CBO Scores the Senate Health Care Bill

The Congressional Budget Office (CBO) just released its score of the Better Care Reconciliation Act of 2017 (BCRA). This is the Senate's version of the American Health Care Act (AHCA) that was passed by the House of Representatives. The bills in many ways resemble each other, but they differ on the subsidy structure for the individual market. You can read our quick take of the differences between the two here (though some small changes have been made to the BCRA).

| Provision | 2017-2026 Cost / Savings (-) | |

|---|---|---|

| AHCA (House) | BCRA (Senate) | |

| End Mandate Penalties | $210 billion | $210 billion |

| Reduce Current Law Spending and Tax Subsidies | -$1.57 trillion | -$1.52 trillion |

| Enact New Spending and Tax Subsidies | $687 billion | $438 billion |

| Repeal ACA Taxes | $553 billion | $550 billion |

| Total Deficit Impact (Conventional Scoring) | -$119 billion | -$321 billion |

Among the key findings of today's report:

- The BCRA would reduce deficits by $321 billion through 2026 under conventional scoring; the House-passed AHCA would reduce deficits by $119 billion.

- The BCRA's $321 billion of savings is the result of a $1.52 trillion reduction in the cost of spending and tax subsidies with most of the funds used to pay for replacement coverage provisions ($438 billion), repeal of the mandate penalties ($210 billion), and rollback of the ACA's tax hikes ($550 billion).

- On net, the BCRA would reduce outlays by $1.02 trillion and revenue by $701 billion through 2026; the House-passed AHCA would reduce outlays and revenue by $1.1 trillion and $990 billion, respectively.

- Today's version of the bill contains a few changes from the version released last Thursday. In particular, it adds a requirement that individuals who chose not to purchase insurance or lapsed coverage for two or more months must wait six months before being eligible again.

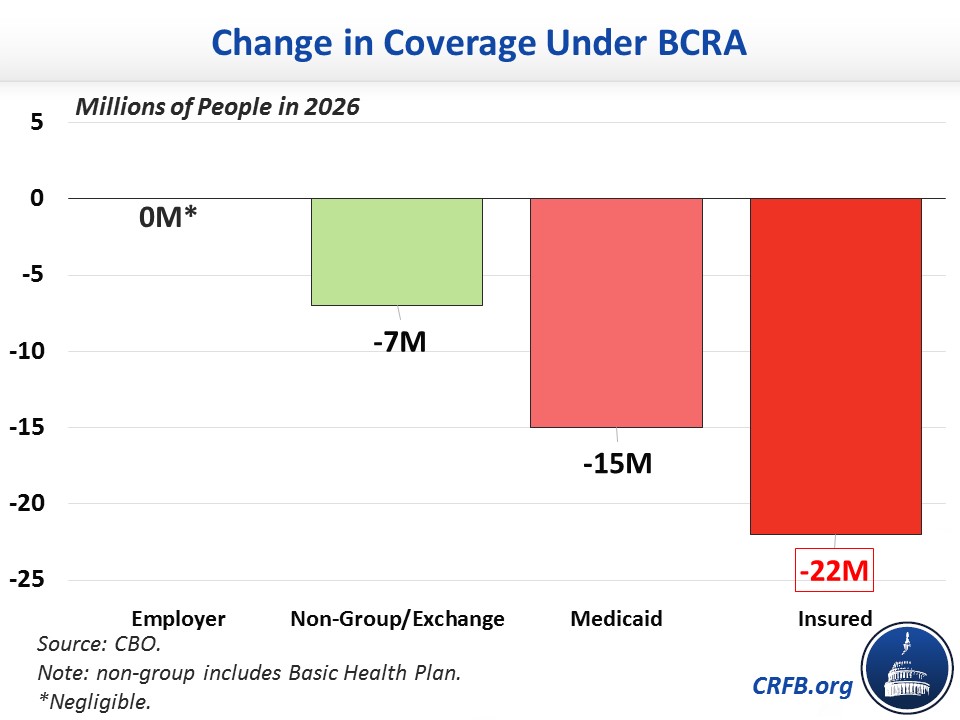

- In terms of coverage, CBO projects the BCRA would reduce the number of Americans with health insurance by 15 million in 2018 and by 22 million in 2026. That compares to 14 million and 23 million, respectively, in the case of the AHCA.

