Analysis of CBO’s April 2018 Budget and Economic Outlook

The Congressional Budget Office (CBO) released its ten-year budget and economic outlook today, showing that recent legislation has made an already challenging fiscal situation much worse. CBO’s report projects that:

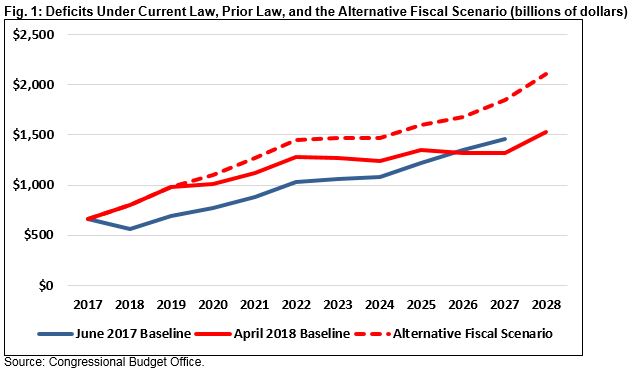

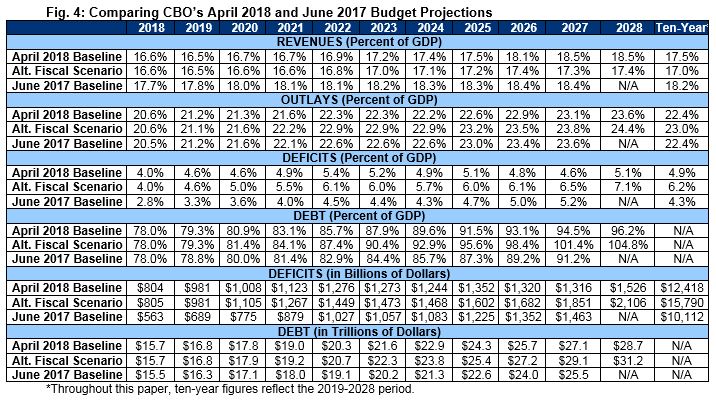

- The budget deficit will near one trillion dollars next year, after which permanent trillion-dollar deficits will emerge and continue indefinitely. Under current law, deficits will rise from $665 billion (3.5 percent of Gross Domestic Product) last year to $1.5 trillion (5.1 percent of GDP) by 2028.

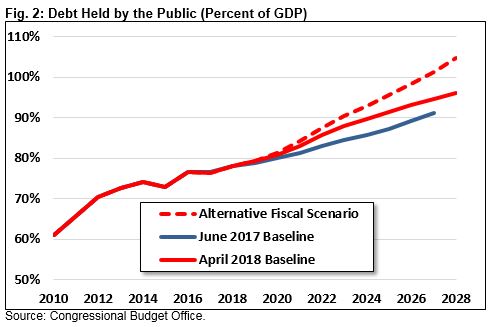

- As a result of these deficits, debt held by the public will increase by more than $13 trillion over the next decade – from $15.5 trillion today to $28.7 trillion by 2028. Debt as a share of the economy will also rise rapidly, from today’s post-war record of 77 percent of GDP to above 96 percent of GDP by 2028.

- Cumulative deficits through 2027 are projected to be $1.6 trillion higher than CBO’s last baseline in June 2017. The entirety of this difference is the result of recent legislation, most significantly the 2017 tax law.

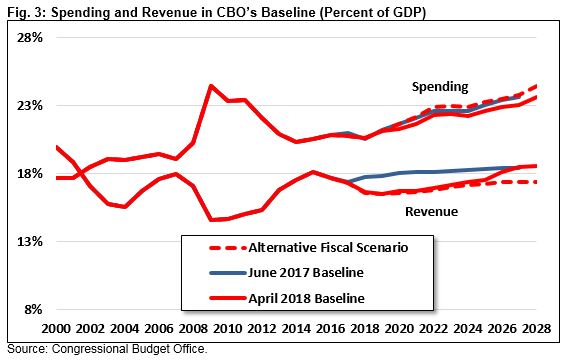

- Spending will increase significantly over the next decade, from 20.8 percent of GDP in 2017 to 23.6 percent by 2028. Revenue will dip from 17.3 percent of GDP in 2017 to 16.5 percent by 2019 before rising to 18.5 percent of GDP by 2028 as numerous temporary tax provisions expire.

- Deficits and debt would be far higher if Congress extends various temporary policies. Under CBO’s Alternative Fiscal Scenario, where Congress extends expiring tax cuts and continues discretionary spending at its current level, the deficit would eclipse $2.1 trillion in 2028, and debt would reach 105 percent of GDP that year – nearing the record previously set after World War II.

CBO’s latest projections show that recent legislation has made an already challenging fiscal situation much more dire. Under current law, trillion-dollar deficits will return soon and debt will be on course to exceed the size of the economy. Under the Alternative Fiscal Scenario, the country would see the emergence of $2 trillion deficits, and debt would reach an all-time record by 2029.

Lawmakers must take prompt corrective action to reverse these deficits. That should include paying for all extensions or new policies, setting reasonable but responsible spending levels, raising new revenue, and reforming major entitlement programs in order to stem the growth of debt.

Deficits and Debt

CBO projects deficits will near the trillion-dollar mark next year and exceed that level every year thereafter. Under current law, deficits will jump significantly in the near term, rising from $665 billion in 2017 to $804 billion in 2018 and $981 billion in 2019. Beyond that, CBO projects nominal dollar deficits to continue to grow steadily to $1.5 trillion by 2028. As a share of the economy, CBO projects deficits will increase from 3.5 percent of GDP in 2017 to 4.6 percent in 2019 and 5.1 percent by 2028.

Under CBO’s Alternative Fiscal Scenario – which assumes many of the 2017 tax law’s expiring provisions and other temporary tax cuts are made permanent, the recent spending deal is extended so that most discretionary spending grows with inflation, and emergency funding for disasters is kept in line with its historical average – deficits will exceed the two-trillion dollar mark by 2028.

Either of these scenarios is substantially worse than what CBO projected in June 2017 prior to the recent tax law and budget agreement. CBO’s previous projections estimated a deficit of $689 billion in 2019, with trillion-dollar deficits not returning until 2022.

CBO’s projections are consistent with those from other forecasters. For example, both CRFB and Goldman Sachs recently estimated budget deficits would reach $1.1 trillion in 2019, and the Treasury’s survey of primary dealers showed a median deficit projection of $965 billion for 2019.

Higher projected deficits, of course, will lead to higher levels of debt. Specifically, CBO projects debt will rise from 76 percent of GDP ($14.7 trillion) at the end of 2017 to 88 percent by 2023 ($21.6 trillion) and 96 percent of GDP ($28.7 trillion) by 2028. Under CBO’s Alternative Fiscal Scenario, debt would reach 105 percent of GDP by 2028, higher than any time in our nation’s history other than in 1946 – immediately after World War II.

These projections are significantly higher than those made in June 2017, when CBO projected debt reaching 91 percent of GDP, or $25.5 trillion, in 2027.

Spending and Revenue

Rising deficits are driven by the disconnect between spending and revenue. Over the next few years, CBO projects spending to rise and revenue to fall as a share of GDP. Over time, CBO projects revenues will recover – both because of the expiration (and instatement) of many provisions in the 2017 tax law and due to real bracket creep that naturally leads revenue to rise – but spending will continue to grow, and revenue will not keep up.

Specifically, spending will increase from 20.8 percent of GDP in 2017 to 21.2 percent in 2019 and 23.6 percent of GDP by 2028. Revenue will decline from 17.3 percent of GDP in 2017 to a low of 16.5 percent by 2019 before rising again to 18.5 percent by 2028. Under the Alternative Fiscal Scenario, spending would reach 24.4 percent of GDP in 2028 while revenue would reach 17.4 percent of GDP.

Spending growth between 2017 and 2019 is driven in large part by a 13 percent, $162 billion nominal increase in discretionary spending. Beyond that, discretionary spending is projected to grow slower than the economy, with a nominal reduction occurring in 2020 after the Bipartisan Budget Act spending increases expire under current law.

Over the course of the next decade, particularly under current law, the vast majority of spending growth will come from health care, Social Security, and interest on the debt. Under CBO’s projections, these three categories account for 81 percent of nominal spending growth between 2017 and 2028 and 144 percent of spending growth as a share of GDP (with other budget categories shrinking).

CBO projects Social Security will grow from 4.9 percent of GDP in 2017 to 6.0 percent by 2028, federal health spending will grow from 5.4 percent to 6.8 percent of GDP, and interest will more than double as a share of the economy from 1.4 percent to 3.1 percent of GDP. Meanwhile, discretionary spending will shrink from 6.3 percent of GDP in 2017 to 5.4 percent by 2028, and other spending will shrink from 2.9 percent to 2.4 percent of GDP.

Under CBO’s Alternative Fiscal Scenario, which assumes the recent budget deal is continued but disaster funding is lower, discretionary spending will remain relatively stable, totaling 5.9 percent of GDP by 2028; interest will rise to 3.3 percent of GDP. Under that scenario, Social Security, health care, and interest will be responsible for 77 percent of nominal spending growth.

On the revenue side, CBO projects individual income tax revenue will remain relatively steady at about 8.3 percent of GDP through 2021, rise gradually to 8.7 percent by 2025, and then rise more rapidly to 9.8 percent of GDP by 2028. Corporate income tax revenue will fall from 1.5 percent in 2017 to 1.2 percent by 2018 before recovering to 1.7 percent by 2025 and shrinking again to 1.5 percent by 2028. Payroll taxes and other sources of revenue will decline slightly as a share of GDP through 2028.

Under CBO’s Alternative Fiscal Scenario, individual income tax revenue would likely remain below 9 percent of GDP and corporate income tax revenue below 1.5 percent. However, these revenue estimates still assume several base-broadening provisions are allowed to go into effect late in the budget window. Absent these provisions, corporate revenue and total revenue would be lower.

Changes in Budget Outlook

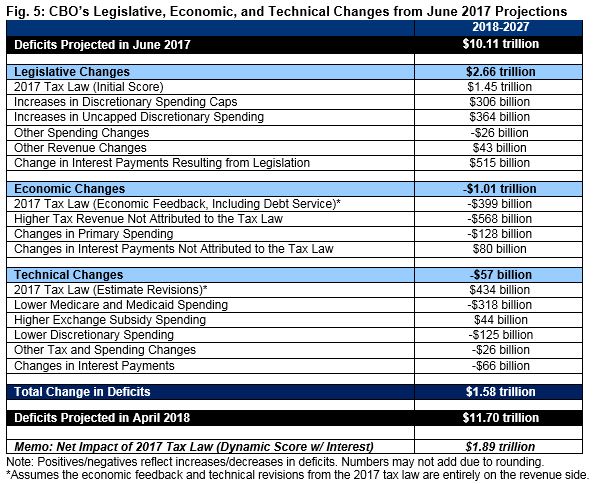

Since June 2017, the budget outlook has deteriorated significantly. Last June, CBO projected deficits to total $10.1 trillion between 2018 and 2027; they now project $11.7 trillion of deficits, a $1.6 trillion increase. This increase can be entirely explained by legislation enacted over the past year.

CBO projects legislative changes added $2.66 trillion to deficits through 2027. The largest contributor to this increase is the 2017 tax law, which was originally scored as costing $1.45 trillion before interest on a conventional basis (this initial score is counted as a legislative change). CBO believes the tax bill will increase GDP by an average of 0.7 percent over the next decade and generate roughly $400 billion of revenue and other economic feedback (counted in the economic section). On the other hand, CBO now estimates the tax law will cost over $430 billion more than the Joint Committee on Taxation (JCT) originally scored under conventional scoring practices (counted as a technical change). On net, CBO estimates the tax bill will add $1.89 trillion to the debt through 2027, including interest.

Other than the tax law, Congress enacted several other costly pieces of legislation. CBO estimates $306 billion more in discretionary spending as a result of the Bipartisan Budget Act and omnibus spending bill and another $362 billion from extrapolated changes in uncapped spending.

The Bipartisan Budget Act generally expires after two years and much of the tax bill after eight years. If these laws were continued, it would add over $2 trillion to the deficit through 2027, mostly due to the spending increases.

While legislative changes have worsened the fiscal outlook since June 2017, economic changes have improved them. CBO projects nominal GDP will be 2.4 percent higher in 2027 than what they projected in June. This and other factors result in $1.01 trillion less in deficits. About 0.7 of the 2.4 percent increase and $400 billion of the $1.01 trillion of feedback is the result of the 2017 tax bill.

Other economic revisions, on net, have resulted in additional $570 billion more in revenue and $130 billion less in primary spending, offset in part by $80 billion more in interest payments.

Technical changes have also improved CBO’s fiscal outlook: deficits are $57 billion lower due to technical changes – though the small size of this net improvement is largely due to the $434 billion additional cost CBO estimates for the 2017 tax bill. Other technical changes reduce projected deficits by about $490 billion.

Most significantly, CBO estimates Medicare and Medicaid will spend almost $320 billion less based on the latest data. They also believe agencies will spend appropriated funds more slowly, resulting in $125 billion of lower discretionary spending. In addition, CBO projects almost $50 billion of lower interest spending due to greater issuance of short-term Treasury securities.

Economic Projections

CBO’s budget baseline is built on a new set of economic projections, updated for recent economic data and the effects of the 2017 tax law and other legislation. CBO projects strong near-term economic growth but modest long-term growth.

