CBO's 2019 Long-Term Budget Outlook

Today, the Congressional Budget Office (CBO) released its Long-Term Budget Outlook, again confirming the budget’s unsustainable long-term trajectory. Under its baseline, CBO projects federal debt held by the public will reach a new record as a share of the economy in less than two decades and will nearly double as a share of Gross Domestic Product (GDP) in three decades. If current tax cuts and spending increases are extended, debt will nearly triple in 30 years.

CBO’s report shows:

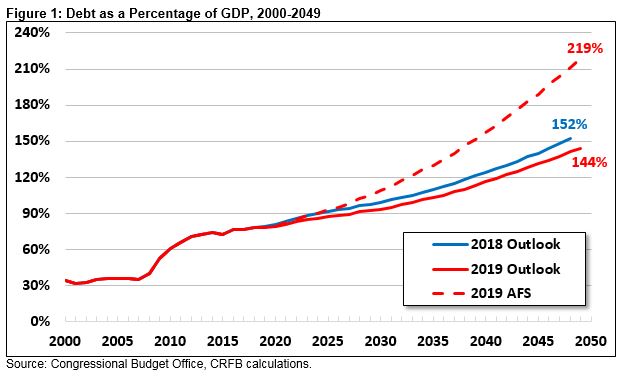

- Debt is Rising Unsustainably. Under current law, CBO projects federal debt held by the public will rise from 78 percent of GDP this year to 144 percent by 2049 – more than a third higher than the historic record of 106 percent set just after World War II.

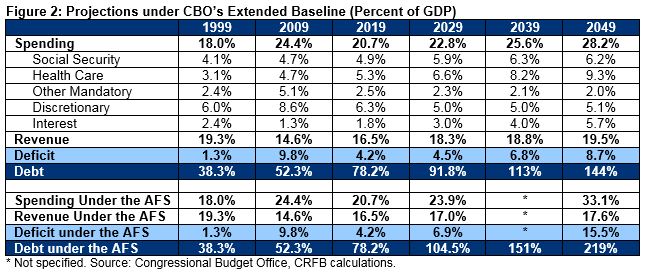

- Spending is Growing Faster than Revenue. CBO projects spending will grow rapidly, from less than 21 percent of GDP in 2019 to over 28 percent by 2049. Revenue will grow more slowly, from 16.5 percent of GDP this year to 19.5 percent by 2049. As a result, annual deficits are expected to more than double from 4.2 percent of GDP in 2019 to 8.7 percent by 2049.

- Recent Legislation Will Substantially Worsen the Long-Term Outlook if Extended. Under current law, large parts of the Tax Cuts and Jobs Act (TCJA) will expire, as will the substantial spending increases enacted in the Bipartisan Budget Act (BBA) of 2018. Extending these and other expiring provisions would increase debt by over 50 percent, to 219 percent of GDP, by 2049.

- Major Trust Funds Are Headed Toward Insolvency. CBO projects the Highway, Pension Benefit Guaranty Corporation Multi-Employer, Medicare Hospital Insurance, Social Security Disability Insurance, and Social Security Old-Age and Survivors Insurance trust funds will all be exhausted in the next 13 years without action to stabilize their finances.

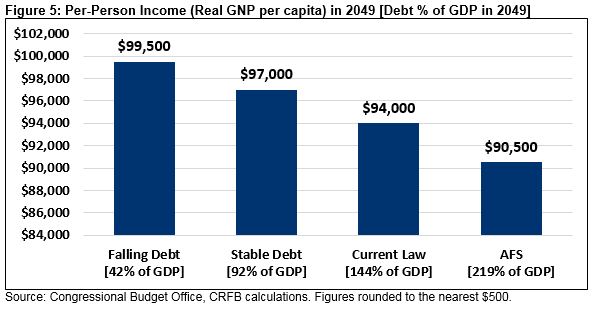

- High and Rising Debt Will Have Adverse and Potentially Dangerous Consequences. CBO estimates that income per person would be almost $9,000 higher in 2049 if we fix the debt compared to continuing current policy as in CBO’s alternative scenario. As we’ve written before, rising debt will slow income growth, increase interest payments, place upward pressure on interest rates, weaken the ability to respond to the next recession or emergency, place an undue burden on future generations, and heighten the risk of a fiscal crisis.

