 6201)

The second legislative response contained broader public health and economic measures in a bill negotiated by House Democrats and the Trump administration. Most notably, the bill requires public and private employers with fewer than 500 employees to provide emergency sick leave to employees during a public health emergency. Specifically, it requires those businesses for the rest of 2020 to offer employees who have to stay home with a child ten days of unpaid sick leave, then paid leave at two-thirds of an employee's pay for another ten weeks, limited to $200 per day and $10,000 total. It also requires two weeks of paid sick leave for anyone specifically affected by COVID at two-thirds pay. Businesses will be reimbursed for the cost of sick leave through payroll tax credits.

Other policies include increasing the Medicaid matching rate to states and Medicaid funding for territories; requiring all insurance to cover COVID testing without cost-sharing and appropriating $1 billion to reimburse tests for the uninsured; expanding Supplemental Nutrition Assistance Program (SNAP) benefits by waiving work requirements and allowing states to increase benefits to the maximum allotment; fully federally funding a second 26-week period of unemployment benefits that is usually half state-funded; and increasing funding for the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC), senior meal delivery, and food banks.

CBO estimates the bill will cost $192 billion over ten years. The majority of the cost ($105 billion) is for the paid leave provisions, with other costs coming from the Medicaid funding ($50 billion), SNAP expansion ($21 billion), free testing requirement ($10 billion), unemployment benefit funding ($5 billion), and nutrition program funding ($1 billion).

The House passed the bill by an overwhelming majority on March 14, and the Senate did the same on March 18. President Trump signed it into law on March 18.

Coronavirus Aid, Relief, and Economic Security (CARES) Act (H.R. 748)

The third legislative response largely focuses on economic relief for households and businesses but also additional funding for health measures. The bill includes $269 billion for an expansion of unemployment benefits to increase the benefit size, the number of weeks it is available for, and the people who qualify beyond just employees. It also provides rebates of $1,200 per adult and $500 per child to people making less than $75,000 and couples making less than $150,000, costing $293 billion. State and local governments will get $150 billion of general funding (at least $1.25 billion per state) and another $30 billion for to cover education spending, while college students are able to receive student aid that was interrupted by the pandemic and get a six-month moratorium on student loan payments, costing $9 billion. In addition, the bill increases safety net spending on nutrition, family services, and housing by $42 billion and includes several small tax cuts for individuals totaling $10 billion.

For businesses, there is $377 billion of funding for small businesses, with almost that entire amount going to Paycheck Protection Program loans that will be forgiven to the extent they went toward basic expenses; emergency grants to businesses take up the small remainder. In addition, the bill authorizes $510 billion of loans for big businesses and governments, with $55 billion set aside for airlines, firms vital to national security, and the postal service, and $454 billion to support Federal Reserve lending facilities to provide $4.5 trillion of credit to other businesses and state and local governments. The bill also includes $280 billion of tax cuts, mostly for temporarily loosening caps on net operating loss and interest deductions but also by providing a payroll tax credit to businesses who maintain payroll and by delaying payment of 2020 employer payroll taxes until the following two years.

The bill contains $180 billion of health-related spending, including $100 billion of hospital funding, about $35 billion of preparedness and response funding across several agencies, $20 billion of funding for veterans and defense health programs, about $20 billion to expand Medicare provider payments and benefits and expand telehealth and home health services, and about $5 billion to fund community health centers. In addition, the bill appropriates $45 billion for the disaster relief fund that the March 13 emergency declaration opened up.

CBO estimates the bill will cost around $1.7 trillion through 2030. The main difference between CBO's score and the numbers above is that the $510 billion of loans for businesses and municipal governments will have very little actual cost. CBO estimates there will be zero net costs from the Fed lending facilities and only a $1 billion net cost from lending to airlines and businesses vital to national security. Combined with the $10 billion of additional borrowing authority for the postal service, this section of the bill will have a net cost of $11 billion.

The Senate unanimously approved the bill on March 25, and the House passed it by voice vote on March 27. President Trump signed it into law on March 27.

Paycheck Protection Program and Health Care Enhancement Act (H.R. 266)

The fourth legislative response, dubbed "phase 3.5" increases funding for the Paycheck Protection Program (PPP) established under the CARES Act; the program exhausted its initial appropriation of $349 billion last week. The bill substantially increases funding for the program from $349 billion to $670 billion — a $321 billion increase ($310 million available in loans). Of the $310 billion available in loans, $60 billion are to be made by small banks, community financial institutions, and credit unions with under $50 billion in consolidated assets.

The bill appropriates an additional $50 billion for the Economic Injury Disaster Loan (EIDL) program, which is estimated to support around $300 billion in loans. The bill also boosts funding for the EIDL grant program by $10 billion, which offers a $10,000 cash advance to help struggling business owners affected by the nationwide economic lockdowns. The Small Business Administration (SBA) will also receive $2.1 billion in additional funding to support their operational capacity.

The bill also provides an additional $75 billion in funding for health providers to prepare and respond to the COVID-19 outbreak, and $25 billion for Coronavirus testing. Of the $25 billon allocated for testing, $11 billion is earmarked for states, localities, territories, and tribal communities.

While the bill provides around $733 billion in fiscal support into the economy through the increased lending capacity of the EIDL program, CBO estimates the bill will cost $483 billion over ten years.

The Senate passed the bill by unanimous consent on April 21, and the House passed it 388-5 on April 23. President Trump signed it into law on April 24.

The Student Veteran Coronavirus Response Act of 2020 (H.R. 6322)

The fifth bill extends several student veteran programs, allowing work-study and other payments to continue during an emergency. If a student’s school closed due to the emergency situation, the time period and amount available under the GI bill is extended. The House and Senate passed the bill by unanimous consent on March 31 and April 21, respectively. President trump signed it into law on April 28. It has not been estimated by CBO.

Paycheck Protection Program Flexibility Act (H.R. 7010)

The sixth bill provides some more flexibility for Paycheck Protection Program loan recipients, relaxing some of the restrictions on PPP loans so they can be used for a broader set of purposes and still be forgiven. Specifically, the bill increases the portion of loans that can be used for non-payroll-related expenses, extends the window within which all funds must be spent in order to be forgiven, extends the deadline for rehiring and creates exemptions for businesses that can't rehire, extends the loan repayment period, changes the rules regarding deferral of repayment for non-forgiven loan portions, and makes recipients eligible to defer their 2020 payroll taxes to 2021 and 2022.

Neither the Congressional Budget Office nor the Joint Committee on Taxation has scored the bill to date, but we estimate a minor deficit impact. As a result of this legislation, more PPP loans will be forgiven and payroll taxes delayed. However, previous CBO estimates already assumed the PPP program would be fully subscribed so we assume most this legislation’s additional cost has already been incorporated in previous estimates.

The Senate passed the bill by unanimous consent on June 3, and the House passed the bill 417-1 on May 28. President Trump signed it into law on June 5.

Paycheck Protection Program extension bill (S. 4116)

The seventh bill extends the PPP application period from the original June 30 deadline through August 8 and does not authorize any additional funding. The bill will therefore not have any net deficit effect. The bill passed both chambers by unanimous consent and was signed into law by the President on July 4, 2020.

Emergency Aid for Returning Americans Affected by Coronavirus Act (S. 4091)

The eighth bill increases the amount of money available for the Department of Health and Human Services (HHS) to provide assistance to repatriated U.S. citizens, from $1 million to $10 million for Fiscal Year 2020.

HHS can provide temporary assistance to Americans without resources who are returning from overseas as a result of crisis. Funding for the program is capped at $1 million per year and typically provides assistance to fewer than 1,000 Americans per year. Since the beginning of the coronavirus outbreak, the State Department has helped repatriate around 100,000 Americans, so Congress deemed it necessary to increase funding for the HHS repatriation program to provide assistance to the large increase in eligible applicants.

The House and Senate both passed the bill by unanimous consent on June 29 and it was signed into law on July 13.

Administrative Actions

Declare a National Emergency

President Trump declared a national emergency on March 13. This declaration allows the Department of Health and Human Services (HHS) to waive nationally certain restrictions in public insurance programs it governs (including the telehealth restrictions that are allowed to be waived in emergency areas in the first response bill). It also frees up a $50 billion Disaster Relief Fund to be spent. There is no cost estimate for waiving the restrictions, and the amount spent from the relief fund depends on how it is deployed. The available funding was later increased by $45 billion by the CARES Act (above). Declaring a national disaster allows some of the other actions to be taken, such as delaying tax deadlines and freeing up $44 billion later allocated to boosting state unemployment benefits (below).

