A Plan to Raise the Caps Without Breaking the Bank

Due to the large temporary increase in discretionary spending levels for Fiscal Years 2018 and 2019 in the Bipartisan Budget Act of 2018, spending is projected to fall by 10 percent ($126 billion) next year, returning to the sequester-level caps set under the 2011 Budget Control Act. Unfortunately, existing proposals to avoid these cuts would cost roughly $350 billion over two years – twice as much as simply repealing the sequester – and add about $2 trillion to projected debt levels over the next decade.

Debt is already on an unsustainable path, and policymakers should not worsen the situation by lifting discretionary spending to record levels without offsets. Instead, policymakers should chart a reasonable and responsible path for discretionary spending through a new multi-year cap regime that is fully offset with mandatory spending reductions and/or new revenue.

There are many options available to offset these costs, including numerous policies put forward by President Trump, President Obama, or both (see appendices). In this paper, we present an illustrative plan based on policies with bipartisan appeal.

Our illustrative plan would:

- Increase the caps through a two-year spending freeze at FY 2019 levels, at a cost of roughly $225 billion over ten years.

- Offset the cap deal with bipartisan deficit reduction, including $75 billion each in spending cuts, tax revenue, and offsetting receipts.

- Extend the caps through 2029 and offset the cost. We suggest freezing spending through 2023, growing it with inflation thereafter, and enacting $350 billion in bipartisan health reforms and fixes to the 2017 tax law.

- Improve the integrity of the caps and facilitate future budget deals by placing limits on tactics to evade or spend above the spending caps and formalize a process to offset future cap increases with alternative savings.

In addition to setting discretionary spending levels for at least FY 2020, policymakers must raise or suspend the debt limit to avoid the threat of a potentially catastrophic default. Rather than simply enacting a one-time increase, we propose replacing the debt limit with a new process to limit debt through a series of fiscal targets.

Importantly, this plan is an illustrative example of responsible action and does not provide the definitive roadmap. Whatever spending levels policymakers choose, they must offset the cost to prevent a bad fiscal situation from becoming worse.

The Cost of Current Policy

The Bipartisan Budget Act (BBA) of 2018 increased spending by 16 percent between 2017 and 2019 but allows for a 10 percent spending drop in 2020. Avoiding this cliff by continuing current spending levels in real terms would add about $2 trillion in debt over the decade. Neither outcome is acceptable.

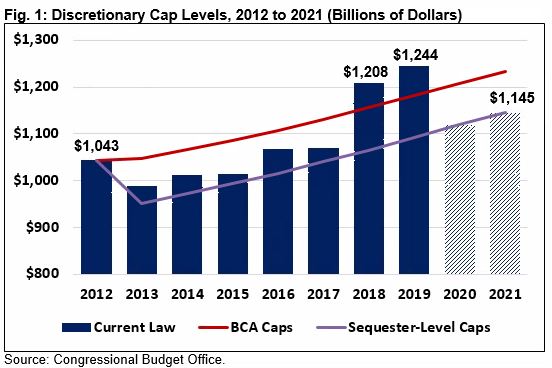

Since 2012, discretionary spending levels have been set through the Budget Control Act (BCA) of 2011, which established defense and non-defense discretionary spending caps that both parties saw as reasonable. Those caps were reduced by roughly $90 billion per year to ‘sequester levels’ after a broader debt reduction plan failed to materialize. Between 2013 and 2017, policymakers increased caps to between these two levels, offsetting the cost above sequester levels.

Unfortunately, lawmakers broke this trend in the BBA 2018, increasing the discretionary caps by $153 billion in 2019 alone – $62 billion more than simply reversing the sequester – and bringing discretionary spending to near-record levels. More troubling, they failed to offset the cost, making future generations pay for it by adding it to the national debt.

Some lawmakers want to continue this practice by increasing spending levels in 2020 and 2021 to above 2019 levels. Because the current caps end after 2021, the Congressional Budget Office (CBO) will assume discretionary spending grows with inflation from 2021 levels, and that assumption will effectively become the new baseline for future discretionary changes.

As a result, growing 2019 levels with inflation through 2021 would ultimately add about $2 trillion in projected debt over the next decade, twice as much as simply repealing the sequester and comparable to the cost of the 2017 tax cuts. This change would increase projected debt from 92 percent of Gross Domestic Product (GDP) at the end of 2029 to 99 percent.

