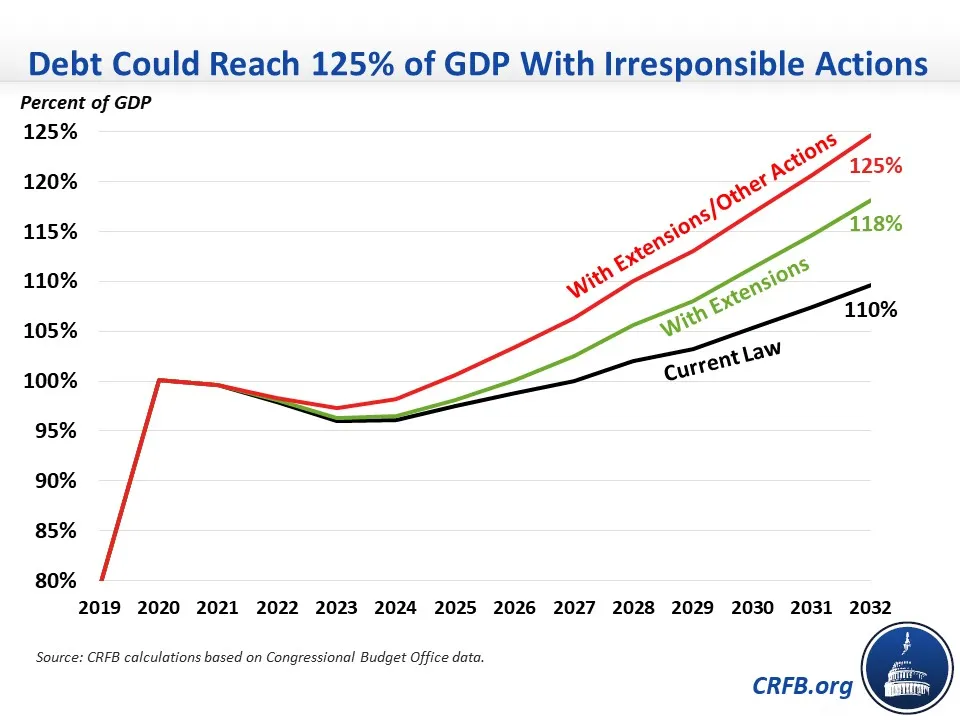

Debt Could Reach 125% of GDP With Irresponsible Actions

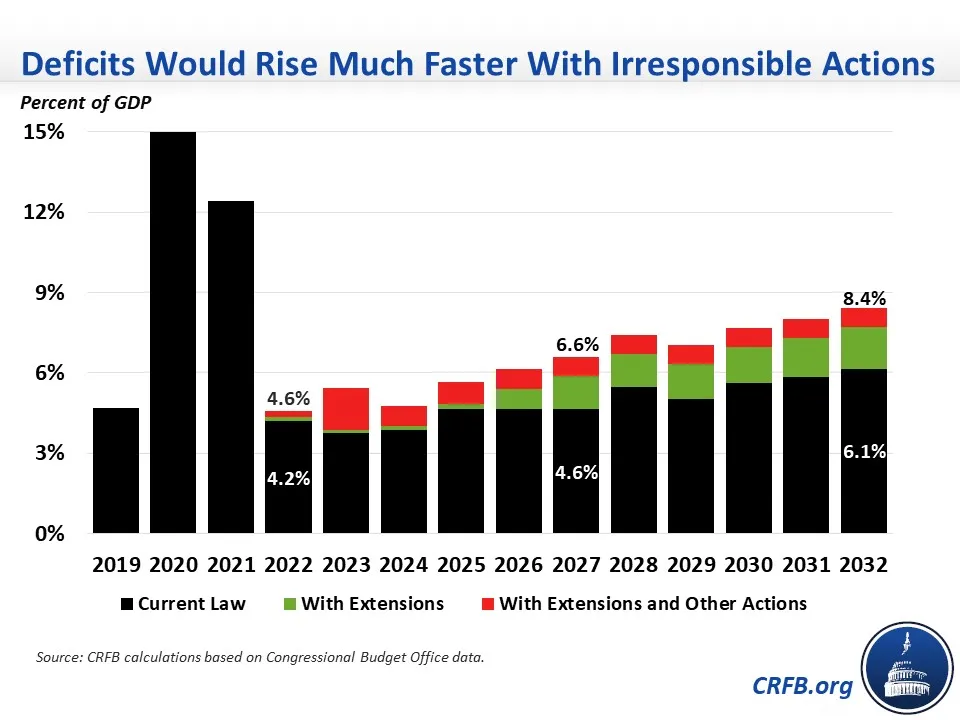

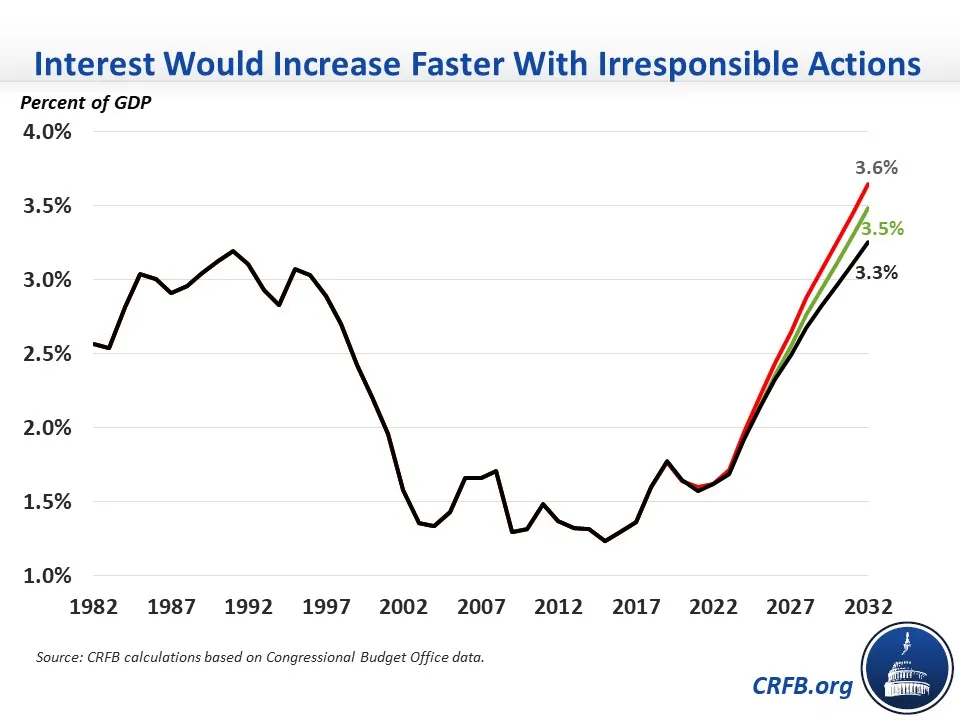

The Congressional Budget Office's (CBO) new budget projections find that debt will reach a record 110 percent of Gross Domestic Product (GDP) ($40.2 trillion) by the end of Fiscal Year (FY) 2032, while the deficit will reach 6.1 percent of GDP ($2.3 trillion) and interest costs will total a record 3.3 percent of GDP ($1.2 trillion). These current law projections may prove optimistic, however, since they assume policymakers will allow a number of temporary policies to expire, only grow discretionary spending with inflation, and won't pass any new deficit-financed legislation. In this analysis, we outline two alternative scenarios that may prove more realistic. We find deficits in 2032 could total $2.8 to $3.1 trillion, while debt could reach 118 to 125 percent of GDP and interest payments could grow to as high as $1.3 trillion, which would be a record 3.6 percent of GDP.

| Metric | 2032 Deficit | 2032 Debt | 2032 Interest |

|---|---|---|---|

| Dollars | |||

| Current Law | $2.3 trillion | $40.2 trillion | $1.2 trillion |

| With Extensions | $2.8 trillion | $43.3 trillion | $1.3 trillion |

| With Extensions and Other Actions | $3.1 trillion | $45.7 trillion | $1.3 trillion |

| Percent of GDP | |||

| Current Law | 6.1% | 110% | 3.3% |

| With Extensions | 7.7% | 118% | 3.5% |

| With Extensions and Other Actions | 8.4% | 125% | 3.6% |

Source: Committee for a Responsible Federal Budget calculations based on Congressional Budget Office data.

CBO's baseline budget projections reflect current law, meaning they, appropriately, do not include the effects of any future legislation or administrative actions, even for temporary policies that have been routinely extended. With so many temporary policies likely to be extended to at least some degree and several pieces of deficit-increasing legislation being actively considered, CBO's current law projections almost certainly reflect an overly optimistic policy environment.