Allow High-Deductible Plans to Pay for COVID Testing and Treatment

In addition, the Internal Revenue Service (IRS) announced on March 11 that high-deductible insurance plans can cover COVID tests and treatment without jeopardizing their tax status. This policy interacts with the second response bill's provision requiring no cost-sharing for COVID tests and potential future policies requiring no cost-sharing for treatment.

Delay the Tax Filing Deadline

Treasury Secretary Steve Mnuchin announced on March 17 that tax filers are able to file up to 90 days beyond the April 15 deadline without penalty, affecting an estimated $300 billion of tax payments. Payments of up to $1 million for individuals and $10 million for businesses can be deferred until July 15. On March 20, Secretary Mnuchin announced that the filing deadline in general will be moved back to July 15. This policy will have almost no cost other than a small amount of interest costs associated with the delay since only the timing of the payments will be affected. Other IRS deadlines are also being extended, including providing more time to receive building rehabilitation investment credits, relaxing rules for opportunity zone investors, and delaying excise tax payments for certain sporting goods.

Advanced Payments to Health Providers

Beginning on March 28, Centers for Medicare & Medicaid Services (CMS) through their Accelerated and Advance Payment (AAP) Program started taking applications for up to $100 billion in advanced payments to health providers across the country. CMS announced on April 26 that it would stop taking applications for Part B suppliers in light of the additional money available for health providers under the $175 billion provider relief fund through the CARES Act. The Program provided $59.6 billion in advance payments to Part A providers and $40.4 billion to Part B suppliers; repayments begin 120 days after loan receipt.

Institute a Moratorium on Federal Student Loan Interest

On March 13, President Trump announced that the Department of Education will waive interest on federal student loans during the COVID emergency. This move will not necessarily change the monthly payments that borrowers owe, but it would enable them to pay down their balances more quickly. The Education Department followed up with a release on March 20 stating that interest rates will be set to zero and student loan payments will be suspended for at least the next 60 days. This policy was superseded by the CARES Act, which suspends student loan payments and interest accrual for six months.

Institute a Moratorium on Evictions and Foreclosures for FHA-Backed Mortgages

On March 18, the Department of Housing and Urban Development (HUD) announced a 60-day moratorium on evictions and foreclosures in properties with federally-backed mortgages. This policy will have little cost since it is temporary and does not affect monthly payments. This policy was superseded in the CARES Act, which also allowed those with federally-backed mortgages to request mortgage forbearance for up to six months with the possibility of an extension for another six months. The moratorium was extended for an additional 60 days on June 17, 2020.

Reimburse health providers for self-isolation counseling

On July 30, CMS and CDC announced that they would start to reimburse health providers and physicians who provide counseling on self-isolation to patients who come in for a COVID test. Reimbursement will be offered irrespective of whether the counseling is given on or off-site.

Expansion and extension of Provider Relief Fund deadlines

On July 31, HHS announced that it would be extending the Phase 2 general distribution deadline for Medicaid, Medicaid managed care, Children's Health Insurance Program (CHIP) and dental providers. This $15 billion distribution is part of the Provider Relief Fund, funded by appropriations from the CARES and Paycheck Protection Program and Health Care Enhancement Acts. HHS also announced that it would extend the application deadline for health providers who experienced difficulties in submitting an application for the $20 billion portion of the Phase 1 Medicare General Distribution. Both deadlines are extended through August 28, 2020.

Expansion of telehealth services and changing payments to rural providers

On August 3, President Trump issued an executive order that would see a shift to an “innovative payment model” for rural health providers to be announced within 30 days of the executive order intended to encourage “high-quality, value-based care” and provide flexibility when it comes to current Medicare rules. The executive order also requires the HHS Secretary to issue a regulation within 60 days that would extend telehealth services for Medicare beneficiaries beyond the duration of the public health crisis and requires the Secretary of Agriculture to come up with a strategy to use existing appropriations to invest in rural physical and communications health care infrastructure.