- Fixing the Debt Will Get Harder the Longer Policymakers Wait. Delaying necessary deficit reduction means larger spending cuts and tax increases concentrated on fewer people. CBO estimates the size of the adjustment would grow by 50 percent if policymakers wait ten years to take action.

Debt Is Rising Unsustainably

Debt held by the public will total 78 percent of the economy by the end of 2019 – a six-decade record and nearly twice as high as the 50-year average of 42 percent of GDP – and debt will grow rapidly from there with no end in sight. Debt will continuously rise as the population ages, interest costs rise, and health spending continues to grow.

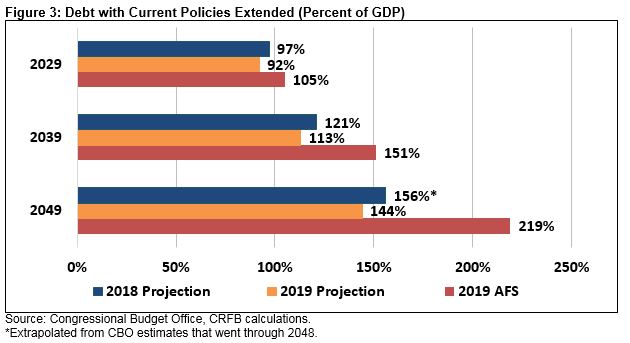

Under current law, CBO projects debt will exceed the size of the economy by 2034, surpass the record high by 2037, and be nearly double today’s level at 144 percent of GDP by 2049. Debt will exceed the record high three years later than projected last year, when CBO estimated the nation was 16 years away from reaching this milestone.

Under the Alternative Fiscal Scenario (AFS), which assumes extension of expiring tax cuts and spending increases, debt will exceed the size of the economy by 2028, hit a new record by 2030, total twice the size of the economy by 2047, and reach 219 percent of GDP by 2049.

Annual deficits will also grow rapidly under CBO’s projections. Under current law, deficits will double from 4.2 percent of GDP in 2019 to 8.4 percent by 2047 and reach 8.7 percent by 2049 – close to the post-war record of 9.8 percent set at the height of the Great Recession. Under CBO’s AFS, deficits will reach 15.5 percent of GDP by 2049 – more than 50 percent above the previous post-war record.

Spending Is Growing Faster Than Revenue

Rising long-term deficits are driven by a disconnect between spending and revenue. In particular, spending on Social Security, the major health programs, and interest payments on the debt will grow faster than revenues over the long term.

Over the next three decades, CBO projects spending will grow from 20.7 percent of GDP to 28.2 percent by 2049 – well above the post-war record of 24.4 percent of GDP and even further above the 50-year average of 20.3 percent of GDP.

Revenue will also rise, though not as quickly. CBO projects receipts will grow from 16.5 percent of GDP in 2019 to 18.3 percent by 2029 – due mainly to the expiration of large parts of the TCJA – and will further climb to 19.5 percent of GDP by 2049. The 50-year average for revenue is 17.4 percent of GDP, and the post-war record is 20.0 percent set in 2000.

Revenue growth comes mainly from rising individual income tax revenue, which after the expiration of TCJA provisions is largely due to real bracket creep (incomes grow much faster than the chained CPI, to which tax brackets are indexed) and the increasing effects of the Affordable Care Act’s “Cadillac tax” on high-cost health insurance plans, scheduled to start in 2022.

CBO’s projections of rapid spending growth reflect continued aging of the population, rising health care costs, and increased interest payments on the debt. Over three decades, Social Security spending will rise by 1.3 percent of GDP, health care spending will rise by 4 percent of GDP, and interest will rise by almost 4 percent of GDP – tripling from 1.8 percent of GDP to 5.7 percent of GDP in 2049. All other areas of spending will shrink by a combined 1.7 percent of GDP.

Put another way, the growth in Social Security, health care, and interest on the debt will account for 123 percent of the growth in spending relative to GDP through 2049. By 2041, spending on these three areas will cost more than all available revenue.

Recent Legislation Will Substantially Worsen the Long-Term Outlook if Extended

Recent tax cuts and spending increases have substantially worsened near-term deficits but have a minimal effect on the long-term outlook since they mostly expire under current law. If policymakers choose to extend these provisions, the long-term fiscal outlook will be far worse.

