Error message

There was a problem getting your available contact lists.The Deficit Has Never Been This High When the Economy Was This Strong

This year, the budget deficit is projected to total about $970 billion – 4.6 percent of GDP – up from $666 billion (3.5 percent of GDP) in 2017. This borrowing is virtually unprecedented in current economic conditions.

Normally, deficits rise during recessions and fall during economic expansions. This feature is unsurprising: lower incomes lead to lower tax revenue (and higher spending on programs like unemployment insurance), and policymakers often respond to recessions by enacting economic stimulus.

Rarely have deficits risen when the economy is booming. And never in modern U.S. history have deficits been so high outside of a war or recession (or their aftermath).

This piece shows that all recent years of very high deficits outside of World War II were accompanied by high unemployment, a larger output gap, and a shrinking (or barely growing) economy. This year is abnormal – we are running high deficits despite low unemployment, no output gap, and a growing economy.

Now would be the time to act: today's relatively strong economy offers policymakers the opportunity to reduce deficits without fear of worsening a recession or disrupting a fragile recovery.

Years with Deficits Above 4 Percent Outside World War II

| Fiscal Year | 1934 (1932-1936) |

1976 | 1983 (1983-1986) |

1992 (1991-1992) |

2009 (2009-2013) |

2019 |

|---|---|---|---|---|---|---|

| Budget Metrics (percent of GDP) | ||||||

| Revenue | 4.8% | 16.6% | 17.0% | 17.0% | 14.6% | 16.5% |

| Spending | 10.6% | 20.8% | 22.8% | 21.5% | 24.4% | 21.2% |

| Deficit | 5.8% | 4.1% | 5.9% | 4.5% | 9.8% | 4.6% |

| Debt | 44% | 27% | 32% | 47% | 52% | 79% |

| Economic Metrics | ||||||

| Unemployment Rate | 23% | 7.8% | 10.1% | 7.4% | 8.5% | 3.4% |

| Real GDP Growth for the Previous Year | -- | -1.8% | -2.5% | -0.1% | 0.1% | 3.0% |

| Output Gap (percent of GDP) | -- | -2.8% | -6.3% | -3.5% | -5.9% | 1.0% |

| Immediately After a Recession? | Yes | Yes | Yes | Yes | Yes | No |

Source: CBO, BEA, BLS. For periods where multiple years had deficits above 4 percent (e.g., 2009-2013), the year with the highest deficit is shown. Not all economic metrics available before 1950. Unemployment rate in 1934 available from BLS estimates done in 1948. 2019 totals are CBO projections.

Deficits Should Rise During Recessions, Not Booms

The federal budget deficit has only exceeded 4.6 percent eight times since 1950. Four of those years were during and immediately following the Great Recession of 2009, and the other four followed the 1981-82 recession (which was followed by large tax cuts and a defense buildup near the end of the Cold War). Most smaller spikes in the deficit also took place during or immediately after a war or recession.

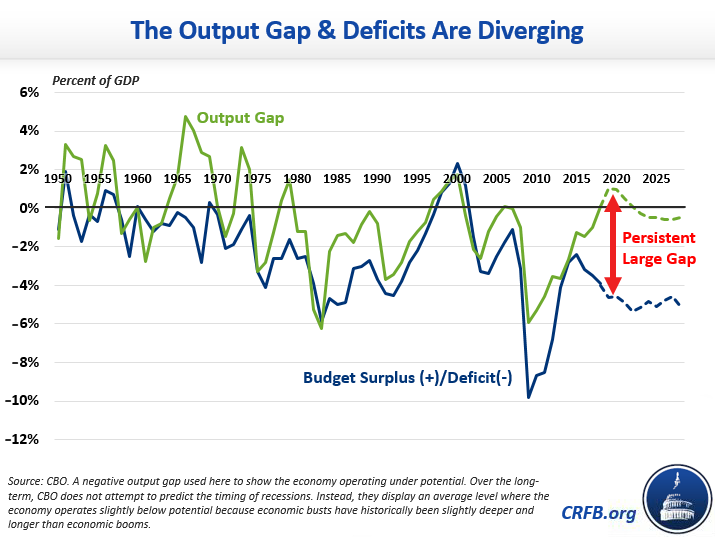

Another measure of economic performance is the "output gap," the amount that the economy is operating below its potential. Throughout modern U.S. history, the output gap and annual deficits have generally moved in the same direction: deficits shrink when the economy is doing well.

Historically, there have been only two other temporary periods when this relationship didn't hold up – in 1968 during the Vietnam War and in the mid-1980s during the military buildup near the end of the Cold War.

Going forward, deficits are projected to rise even assuming the economy remains stable. Under current law, CBO projects deficits in 2028 will exceed 5 percent of GDP, and under a (perhaps more realistic) Alternative Fiscal Scenario that assumes Congress continues recently enacted policies, deficits will reach 7.1 percent of GDP in ten years.

The same pattern holds with employment rates – the deficit has typically moved in the same direction as the unemployment rate. Yet the current unemployment rate of 3.7 percent is the lowest since 1969, and the deficit is high and rising. All other recent periods of high deficits have been accompanied by high unemployment.

Today's Deficits Are Structural and Economically Dangerous

Historically, deficits have been counter-cyclical (meaning they move in the opposite direction of the economy) and largely temporary. Today's deficits are an aberration, unfortunately: both pro-cyclical and permanent.

Running large deficits when the economy is already strong means that any boost provided to the economy will be temporary, and may put unnecessary upward pressure on inflation and interest rates.

Running permanent deficits means that they will increasingly hurt investment and growth over time. They cannot simply be waited out. Rising deficits are largely driven by the increasing cost of interest and health and retirement programs, which are caused by rising health care prices and an aging population. Yet even with these factors, deficits were on course to decline over the next couple years before Congress enacted fiscally irresponsible tax cuts and spending hikes.

Proactive policy action will be needed to turn the situation around. As John F. Kennedy said in 1962 in advocating to prepare the country for the next recession, “Pleasant as it may be to bask in the warmth of recovery…the time to repair the roof is when the sun is shining.” Policymakers must begin reducing deficits and certainly should stop adding to them.