Expansion and extension of federal unemployment payments

On August 8, President Trump issued an executive order that would redirect up to $44 billion of existing funding within the Disaster Relief Fund to create a new program to pay an additional $400 per week to those already receiving at least $100 per week through state unemployment benefits. Governors could request the additional funds from the Federal Emergency Management Agency. Like other disaster funding, states would be required to provide a 25 percent match, for which the order encourages states to use their unspent funds from of the Coronavirus Relief Fund, or other state funds, for their $15 billion. As of June 30, about 25 percent of these funds had already been spent, though states may have allocated a much greater share to future costs. The enhanced benefits go through the first week in December, or until funds expire. We estimate that the program would have sufficient funding for five weeks of benefits (through August 29). Because the money was already appropriated to the Disaster Relief Fund, some by the CARES Act and some by previous legislation, this money could have been spent already so choosing it to spend on unemployment will have no additional deficit impact.

Employee-side payroll tax deferral

On August 8, President Trump issued an executive order that instructs the Treasury Department to defer the withholding and payment of the 6.2 percent Social Security tax paid by employees for any employee making less than approximately $100,000 annually. The employer-side payroll taxes (both Social Security and Medicare) are already deferred, at an employer's discretion, by the CARES Act. It is not clear how many employers would choose to defer withholding of taxes that they will still owe, but we estimate that up to $100 billion could be delayed. Because most of these taxes would be repaid later, we estimate a deficit impact of roughly $5 billion.

Student loan payments and interest deferral

On August 8, President Trump issued an executive order that continues relief from a previous executive order and in the CARES Act to extend from September 30 a deferral on student loan payments and 0 percent interest rate through December 31. We estimate approximately $20 billion of payments will be deferred, but because the amount is due later, the deficit impact from the delay would be about $5 billion.

Review of homeowner and renter assistance

On August 8, President Trump issued an executive order that directs the Departments of Treasury and Housing and Urban Development to identify funds to provide financial assistance to assist renters and homeowners, promote their ability to avoid foreclosure, and review existing authorities to prevent evictions. This order does not provide specific dates or dollar amounts or reinstate the federal eviction moratorium.

Federal Reserve Actions

Cut the Federal Funds Rate and Repeal Reserve Requirements.

In two different moves, the Federal Reserve reduced the federal funds rate to near zero as it was for years following the Great Recession. The Federal Open Market Committee (FOMC) first lowered the rate from 1.5-1.75 percent to 1-1.25 percent on March 3, then lowered it further to 0-0.25 percent on March 15. Effective March 26, the Federal Reserve eliminated reserve requirements for all banks in an attempt to increase lending and liquidity.

Increase Long-Term Treasury Security Holdings

On March 12, the Fed announced the purchase of $60 billion of Treasury securities over the next month. On March 15, along with cutting the fed funds rate to near zero, the FOMC announced the purchase of $500 billion of Treasury securities, as well as the reinvestment of principal back into those securities. On March 23, the Fed announced that the security purchases would increase to be as large as needed to support market functioning, and the New York Fed stated the same day that it planned to purchase $75 billion of Treasury securities per day. These are the first major Fed increases in these holdings since a round of quantitative easing that ran from 2012 through 2014.

Though the Fed initially purchased $75 billion per day of Treasury securities, the purchasing schedule fell significantly since early April. On June 10, the New York Fed announced that it planned to buy $80 billion per month of Treasuries going forward.

Increase Mortgage-Backed Security Holdings

In addition to purchasing long-term Treasury securities, the Fed started purchasing mortgage-backed securities as it did following the Great Recession. On March 15, the FOMC announced the purchase of $200 billion of mortgage-backed securities. On March 23, the Fed announced that the security purchases would increase to be as large as needed to support market functioning and that the purchases would also involve commercial mortgage-backed securities. The New York Fed stated the same day that it planned to purchase $50 billion of mortgage-backed securities per day. These are the first major Fed increases in these holdings since a round of quantitative easing that ran from 2012 through 2014.

Though the Fed initially purchased $50 billion per day of mortgage-backed securities, the purchasing schedule fell significantly since early April. On June 10, the New York Fed announced that it planned to buy $40 billion per month of mortgage-backed securities going forward.