CBO’s AFS assumes most expiring provisions of the TCJA are extended, discretionary spending increases in the BBA 2018 are continued (so total discretionary spending grows with inflation and then GDP), various expired and expiring ”tax extenders” are made permanent, and the Affordable Care Act taxes that policymakers routinely delay or suspend are not allowed to go into effect.

Under the AFS, total spending would rise to 33.1 percent of GDP by 2049 instead of 28.2 percent under current law, and revenue would rise to only 17.6 percent of GDP instead of 19.5 percent. As a result, deficits would reach 15.5 percent of GDP instead of 8.7 percent under current law.

Debt under CBO’s AFS would exceed the size of the economy by 2028 (as opposed to 2034), reach a new record by 2030 (as opposed to 2037), and rise to 219 percent of GDP by 2049 (compared to 144 percent). Such levels of debt are historically unprecedented and have rarely been seen internationally without some kind of crisis. This is especially troubling given the trajectory of debt, which we previously estimated was headed toward 600 percent of GDP after 75 years.

To avoid such high levels of debt, policymakers should abide by the minimum standard of paying for all new initiatives and extensions. That’s why we’ve proposed an illustrative plan to responsibly raise the discretionary spending caps, called for an end to the already expired ”Zombie Tax Extenders,” and opposed unpaid-for extensions or expansions of the TCJA.

All of the Major Trust Funds Are Headed Toward Insolvency

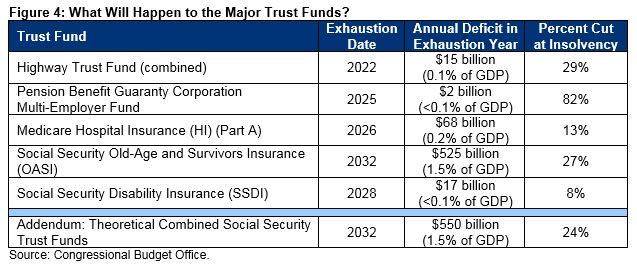

A number of important federal programs are financed through trust funds. Within the next 13 years, CBO projects five major trust funds will exhaust their reserves and become insolvent.

CBO projects the Highway Trust Fund will be depleted by 2022, the Pension Benefit Guaranty Corporation (PBGC) Multi-Employer fund by 2025, the Medicare Hospital Insurance (HI) trust fund by 2026, the Social Security Disability Insurance (SSDI) trust fund by 2028, and the Social Security Old-Age and Survivors Insurance (OASI) trust fund by 2032. On a combined basis, the Social Security trust funds will run out of reserves in 2032.

Upon insolvency, the law mandates that spending be reduced so it equals available revenue to fund these programs. For example, CBO estimates Social Security benefits would be abruptly cut by 24 percent for all beneficiaries regardless of age or income. Medicare’s cut would total about 13 percent.

CBO estimates Social Security’s shortfall will total 1.5 percent of GDP over 75 years and 2.0 percent of the economy in the 75th year (2093). Making the program solvent would require the equivalent of a 33 percent (4.6 percentage point) increase in the payroll tax rate, a 25 percent cut in benefits, or some combination. The sooner lawmakers act the more thoughtful and targeted these reforms can be (see https://www.SocialSecurityReformer.org).

While achieving solvency may not be easy, CBO finds it could have substantial upside. By CBO’s estimates, limiting benefits to revenue would reduce debt from 144 percent of GDP in 2049 to 106 percent of GDP, increase GDP by nearly 2 percent, raise income per person by $3,000 (over 3 percent), and reduce interest rates by 20 basis points. More thoughtful and targeted reforms could be even more pro-growth, while achieving solvency of other trust funds could do even more to slow the growth in debt and increase incomes.

High and Rising Debt Will Have Adverse and Potentially Dangerous Consequences

Reiterating many of the points we made in our piece Why Should We Worry About the National Debt?, CBO warns that high and rising debt could have substantial adverse consequences.

For example, rising debt is likely to slow economic growth and reduce future wages and incomes by crowding out productive investment. CBO estimates that income per person will be $5,500 lower by 2049 under current law as compared to restoring debt to its historic average and almost $9,000 lower under the AFS.

High debt also causes interest rates to rise. CBO estimates the rate on ten-year treasury securities will be 7 percent – 30 basis points – higher as a result of rising debt by 2049. Under the AFS, rates on ten-year Treasuries would be 16 percent – or 70 basis points – higher. These increased rates will spill over into mortgages, car loans, student loans, business loans, and credit card debt.