In particular, CBO's current law baseline assumes the individual tax cuts in the Tax Cuts and Jobs Act (TCJA) expire at the end of calendar year 2025 and future discretionary spending grows with inflation, despite new national security challenges, immense pressure to boost both the defense- and non-defense sides of the budget, and no discretionary spending caps to constrain appropriations levels. Because of when the baseline was constructed, it also doesn't incorporate several policies enacted just before its publication, including $41 billion of aid to Ukraine and several administrative changes related to student loans and health care spending.1 On the other hand, it extrapolates hundreds of billions of dollars of temporary funding in the bipartisan Infrastructure Investment and Jobs Act (IIJA) that lawmakers would have to, but don't intend to, appropriate in future legislation.

If we instead assume that the TCJA tax cuts are extended permanently and discretionary spending grows with GDP along with the adjustments mentioned above, deficits through FY 2032 would be $3.1 trillion higher and debt would reach a record 118 percent of GDP by 2032.

On top of this, policymakers may undertake several other costly fiscal actions. For example, they may continue various "tax extenders" and "health extenders," along with full expensing for equipment, a few trade promotion policies, and the soon-expiring expansion of Affordable Care Act subsidies. In addition, Congress is currently considering a bill to expand veterans' compensation and health coverage for those with toxic exposure, a competition bill with funding for semiconductor production, and a bill providing additional funding for restaurants and other small businesses. They may also consider reinstating immediate R&E expensing instead of a five-year write-off period that started this year and provide further aid for Ukraine and COVID treatment and vaccine funding. At the same time, the Biden Administration may consider extending the student loan repayment pause and broadly canceling some amount of student debt. Finally, lawmakers are likely to continue the practice of using phony CHIMPs (changes in mandatory programs) to enable higher discretionary spending.

Though it is unclear exactly how much many of these provisions will cost,2 a reasonable set of assumptions suggests they could add an additional $2.4 trillion to budget deficits through FY 2032 for a total of $5.5 trillion of costs above current law. This would cause debt to reach a record 125 percent of GDP by 2032.

These same scenarios would also increase deficits. Deficits would average 5.0 percent of GDP over the 2022-2032 period under current law but would average 5.9 percent with extensions and average 6.7 percent with additional actions. The gap would be wider by 2032: deficits would total 6.1 percent of GDP under current law, 7.7 percent with extensions, and 8.4 percent with additional actions.

In addition, this would push interest payments to record levels. Interest payments previously peaked at 3.2 percent of GDP in FY 1991. Even under current law, interest spending will rise significantly from 1.6 percent of GDP in 2022 to a record 3.3 percent in 2032. With extensions, interest would increase further to 3.5 percent by 2032, and with the additional actions, it would reach 3.6 percent. If higher borrowing pushed up interest rates and dampened growth as expected, interest costs would rise even further.

CBO's budget projections show debt rebounding from a short-term decline to reach a record 110 percent of GDP by 2032. However, debt could rise much higher -- up to 125 percent of GDP under our estimates -- if policymakers extend several costly temporary policies and take on several other deficit-increasing policies in the near term. Given our bleak fiscal situation, we can't afford more irresponsible actions.

| Policies Assumed in Budget Scenarios | 2022-2032 Cost |

|---|---|

| Current Law Deficits | $16.8 trillion |

| Incorporate already-enacted policies | $150 billion |

| Remove extrapolated IIJA funding | -$840 billion |

| Extend TCJA individual tax cuts | $2,165 billion |

| Grow discretionary spending with GDP | $1,350 billion |

| Interest | $300 billion |

| Subtotal, Extensions | $3.1 trillion |

| Extend bonus depreciation and tax extenders | $420 billion |

| Extend ACA subsidies and health extenders | $300 billion |

| Reinstate R&E expensing and remove other TCJA tax rule tightening | $280 billion |

| Enact bipartisan veterans toxic exposure bill | $385 billion |

| Enact competition bill | $70 billion |

| Provide further COVID funding and extend public health emergency | $250 billion |

| Provide more restaurant funding and Ukraine aid | $100 billion |

| Enact partial student debt cancellation | $250 billion |

| Adjust baseline to account for CHIMPs beyond FY 2022 | $160 billion |

| Interest | $200 billion |

| Subtotal, Other Actions | $2.4 trillion |

| Total, Extensions and Other Actions | $5.5 trillion |

| Total Deficits | $22.4 trillion |

Source: Committee for a Responsible Federal Budget and Congressional Budget Office. Numbers are rough and may not add up due to rounding.

1 Specifically, this refers to extending the student loan repayment pause from the end of May until the end of August, making changes related to income-driven repayment plans, fixing the "family glitch," and imposing a new rule on prescription drug rebates. None of the costs of the first three policies and only half of the rebate rule are reflected in CBO's baseline.

2 For example, there is no estimate for the bipartisan veterans' toxic exposure bill, so we assume the cost of the House version.