Charting a Responsible Path for Discretionary Spending

With the government now fully funded for Fiscal Year (FY) 2019, policymakers must begin the conversation over appropriate funding levels for next year.

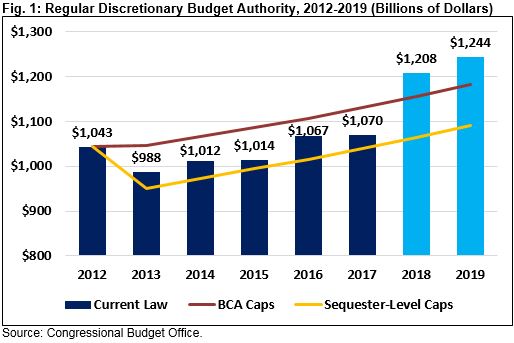

The combination of large spending cap increases for 2018 and 2019 and the return of sequester-level caps in 2020 means that discretionary spending is scheduled to decline by $126 billion (10 percent) between this year and next. Some have called for not only avoiding this cut but also enacting further spending increases.

With annual deficits approaching the trillion-dollar mark and discretionary spending already at elevated levels, it is important to consider any increases against competing priorities, and it would be irresponsible to increase current law spending caps without offsets.

Lawmakers should chart a reasonable and responsible path for discretionary spending through a new multi-year cap regime, paying for increases relative to current law projections with mandatory spending reductions and/or new revenue.

In this analysis, we show:

- The 2018 budget deal enacted a massive increase in discretionary spending. The deal grew spending by 16 percent from 2017 to 2019, blew through the bipartisan caps set in 2011, and added $420 billion to the debt – mostly over two years.

- Today’s spending levels are high by historical standards. In inflation-adjusted dollars, base discretionary spending in 2019 is higher than any other time in history besides 2010. Even as a share of Gross Domestic Product (GDP), discretionary spending is in line with historical averages.

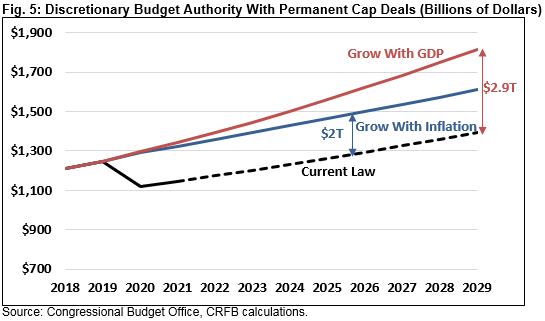

- Extending or expanding recent cap increases could explode the national debt. Simply growing 2019 discretionary spending with inflation would add $2 trillion to deficits through 2029. Growing spending with GDP would cost $2.9 trillion.

- Policymakers should set realistic, reasonable, and responsible discretionary caps. Rather than continuing unprecedented spending hikes without offsets or allowing spending levels to fall abruptly, lawmakers should enact new budget caps over the next decade at levels that are both achievable and affordable. The budgetary cost of these new caps should be offset by addressing the rising cost of mandatory spending programs and lack of revenue to finance federal spending.

The 2018 Budget Deal Dramatically Increased Discretionary Spending

Today’s discretionary spending levels were set under the Bipartisan Budget Act of 2018 (BBA 2018), which increased defense and non-defense spending by about $150 billion per year relative to prior law and by 16 percent relative to 2017 levels.

The law prior to the BBA 2018 had limited defense discretionary spending in FY 2019 to $562 billion and non-defense discretionary to $530 billion. The BBA 2018 increased these spending levels by $85 billion and $67 billion, respectively, for a total of $153 billion (0.7 percent of GDP).

This increase was more than either side had asked for and was a huge break in precedent. Since 2012, discretionary spending levels have been set based on the Budget Control Act (BCA) of 2011, a bipartisan agreement that established discretionary spending caps designed to keep defense and non-defense spending in check.

The BCA put in place caps that both parties viewed as reasonable then reduced those caps by about $90 billion per year under sequestration, which went into effect after the failure of the Joint Select Committee on Deficit Reduction. Lawmakers had always set caps somewhere between the BCA’s pre-sequester levels and sequester levels and have generally offset the cost of any increase.

Rather than enacting partial sequester relief as had been done in the past, the BBA 2018 not only reversed the full $90 billion in sequester savings but also blew through the pre-sequester level caps, which both parties supported, spending an extra $62 billion in 2019 alone. In another troubling break in precedent, this increase – unlike past cap increases – was not offset with mandatory spending cuts or revenue increases (though some past offsets were gimmicks).

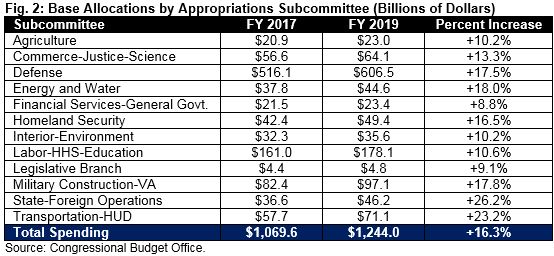

This cap increase has resulted in massive growth in appropriations. Between 2017 and 2019, appropriations increased 16 percent, from $1.070 trillion to $1.244 trillion. Defense spending grew 17 percent, while non-defense grew 15 percent. Some areas have enjoyed even faster growth – for example, Transportation and Housing and Urban Development (HUD) funding grew 23 percent.