Rising debt and rates mean rapid growth in interest payments. By 2046, under current law the federal government will spend more on interest than total defense and non-defense discretionary spending. Under the AFS, interest will grow to be the single largest government spending program. Every dollar spent on interest is a dollar unavailable for other priorities.

CBO also points to other costs of high and rising debt, including reduced fiscal space and ability to address a crisis, weaker national security, increased costs of various types of disruptions, and a small but increased risk of a fiscal crisis.

“In a fiscal crisis,” CBO explains,” dramatic increases in Treasury rates would reduce the market value of outstanding government securities, and the resulting losses – for mutual funds, pension funds, insurance companies, banks, and other holders of government debt – could be large enough to cause some financial institutions to fail,“ leading to a global financial crisis.

Fixing the Debt Will Get Harder the Longer We Wait

The longer policymakers wait to fix the debt, the harder and costlier it will get.

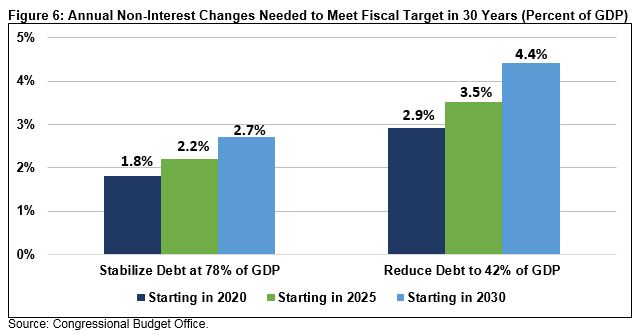

CBO projects maintaining today’s high debt as a share of the economy through 2049 will require annual tax or spending adjustments (excluding interest) of 1.8 percent of GDP if they start in 2020 – the equivalent of $4.7 trillion over a decade. Waiting ten years would make the adjustments even more expensive: 2.7 percent of GDP – the equivalent of $7.1 trillion over the same decade.1

Putting debt on a downward path requires even larger savings. Reducing debt to its 50-year average of 42 percent of GDP would require adjustments of 2.9 percent of GDP today ($7.6 trillion) or 4.4 percent of GDP (the equivalent of $11.6 trillion) if changes aren’t made for a decade.

In either case, a decade of delay would increase the necessary adjustments by about 50 percent.

What could be solved with an 11 percent across the board tax increase or 10 percent spending cut today would require a 16 percent tax increase or 15 percent cut in a decade.

Moreover, delaying action means it must be spread among fewer people, policymakers have less ability to target changes, and ultimately it will be harder to phase in adjustments and give families and businesses time to prepare and adjust for them.

The size of the needed adjustments will also continue to grow over time. At some point, needed changes may become so drastic that policymakers are unwilling to act, absent a crisis.

Conclusion

CBO continues to remind us what we’ve known for years but have chosen to ignore: the federal budget is on an unsustainable course, particularly over the long term. If policymakers make the tough decisions now – rather than wait until there’s a crisis on the horizon – the solutions will be fairer and the costs less painful.

With debt on track to blow through previous records, lawmakers need to stop making a bad situation worse. That means, at the very least, offsetting any new policies and any extensions to recent tax cuts and spending increases. We simply cannot afford to continue the pattern of making temporary policies permanent without paying for them.

CBO’s latest budget and economic projections confirm the fundamental challenges we face: an aging population – which increases the costs of Social Security and Medicare – and slower economic growth. While the economy is growing at roughly 3 percent now and unemployment is at a historic low, this won’t last forever and won’t make our fiscal problems disappear.

There is no magic wand we can wave to fix these problems. Instead, lawmakers must take action to save the trust funds headed toward insolvency and begin to narrow the structural gap between spending and revenue.

Smart and thoughtful deficit reduction enacted today and phased in over time can accelerate economic growth, keep interest rates low, increase future incomes, prevent interest payments from overwhelming the debt, secure the solvency of Social Security and other trust funds, improve generational fairness, create fiscal space, and reduce the risk of fiscal crisis.

Our leaders should start today.

1 These numbers are calculated based on the 2020-2029 window for a direct comparison, even though cuts would not actually begin until 2030.

What's Next

-

Image

-

-

Image