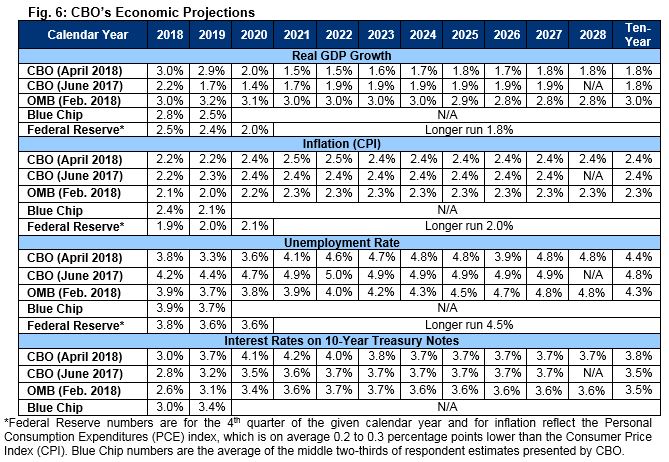

Real GDP is projected to expand by 3.0 percent this calendar year and by 2.9 percent in the 2019 calendar year, compared to the June 2017 projections of 2.2 and 1.7 percent, respectively.

This rapid near-term growth is driven in part, CBO believes, by a strong recovery, allowing the economy to perform in excess of its long-term potential. In 2019, for example, CBO projects GDP will be a percentage point higher than potential GDP.

CBO believes recent legislation has and will help to provide this boost above potential and to increase potential output. Most significantly, CBO believes the 2017 tax bill will boost growth by about 0.3 percentage points per year over the next three years and ultimately lead to a 1 percent increase in GDP by 2022.

CBO also believes the tax law will have a declining effect over time as it adds to the debt and parts of the law expire or emerge. Between 2023 and 2028, CBO believes the law will slow the rate of GDP growth, leaving total GDP in 2028 about 0.5 percent higher than it otherwise would have been (down from 1 percent in 2022). Other legislation estimated to increase output in the short term would dampen it over the longer term, notably due to larger deficits that would reduce the resources available for private investment.

As a result of this and other effects, CBO estimates real GDP growth of 1.5 to 1.8 percent each year after 2020, with an annual average of 1.8 percent over the 2018-2028 period. This is very similar to the average growth rate projected in June 2017.

Notably, CBO’s projected average growth rate is significantly lower than the roughly 3 percent assumed in the President’s FY 2019 budget. Such rapid levels of growth are far below what others – including the Federal Reserve – have projected; and they are highly unlikely to occur based on available economic evidence. The fact that 3 percent growth could be sustained for two years does not suggest it could be continued indefinitely over the long term.

As the economy expands and deficits grow in the near term, CBO also expects interest rates to rise. They estimate the interest rate on three-month Treasury bills will increase from 0.9 percent in 2017 to 3.8 percent by 2021, and the ten-year bond rate will rise from 2.3 percent to 4.2 percent over that period. This represents a significant increase over prior projections – 1.0 percentage points for the three-month bond and 0.6 percentage points for the ten-year bond. However, by 2027 CBO projects interest rates to stabilize at 2.7 percent and 3.7 percent, respectively, which is similar to its estimates last June.

CBO has also revised down its near-term projections for the unemployment rate. It now projects unemployment to average 3.8 percent in 2018 and 3.3 percent in 2019, compared to 4.2 percent and 4.4 percent projected in its June 2017 outlook, before drifting up to the estimated natural rate of unemployment of 4.6 percent by 2022.

Conclusion

CBO’s latest budget projections confirm what we and others have warned for over a year: recent legislation took a dismal fiscal situation and made it much more dire.

Under CBO’s baseline projections, the deficit will approach $1 trillion next year and exceed that mark every year after. Under CBO’s Alternative Fiscal Scenario, $2 trillion deficits will emerge in just a decade.

The combination of fiscally irresponsible tax cuts and spending hikes, population aging, growing health costs, and rising interest rates will drive the national debt up to 96 percent of GDP under current law and 105 percent under the Alternative Fiscal Scenario. Under either scenario, debt would ultimately well exceed the prior record set just after World War II.

Lawmakers need to reverse course sooner rather than later. The problem will only become more difficult to solve the longer we wait to put our fiscal house in order, and continuing to extend current policies without offsets could do far more damage. Instead, policymakers should enact reasonable and responsible discretionary spending caps, fix the recent tax bill to stem revenue losses, reform our nation’s largest entitlement programs, and enact other tax and spending changes as necessary to put the country on sound fiscal footing.