Increase Overnight Repo Operations

The Fed uses repurchase agreements, or repos, to stabilize short-term funding for financial institutions through short-term collateralized loans. The Fed had instituted repo operations in September 2019 to address market turmoil at the time. On March 9, the Fed increased its daily overnight repo operations, where loans last for one day, from $100 to $150 billion. On March 11, the Fed again increased its daily overnight repo operations to $175 billion and instituted three one-month term repo operations of $50 billion each. On March 16, the Fed announced an additional $500 billion of overnight repos to be conducted that day, which were extended the next day to twice-daily operations through March 20. On March 20, it extended the $500 billion of twice-daily overnight repos through April 13, and on April 13, the New York Fed announced an extension through May 4. After that date, the Fed pared down operations to be held daily rather than twice per day.

Notably, the numbers above and in subsequent repo operations sections represent upper limits on repo operations. Actual take-up has been substantially less than these limits and declined significantly after mid-March.

Conduct One-Month Term Repo Operations

In addition to increasing overnight repo operations, the Fed has instituted one-month term operations. On March 11, it announced it would hold three one-month operations of $50 billion each. The following day, it established another $500 billion one-month operation and stated that it would hold weekly one-month operations of $500 billion each through April 13. On April 13, the New York Fed announced an extension of weekly operations for another month, and another extension was made on May 13.

Conduct Three-Month Term Repo Operations

The Fed has also conducted three-month term operations. On March 12, the Fed announced two $500 billion three-month operations and weekly three-month operations of $500 billion each through April 13. The weekly operations were extended on April 13 through May 4, after which operations would be held every other week rather than weekly. On May 13, the New York Fed announced that three-month repos would be discontinued "in light of more stable repo market conditions."

Support U.S. Dollar Liquidity Abroad

On March 15, the Fed announced coordinated action with four other central banks who already conduct regular U.S. dollar operations that they would expand swap line arrangements to enhance dollar liquidity. These swap lines were also On March 31, it announced the establishment of a FIMA Repo Facility, which would undertake repos with foreign central banks' Treasury security holdings to support U.S. dollar liquidity abroad and smooth the functioning of the Treasury market.

Re-Institute Commercial Paper Funding Facility

On March 17, the Fed re-instituted the Commercial Paper Funding Facility (CPFF), which was originally created in 2008 during the financial crisis. The facility supports the commercial paper market that provides short-term financing for companies. There is no specific limit on the size of the facility.

Re-Institute Primary Dealer Credit Facility

On March 17, the Fed re-instituted the Primary Dealer Credit Facility (PDCF), another facility originally created in 2008 that backstops financial institutions who help the Fed implement its monetary policy. There is no specific limit on the size of the facility.

Re-Institute Money Market Mutual Fund Liquidity Facility

On March 18, the Fed re-instituted the Money Market Mutual Fund Liquidity Facility (MMLF), another facility that was originally created in 2008, with the purpose of backstopping money market funds. There is no specific limit on the size of the facility.

Re-Institute Term Asset-Backed Securities Loan Facility

On March 23, the Fed re-instituted the Term Asset-Backed Securities Loan Facility (TALF), another major part of the Fed's 2008 response to backstop the issuance of asset-backed securities. It later stated that TALF would support up to $100 billion of loans.

Establish Primary and Secondary Market Corporate Credit Facilities

In addition to re-instituting several Great Recession-era lending facilities, the Fed established two new facilities on March 23: the Primary Market Corporate Credit Facility (PMCCF) and the Secondary Market Corporate Credit Facility (SMCCF). The primary market facility was formed to backstop new corporate bond and loan issuance while the secondary market facility was formed to provide liquidity for existing corporate bonds. The facility will begin functioning on April 6 and will run for six months. The Fed later stated that the two facilities would support up to $750 billion of loans, with $75 billion of equity coming from CARES Act funding.

Establish Municipal Liquidity Facility

On April 9, the Fed announced a Municipal Liquidity Facility (MLF) to purchase up $500 billion of short-term bonds from states, counties with more than 2 million people, and cities with more than 1 million people. The facility would get $35 billion of credit protection from the CARES Act funding for Fed facilities to support this lending. On April 27, the Fed expanded the facility to include counties with more than 500,000 people and cities with more than 250,000 people. On June 3, the Fed again expanded the facility to make at least two cities or counties eligible in each state while allowing Governors to designate two government-related agencies such as public transit agencies and utility companies to be eligible.

