Financial Report of the U.S. Government Shows Bleak Picture

Every year, the Treasury Department releases the Financial Report of the United States Government, which provides a detailed picture of the government's finances over the next 75 years. This year's report, released last week, shows a similar outlook as previous years; we are on an unsustainable fiscal path.

The report presents budget numbers in slightly different ways than CBO does. For one, instead of reporting an annual deficit, which was $483 billion in FY 2014, it reports the net operating cost. This measure differs in a few key respects:

- It includes changes in government asset values.

- It measures the increase in debt held by the public, a cash-flow measure, in contrast to the deficit, which uses accrual accounting for credit programs.

- It includes the net liabilities of federal retirement and veterans' benefits (and similar programs).

The net operating cost is usually higher than the deficit, but it was much higher this year at $791 billion. Most of this is reflected in the fact that debt increased by a lot more than the official deficit did.

The Financial Report also measures net liabilities of the federal government over 75 years. In addition to the "net position," which is the stock to the net operating cost's flow (like debt is to deficits), it also separately evaluates the net social insurance liabilities of Social Security and Medicare and total net liabilities for noninterest spending. The current net position is $17.7 trillion, and the total noninterest liability going forward is $4.7 trillion, or 0.4 percent of total GDP over the next 75 years. Within the total noninterest liability is the net social insurance liability of Social Security and Medicare, which is $41.9 trillion (4 percent of 75-year GDP), or $14.1 trillion (1.3 percent of 75-year GDP) if current trust fund balances and Medicare general revenue transfers are counted. These totals are larger in nominal dollars than last year's report but similar as percentages of GDP.

| U.S. Government Assets and Liabilities (billions) | ||

| FY 2014 | FY 2013 | |

| Assets | $3,065 | $2,968 |

| Debt Held by the Public | -$12,834 | -$12,028 |

| Other Liabilities* | -$7,932 | -$7,849 |

| Net Position | -$17,701 | -$16,909 |

| Net Liabilities of Social Security | -$13,330 | -$12,294 |

| Net Liabilities of Medicare Part A (HI) | -$3,823 | -$4,772 |

| Net Liabilities of Medicare Parts B and D (SMI)** | -$24,763 | -$22,632 |

| Net 75-Year Social Insurance Liabilities | -$41,916 | -$39,698 |

| Total 75-Year Noninterest Liabilities | -$4,700 | -$4,000 |

| Memo: Social Insurance Liabilities (Trust Fund Perspective)^ | -$14,108 | -$14,047 |

Source: Treasury Department

*Includes liabilities of federal employee benefits, veterans benefits, and other liabilities.

**Does not include federal general revenue transfers.

^Includes trust fund balances and general revenue transfers.

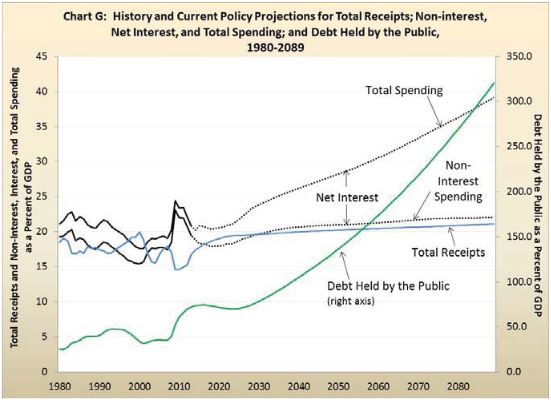

The Financial Report also includes more familiar measures, like the fiscal gap and the path of debt as a percent of GDP. Treasury estimates that the fiscal gap, or the amount of savings needed to keep debt at its current level, is 2.1 percent of GDP, slightly higher than CBO's estimate of 1.8 percent. Treasury also estimates that delaying reforms would make the needed changes larger, increasing the fiscal gap to 2.5 percent and 3.1 percent, if we wait ten and twenty years, respectively. CBO also estimated a significant cost of delay.

Like CBO, Treasury estimates a dramatic rise in debt as a share of economy over the long term. Although the non-interest liability number is a modest 0.4 percent of 75-year GDP, interest spending grows explosively over the long term because of not only that gap, but an increase in interest rates back to more normal levels and the already-existing debt. Under Treasury's projections, debt does decline from 74 percent of GDP in 2014 to 70 percent by 2024, but it quickly rises to 117 percent by 2044 and 321 percent by 2089. This path is clearly unsustainable.

Source: Treasury Department

Like other long-term projections, the Financial Report should throw cold water on the idea that policymakers can be complacent about the debt. Instead, they should use the time they have to make the choices that are necessary to make our long-term fiscal future much brighter.