A Realistic and Responsible Path Forward

Rather than enacting a massive spending increase without offsets or allowing an abrupt reduction in military spending and domestic government services, policymakers should aim to strike a balance that ensures adequate spending but does not add to the debt. The best approach would be to establish a new set of caps over the next decade to smooth the transition from current levels of spending to levels policymakers could more easily pay for.

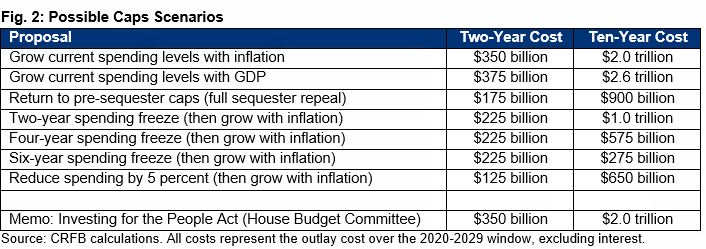

Policymakers could select several paths to achieve this goal. For example, growing current spending levels with inflation would add about $2 trillion in projected debt, while enacting a two-year spending freeze at current levels or returning to the BCA pre-sequester caps would cost about $1 trillion. Extending that freeze for four years would cost $575 billion, and extending it for six years would cost $275 billion – saving money in the second half of the decade.

In each case, the first two years represent the direct cost (over a decade) whereas the next eight years represent the indirect cost imposed by CBO’s baseline assumption. The direct cost of growing the caps with inflation over the next two years is about $350 billion, whereas the cost of freezing spending for the next two to six years is about $225 billion.

While policymakers should set caps for the next decade, they could focus their efforts on setting achievable levels for the next two years and then set placeholder caps that could be adjusted in future budget agreements.

In any case, lawmakers must put forward sufficient offsets to cover the full ten-year cost of their proposed increase. While these offsets do not need to cover all costs in the first year, they should pay for the new spending within a decade and reduce deficits over time by tackling the long-term growth of mandatory spending and lack of sufficient revenue.

The appendices of this paper include two tables of offsets with potential for bipartisan support.

An Illustrative Plan To Raise the Caps Without Breaking the Bank

While there is not one single correct way to responsibly raise discretionary spending caps, we suggest an illustrative plan that would do the following:

- Increase current law caps through a two-year spending freeze at current levels

- Offset the cap deal with bipartisan deficit reduction

- Extend the caps through 2029 and offset the cost

- Improve the integrity of the caps and facilitate future budget deals

Increase the caps through a two-year spending freeze

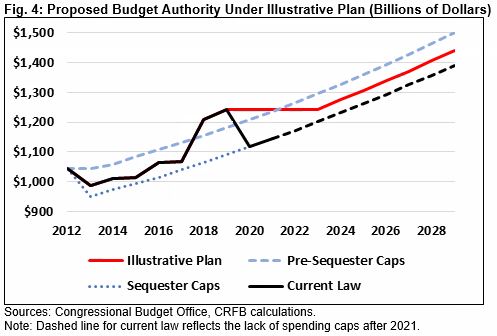

To prevent the 10 percent funding cliff called for under current law, we recommend freezing spending at 2019 levels for at least the next two years. This increase would have a direct cost of about $225 billion, compared to $350 billion if spending grows with inflation.

Importantly, a two-year freeze would still leave 2021 appropriations 16 percent above 2017 levels in nominal terms, 7 percent higher in real terms, and about the same size as a share of GDP. Spending would be about 9 percent higher than current law caps and 1 percent above the pre-sequester caps agreed to on a bipartisan basis in the BCA.

At the same time, a two-year freeze would erode the extremely high real levels of defense and non-defense spending appropriated over the past two years, reducing them from near their record to levels more consistent with recent history. It would also force appropriators to identify efficiencies and targeted spending cuts rather than continue to spend more funds each year.

Offset the cap deal with bipartisan deficit reduction

The $225 billion cost of a two-year spending freeze could be offset with policies that have bipartisan support, many of which appear in budget proposals put forward both by President Trump and former President Obama. While lawmakers could enact any combination of mandatory spending and revenue adjustments they choose, our illustrative plan suggests $75 billion in tax revenue, $75 billion in spending reductions, and $75 billion in offsetting receipts, such as premiums and user fees.

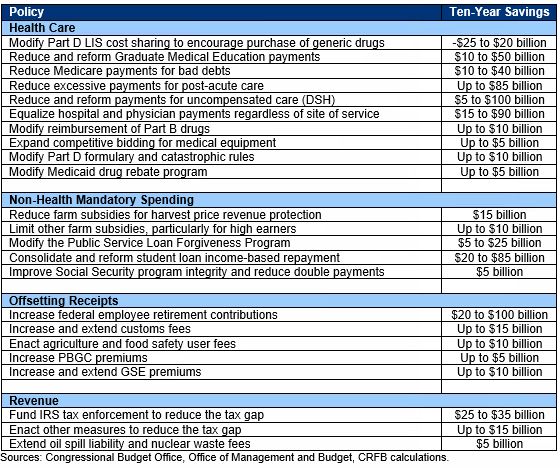

On the revenue side, we suggest policies proposed by Presidents Trump and Obama to reduce the tax gap – the difference between taxes owed and taxes paid – mainly by increasing tax enforcement funding for the Internal Revenue Service (IRS). We also suggest policies both have supported to extend excise taxes for oil spill liability and nuclear waste cleanup. Finally, we suggest closing loopholes that allow earned income to be classified as lower-taxed capital gains or business income.

On the spending side, we propose a number of bipartisan policies to reduce health care spending, including changes that increase the availability of low-cost generic prescription drugs, limit out-of-network surprise billing, and close a loophole that allows hospital-owned physician clinics to receive higher Medicare payments than physician-owned clinics. In addition, we suggest extending the mandatory spending sequester, which reduces Medicare and other spending through 2027 but then expires. Lastly, we suggest adopting some modest proposals from President Trump’s latest budget to reduce waste, fraud, and overpayments throughout government and limiting farm subsidies, mainly for higher earners.

The largest offsetting receipts in our illustrative proposal come from extending the current freeze on the income threshold for Medicare means-tested premiums, which expires after this year, for two years, slightly increasing the number of high-income beneficiaries who pay higher premiums. We also suggest extending and increasing customs fees and Transportation Security Administration (TSA) fees; increasing premiums for the Pension Benefit Guaranty Corporation (PBGC), Fannie Mae, and Freddie Mac; increasing food safety user fees; selling and charging user fees for spectrum; and enacting a number of other small proposals.

Extend the caps through 2029 and offset the cost

Our unsustainable fiscal outlook requires long-term discipline throughout the budget. The discretionary spending caps should be extended at least through 2029 at a level that is both responsible and achievable, and any increases relative to CBO's current law projections should be offset with changes to mandatory spending and/or revenue.

Our illustrative plan assumes the suggested spending freeze will continue through 2023, bringing discretionary spending levels about halfway between pre-sequester and post-sequester levels, which is where they were every year between 2013 and 2017. Doing so would cost an additional $350 billion through 2029 ($575 billion in total spending increases), including $45 billion in 2029. Lawmakers could further increase spending so long as they offset the increase with other spending or revenue adjustments.

We suggest three sources to cover the $350 billion cost. First, our illustrative plan would reduce Medicare spending on post-acute care and bad debts as proposed by both President Trump and President Obama.

Second, our illustrative plan would reverse a recent rule that requires drug rebates in Medicare Part D and Medicaid managed care to be passed directly to consumers; in its place, the plan would enact alternative reforms to reduce Part D drug costs for individuals and the government. These reforms include a hard cap on out-of-pocket spending – proposed by President Trump – and changes to the program’s low-income subsidy (LIS) program – proposed by President Obama – to encourage the use of low-cost generic drugs.

Finally, our illustrative plan would improve the Tax Cuts and Jobs Act (TCJA) by replacing a scheduled amortization of research costs that could slow economic growth (and is unlikely to be allowed to occur) with a limit on the business deductibility of state and local taxes (SALT). The TCJA already caps the SALT deduction for individuals at $10,000, so this change would promote parity and reduce possible gaming under current law.

Improve the integrity of the caps and facilitate future budget deals

In addition to increasing and extending the caps, policymakers should strengthen them. That means establishing clear guidelines and requirements for discretionary spending not subject to the caps, such as Overseas Contingency Operations (OCO), disaster relief, or emergency spending. Cap exceptions should be limited and clearly defined in order to maintain fiscal discipline and transparency.

