CBO: Debt Remains Unsustainable With r < g

The national debt is rising at an unsustainable pace. A factor that helps is interest rates currently being lower than the economic growth rate (r<g). This means that if revenue covers primary spending, debt should fall as a share of Gross Domestic Product (GDP), and the United States could sustainably run small primary deficits. However, as we explained in a recent Q&A and the Congressional Budget Office (CBO) recently affirmed, debt in the United States remains unsustainable despite low interest rates.

It's true that debt is more sustainable when the interest rate is below the growth rate (r<g); economists such as Olivier Blanchard have pointed out that when r<g, a country can effectively grow its way out of its current debt load. Even though nominal debt will grow as a result of interest payments, the economy will grow faster, and debt-to-GDP will shrink.

Unfortunately, the United States continues to borrow more year after year, running large and increasing primary deficits that make it virtually impossible to grow its way out of the problem.

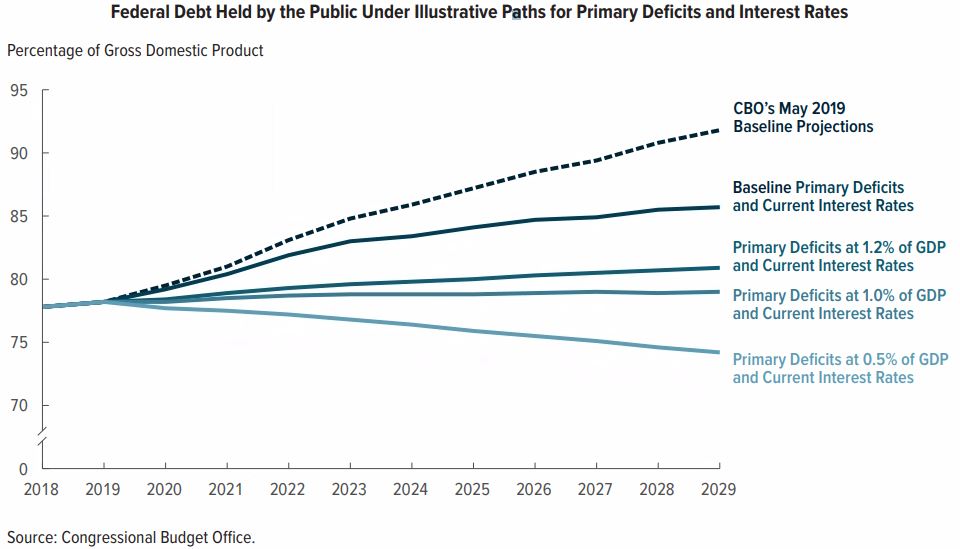

Under current law, CBO projects debt will rise from 78 percent of GDP this year to 92 percent by 2029 and continuously grow thereafter. But even if interest rates remain at their early 2019 levels – rather than rising as CBO projects – debt will still rise faster than the economy, reaching 86 percent of GDP by 2029. In fact, according to CBO, even "if the interest rate on federal debt fell by one half of one percentage point and remained at that low rate over the next decade [we would still face] rising debt as a share of GDP."

So what would it take to stabilize the debt with low interest rates? Under current law, CBO estimates stabilizing the debt would require reducing primary deficits from 1.7 percent of GDP on average to 0.4 percent of GDP, the equivalent of $3.4 trillion in spending cuts or tax increases.

If interest rates stay at the low levels experienced in early 2019, primary deficits would still need to be cut from 1.7 percent of GDP to 1.0 percent, the equivalent of $1.8 trillion in spending cuts or tax increases over the next ten years. Putting debt on a clear downward path under this scenario would require reducing primary deficits to about 0.5 percent of GDP, the equivalent of $3.1 trillion of spending cuts or tax increases.

Importantly, these projections are based on current law and don't account for the cost of extending recent spending increases or tax cuts. Under CBO's Alternative Fiscal Scenario, we estimate it would require about $6.9 trillion to stabilize the debt at current levels and $5.3 trillion if interest rates remained at early 2019 levels.

Two other points are worth noting. First, with low interest rates but relatively high debt, the budget is increasingly sensitive to interest rate risk – just a 1 percentage point increase in projected interest rates would cost $1.9 trillion and raise projected debt from 92 percent of GDP in 2029 to 98 percent of GDP.

Secondly, r is not guaranteed to remain below g forever. Indeed, running large deficits and debt tends to push up the interest rate and push down the growth rate. As economist Ernie Tedeschi recently put it, "the more that policymakers exploit an r<g state and deficit-finance changes in fiscal policy, the less likely it will be that the r<g state persists over the medium- to long-term."

Yet even if interest rates do stay low and economic growth continues, CBO's analysis confirms that the debt remains on an unsustainable path and significant deficit reduction would need to be done to keep debt from rising as a share of the economy. As CBO says,

Even interest rates close to those projected in CBO’s baseline along with persistent primary deficits would not preclude debt from declining in relation to the size of the economy, but those primary deficits would have to be significantly smaller than they are projected to be under current law.