- The 22 million reduction in 2026 is the result of 15 million fewer Medicaid beneficiaries and 7 million fewer with private non-group insurance, including insurance subsidized on the exchanges.

- CBO has not completed an estimate of the macroeconomic effects of the BCRA. In our assessment, the legislation would likely improve growth slightly under CBO's model but less so than the modest growth we expected from the House-passed AHCA.

- CBO has not completed a second-decade estimate of the BCRA, but it does estimate that the legislation would reduce future deficits. Given the $100 billion of deficit reduction in 2026, the stringent cap on per enrollee Medicaid cost growth, and the return of the Cadillac tax in 2026, we expect substantial deficit reduction in the second decade – possibly much more than the $2 trillion of two-decade savings we estimated from the original House bill.

The table below breaks down the major elements of the CBO score.

| Provision | 2017-2026 Cost / Savings(-) | |

|---|---|---|

| AHCA (House) | BCRA (Senate) | |

| Reduce Individual Mandate Penalty to $0 | $171 billion | $171 billion |

| Reduce Employer Mandate Penalty to $0 | $38 billion | $38 billion |

| Subtotal, End Mandate Penalties | $210 billion | $210 billion |

| Repeal ACA Premium and Cost-Sharing Subsidies in 2020 | -$665 billion | -$657 billion |

| Reduce ACA Medicaid Match to Base Medicaid Rate for “Expansion” Beneficiaries, Establish Per-Capita Caps, & Institute Optional Work Requirements | -$834 billion | -$772 billion |

| Other Reductions | -$47 billion | -$69 billion |

| Coverage Interactions | -$23 billion | -$21 billion |

| Subtotal, Reduce Spending and Tax Subsidies | -$1.57 trillion | -$1.52 trillion |

| Establish New Premium Tax Credits in 2020 | $375 billion | $233 billion |

| House Placeholder for Credit Expansion (Reduce the Medical Expense Deduction Floor from 7.5% to 5.8%) | $90 billion | |

| Create State Stability and Innovation Funds | $117 billion | $107 billion |

| Repeal Disproportionate Share Hospital Payment Cuts (Medicare & Medicaid) | $74 billion | $61 billion |

| Expand Health Savings Accounts | $19 billion | $19 billion |

| Other Costs | $11 billion | $18 billion |

| Subtotal, Increase Spending and Tax Subsidies | $687 billion | $438 billion |

| Repeal ACA 3.8% Net Investment Income Tax (NIIT) | $172 billion | $172 billion |

| Repeal ACA Health Insurer Tax | $145 billion | $145 billion |

| Repeal ACA Medicare Hospital Insurance 0.9% Surtax Starting in 2023 | $59 billion | $59 billion |

| Delay ACA “Cadillac Tax” Start Date to 2026 | $66 billion | $66 billion |

| Repeal Most Other ACA Tax Increases | $112 billion | $109 billion |

| Subtotal, Repeal ACA Taxes | $553 billion | $550 billion |

| Total Deficit Impact | -$119 billion | -$321 billion |

Source: Congressional Budget Office and Joint Committee on Taxation. Note: numbers may not add due to rounding.

The biggest changes in the cost estimate of this bill versus the AHCA come from the change in individual market subsidies, in which the BCRA's subsidies cost substantially less – between $140 billion and $230 billion less, depending on how it is measured – than the AHCA's subsidies. Partially offsetting this effect, the BCRA reduces Medicaid by about $50 billion less than the AHCA over ten years, though reductions would be larger starting in 2025 and by increasing amounts over the long term due to the slower growth rate of the per-capita cap.

CBO estimates the bill would increase the uninsured by 22 million in 2026. This is a result of 15 million fewer on Medicaid and 7 million from the individual market. Employer coverage would change only negligibly on net. The chart below shows how much coverage would change in 2026 compared to current law under the ACA.

Below is a chart showing the various proposals and their effects on the number of uninsured:

Importantly, CBO’s estimates do not incorporate future changes that could be made to insurance market rules, either by regulation or through further legislation. Such changes have the potential to increase total insurance coverage, but increasing coverage would also likely reduce the net savings.

Continue to visit CRFB's health care page for further ongoing analysis.

Further Readings: