The State and Local Tax Deduction Should Be on the Table

As tax reform gets underway, there will be disagreement about which tax breaks should be eliminated or reformed and which should remain. There is a constituency for each tax expenditure, but many are long overdue for reform, and the more we scale back tax breaks, the more we can accommodate larger rate reductions and other reforms.

The recent tax framework proposes eliminating the state and local tax (SALT) deduction, and despite the pushback, this is a sensible reform for many reasons. The SALT deduction is unjustified, unfair, expensive, regressive, and anti-growth.

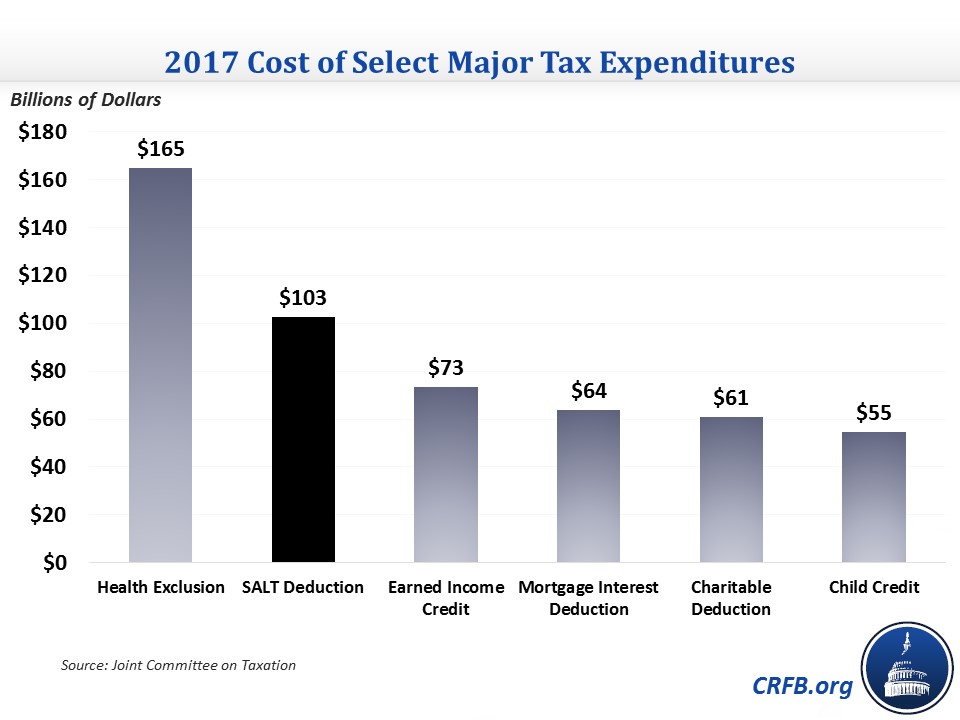

The SALT deduction is expensive and is the most expensive tax expenditure that any recent tax reform effort has aimed to repeal. According to the Joint Committee on Taxation (JCT), the SALT deduction costs over $100 billion this year; by comparison, the mortgage interest and charitable giving deductions, two other large tax breaks, cost $65 billion and $60 billion, respectively. Indeed, under the "Big 6" tax framework released last month, repealing the SALT deduction would raise $1.3 trillion – enough to cover the costs of reducing individual tax rates to 12, 25, and 35 percent or pay for doubling the standard deduction and expanding the child tax credit. This is the second-largest revenue-raiser in the proposed reform.

The SALT deduction is unjustified because it allows individuals to deduct costs that largely go to pay for goods and services they benefit from. While some argue state and local taxes should be deductible to prevent double taxation, in reality no such phenomenon is occurring. People pay federal taxes in exchange for federal services – the military, interstate highways, and Medicare, for example; they pay state and local taxes for state and local services – education, public parks, and law enforcement, for instance. Those services are not taxed when provided, nor are state and local transfer payments. Removing the deduction therefore does not lead to double taxation, but rather single taxation. A basic principle of taxation is that all income (or consumption goods under a consumption tax) should be taxed exactly once. Removing the SALT deduction helps accomplish this goal.

The SALT deduction is unfair because it disproportionately subsidizes states and localities with higher earners and higher income and property taxes. This unjustifiably rewards high-tax states, and because deductions rise with income (they are worth 39.6 cents per $1 at the top, but only 10 cents or less at the bottom), it also rewards areas with more wealthy taxpayers, even holding state and local tax rates constant. This reality, combined with their large populations, means that California and New York alone accounted for one-third of the value of all SALT deductions claimed in 2014 despite making up just 18 percent of the population. The top six states benefiting from the deduction – California, New York, New Jersey, Illinois, Texas, and Pennsylvania – account for more than half of the cost of the deduction while making up 38 percent of the population.

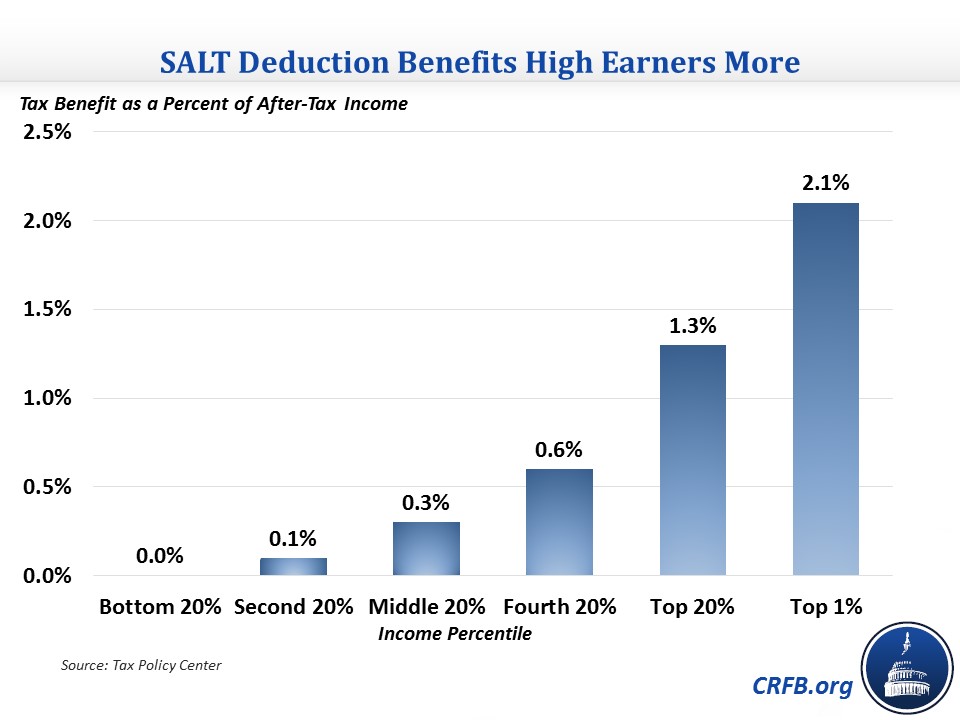

The SALT deduction is regressive since one-third of the benefit of the deduction goes to the top 1 percent of earners and virtually none goes to the bottom half. The SALT deduction is regressive for several reasons: it is only available for the one-third of taxpayers who itemize deductions, it is more beneficial for those who are paying higher state and local taxes, and perhaps most significantly, its benefit goes up with one's tax rate. For a family making $15,000 and paying at the 10 percent rate, each $1 of state taxes leads to a 10-cent reduction in federal taxes. For a family making $1,000,000 and paying at the 39.6 percent rate, each $1 of states taxes results in a 39.6 cent federal tax reduction. In other words, for every $10,000 in taxes a state imposes on high-income earners, the federal government effectively refunds them $3,960.

This regressivity is apparent when looking at the effect of the SALT deduction on after-tax income. While the tax benefit of the SALT deduction is roughly equal to 0.3 percent of income for those in the middle of the income spectrum, it increases to 1.3 percent of income for those in the top fifth and 2.1 percent for those in the top 1 percent. Importantly, when one measures the distributional effect of tax reform they must look at the entire plan; however, absent SALT repeal, it is more challenging to achieve distributional-neutrality and more likely that tax reform overall will be regressive in nature.

Finally, in many ways, the SALT deduction is anti-growth, at least relative to many alternatives. Because of the SALT deduction's cost, statutory tax rates, deficits, or both are higher than they otherwise would be, and state and local taxes are likely higher as well. Either lower tax rates or lower deficits would help to improve economic growth.* Repealing the deduction in exchange for lower tax rates would also improve efficiency more broadly by indirectly reducing the value of economically distorting tax expenditures.

To be sure, SALT has its defenders, and there are real transitional issues policymakers must deal with. For this reason, phasing out the deduction, or perhaps maintaining a much smaller capped deduction for a number of years, might be sensible. Policymakers could also consider addressing the SALT indirectly through an across-the-board tax expenditure cap. But failure to at least significantly pare back the SALT deduction will throw into question the possibility of fiscally responsible individual tax reform. This is why it was eliminated not only in the Big 6 framework, but under recommendations from the 2005 President's Advisory Panel on Federal Tax Reform, the Simpson-Bowles Fiscal Commission plan, the Domenici-Rivlin Debt Reduction Task Force plan, and former Ways and Means Committee Chairman Dave Camp's (R-MI) Tax Reform Act of 2014.

Eliminating or scaling back the SALT deduction makes the tax code cleaner, fairer, more progressive, and more pro-growth than would otherwise be the case, and it is an important element to achieving fiscally responsible tax reform. Rather than working to remove offsets from the Big 6 framework, policymakers should be looking to add offsets and then scale back whatever revenue-reducing provisions they can't afford to fully pay for.

Read more options and analyses on our SALT Deduction Resources page.

*Importantly, trading the SALT deduction for lower rates isn't a pure economic win since the deductibility of income taxes leads to lower effective marginal rates on income. However, property taxes have a much more tenuous relationship to income – a $1,000 or even $10,000 increase in income is unlikely to lead to a direct increase in owned property value. Therefore, depending on the details, trading the SALT deduction for lower statutory rates is likely to result in lower effective marginal rates overall.