Establish Main Street Business Lending Program

On March 23, the Fed announced that it would establish a Main Street Business Lending Program to support lending to small and medium-sized businesses, "complementing efforts by the SBA." On April 9, it provided further details on the program, stating that it would purchase 95 percent of loans from banks to businesses with fewer than 10,000 employees or $2.5 billion in annual revenue up to $600 billion in total loans. The program would be backed with $75 billion of CARES Act funding. On April 30, the Fed expanded the program to increase the business thresholds to 15,000 employees or $5 billion in revenue and lower the minimum loan size from $1 million to $500,000. It also announced a new loan option that would allow for larger maximum loans in exchange for lenders retaining a larger share of the loan. On June 8, the Fed again expanded the program to lower the minimum loan size to $250,000, increase the maximum loan size, set the Fed's ownership share for all loans at 95 percent, and make the repayment terms more generous.

Establish Paycheck Protection Program Loan Facility

On April 6, it announced that it would establish a Paycheck Protection Program Loan Facility to backstop loans issued through the Paycheck Protection Program (PPP) established in the CARES Act. There is no limit established for the facility, though it would effectively be limited to the size of PPP itself.

0 This legislation would increase usage of the PPP program and the cost of the payroll tax delay. However, previous CBO estimates already assumed the PPP program would be fully subscribed so we assume this legislation’s additional cost has already been incorporated in previous estimates.

1 Represents amount disbursed plus the scheduled pace of purchases, currently about $55 billion for long-term Treasuries and $62 billion for mortgage-backed securities.

2 CBO originally estimated this provision would cost $176 billion in total. Given that spending has already exceeded this threshold, we updated our estimate of total spending to $200 billion.

3 CBO originally estimated this provision would cost $35 billion, based on the assumption that 5 million people would claim PUA benefits. Given that 12.9 million people are claiming PUA as of the week ending June 13, we updated this estimate to $49 billion reflect newer cost figures from the Department of Labor Office of Inspector General. On August 6 we revised down our disbursed estimate for Pandemic Unemployment Assistance based on reports that states are including retroactive weekly claims in their reported continuing claims totals. We also revised our cost estimates for Amount Allowed and Deficit Impact. For these numbers, we extrapolate our updated cost estimate methodology through December 31, 2020 based on CBO projections of unemployment through the end of the year. These estimates are subject to further revision.

4 Represents total amount Federal Reserve has committed to funding lending facilities so far. The facilities themselves provide up to $1.95 trillion in funding.

5 Includes estimated returns and estimated bank fees. Per a June 25 GAO report, $38.5 billion in loans had been cancelled as of May 31, 2020. We assume $21 billion of the $38.5 billion in returns reported as of May 31, 2020 come from the first tranche, based on the difference between the net approvals reported through the end of June and the intitial report on the first tranche approvals on April 16, 2020. Returned or cancelled loans are made available to be re-loaned, per the Small Business Administrtation.

6 Some of these tax changes provide tax cuts in FY 2020 and 2021 but generate revenue in future years, lowering the overall deficit impact.

7 Publicly disclosed loan eligibility.

8 The legislation appropriates $50 billion toward the EIDL program, which supports $366 billion in lending capacity.

9 Disaster declaration opened up around $45 billion of disaster relief funds and enables spending in other areas of government where policy is tied to an emergency declaration. $44 billion was subsequently redirected toward spending on a weekly $300 federal unemployment payment, per this executive order, signed by President Trump on August 8, 2020.

10 Most of these funds have now been paid back, since the passage of the delayed July 15 tax deadline.

11 Under this provision, the federal government would pay for a $300 increase in states that paid for a $100 increase, up until the $44 billion in funds is exhausted. Assuming all states participate, we estimate funds would last five weeks until the week ending August 29.

12 Represents amount disbursed plus the scheduled monthly pace of purchases, currently $55 billion for long-term Treasuries and $62 billion from July 28 through August 13 for mortgage-backed securities.

13 Represents increase in holdings since February 26

14 Amount disbursed represents current increase since February 26. Peak increase was $299 billion in mid-March.

15 As of May 14, three-month repos are no longer being offered.

16 Supported by CARES Act funding. $75 billion is for the corporate credit facilities, $75 billion is for Main Street lending program, and $35 billion is for Municipal Liquidity Facility.

What's Next

-

Image

-

Image

-

Image