Lawmakers should explicitly cap OCO spending for future years, phase out the ability of appropriations to rely on phony changes in mandatory spending programs (CHIMPs) that allow discretionary spending to increase without actually reducing mandatory spending, and create new offset rules to require disaster costs be paid for over some period of time.

Lastly, lawmakers should consider designing an explicit process – either through pay-as-you-go rules (PAYGO) or a new regime – to allow future lawmakers to raise discretionary caps in exchange for offsetting revenue or mandatory spending. The current process is ad hoc and, even when consistent with the spirit of the law, is in violation of current budget rules, which must be waived to even allow for a responsible budget deal.

An Illustrative Framework to Replace the Debt Limit

Estimates from CBO and the Bipartisan Policy Center (BPC) find that Congress will need to increase or suspend the statutory debt limit by October or early November of 2019 or else default on some of the country’s obligations. Such a default could result in economic catastrophe, and even coming close to default could shake markets. Policymakers must therefore address the debt limit sooner rather than later; they are likely to do so in combination with a budget cap deal.

Rather than simply increasing or suspending the debt limit, we suggest reforming it. Today’s statutory debt limit suffers from numerous well-known defects that become clearer each year. In addition, the debt limit actually does little to directly prevent debt from growing unsustainably relative to the economy – except by serving as a reminder for policymakers to take action.

We therefore suggest replacing the debt limit with a series of new fiscal targets. Unlike the current debt limit, which is linked to nominal gross debt, these fiscal targets should be economically meaningful and based on fiscal goals that both parties agree to. These could be debt-to-GDP targets focused on stabilizing the debt ratio, or they could be deficit targets. A ten-year transition to structural primary balance (current spending less than current revenue, excluding net interest) would ultimately put debt on a downward path so long as interest rates remain below the growth rate.

In addition to annual targets, lawmakers could consider long-term targets designed to limit future debt growth. For example, they could target reductions in projected debt at some point in the future, narrowing the long-term fiscal gap, or reducing the country’s net liabilities.

Policymakers should include a process to facilitate deficit reduction in order to achieve these targets, which could be a process similar to budget reconciliation, a requirement to vote on presidential recommendations, a commission approach, or something else.

They should also include enforcement. For example, failure to achieve fiscal targets could result in a freeze or reductions to discretionary cap levels as well as mandatory spending and revenue provisions. The more these adjustments reflect small modifications to current policy rather than across-the-board cuts, the more likely they are to work.

Fiscal targets could also be encouraged and enforced by making debt limit repeal conditional on achieving those targets. In the event targets are missed, lawmakers would have to vote explicitly in support of increasing the debt limit.

Conclusion

It would be highly disruptive to allow defense and non-defense discretionary spending to fall by 10 percent to sequester levels, and it would be disastrous to breach the debt limit. However, the need to avoid a spending cliff and raise the debt limit should not be an excuse to add trillions of dollars to the national debt.

Current discretionary spending levels are already at near record-highs, and continuing to grow them at their current pace would be the equivalent of lifting the sequester twice over. Lawmakers should instead transition to more reasonable and affordable levels of spending and, more importantly, they should fully offset the cost by addressing the growth of mandatory spending and raising more revenue.

Lawmakers should also reform or replace the debt ceiling with a mechanism that will better control rising debt as a share of the economy without threatening the full faith and credit of the U.S. government.

Our illustrative plan would responsibly address the pending funding cliff by freezing spending at 2019 levels through 2023, extending caps through 2029, and paying for the cost of these proposals through a mix of spending and revenue changes that enjoy bipartisan support. In the appendix to this paper, we also put forward alternative options to offset a new cap increase. Additionally, we propose to improve the integrity of the caps and facilitate future budget deals through a variety of changes to budget rules.

This paper also puts forward an illustrative framework to replace the debt limit with a new process that would actually serve to more meaningfully limit debt through a series of fiscal targets and a process to achieve those targets.

While these plans are illustrative, they show a responsible path forward. Whatever discretionary spending levels policymakers agree to, their cost must be offset to prevent our unsustainable fiscal outlook from becoming worse.

Appendix I: Offsets Proposed by Both President Trump and President Obama

Appendix II: Other Policies With Potential Bipartisan Support

What's Next

-

Image

-

Image

-

Image