No other part of government outside of interest has grown as fast as discretionary spending over the past two years; even health care spending only grew 8 percent. Only a few times in modern history has discretionary spending grown this quickly.

Current Discretionary Spending Levels Are High

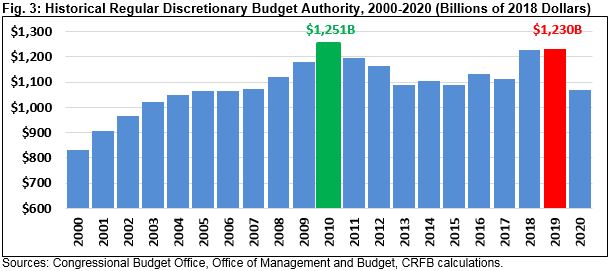

Not only did the BBA 2018 enact a massive increase in discretionary spending, it also set spending at historically high levels. While defenders of the BBA 2018 have argued discretionary spending remains below its 2010 level in inflation-adjusted terms, this claim is misleading.

This year, base discretionary spending is slated to be larger in inflation-adjusted terms than any year since the modern budget process began except for 2010. Non-defense discretionary spending this year is the second highest since 1976, while regular defense spending is the fourth highest.

FY 2010 represented both a high water mark for discretionary spending and an anomaly, driven in part by a new majority, stimulus enacted through the appropriations process, and decennial census funding. Spending that year was so high that both parties proposed reductions.

|

Box 1: The Appropriate Measure for Discretionary Spending Levels Over Time An important factor in determining how high discretionary spending is by historical standards is what measure to use for the comparison. There are several possible measures, including nominal dollars, inflation-adjusted dollars, inflation- and population-adjusted dollars, and percent of GDP. Nominal dollars is the easiest measure since it is readily available, easily understandable, and requires no adjustments. However, nominal dollars is a poor comparative measure since prices for the same goods and services throughout the economy change over time. Using inflation-adjusted dollars (or “real” dollars) corrects for the obvious flaw in the nominal dollar measure by adjusting for changes that occur in economy-wide prices. Indeed, comparing real dollars is probably the best way to measure actual differences in spending levels over time. However, spending levels do not always conform to the level of government services since they may not fully account for changes in the cost of providing specific services or changes in the number of people eligible for those services. Adjusting spending for inflation and population growth can, in some cases, offer a better measure of changes in per-person services. However, many government purchases, subsidies, and programs have little relation to the size of the population. Additionally, adjusting for population growth does nothing to address changes in the composition of the population or the share of the population covered by specific programs. Using percent of GDP effectively accounts for rising population, input prices, and a variety of other factors. This is probably the best measure to show what share of the nation’s resources are going toward discretionary spending over time. However, using percent of GDP masks the reality that many aspects of government spending are becoming more generous by offering more or better services over time. While it certainly makes sense to grow some parts of the budget with GDP to maintain services, a larger economy clearly does not require a proportional increase in all other parts of the defense and non-defense budgets. Using percent of GDP can also mask the growth of real resources being expended by the government. It is important to note that public needs and wants may change over time, both on the defense and non-defense side of the budget. However, comparisons of spending levels over time should not account for changes in needed or desired public activities. If the public requires or demands more government services, policymakers must make the case for meeting those demands. |

Even with these considerations, spending this year is within 1 percent of 2010 inflation-adjusted levels when adjusted for emergency spending, one-time census funding, and phony CHIMPs. Real discretionary spending is 23 percent higher than the average over the past three decades.

To be fair, it might not make sense to compare all discretionary spending using inflation-adjusted dollars. While this certainly provides a useful way to measure many types of government spending, some inputs and programs might be better measured using inflation and population, as a share of the economy, or some other index (see Box 1 for a broader discussion).

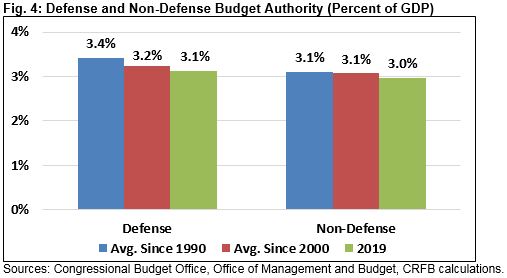

Even comparing the entire discretionary budget using shares of GDP – the most generous measure – current spending levels do not suggest an austere budget. Total base discretionary spending this year will total nearly 6 percent of GDP, 3.1 percent for defense and 3.0 percent for non-defense. These levels are relatively similar to historical averages in recent decades.

Extending the Current Caps Would Be Very Expensive

While the BBA 2018 raised the discretionary spending caps by $143 billion in 2018 and $153 billion in 2019, it made no adjustments in 2020 and beyond. Extending current spending levels into the future would be extremely expensive.

For example, extending current spending levels with inflation would cost $170 billion in 2020. Continuing inflation adjustments over the next decade would cost $2 trillion through 2029 ($220 billion in 2029 alone). Maintaining current levels as a share of GDP would be even more expensive, costing $175 billion next year, $425 billion in 2029, and $2.9 trillion over the decade.

For perspective, either of these scenarios would cost more than the 2017 tax cuts (assuming they expire as scheduled). Absent offsets, they would increase debt as a share of the economy in 2029 from 93 percent of GDP under current law to between 99 and 102 percent of GDP.

Policymakers may try to avoid recognizing the full cost of this change by only increasing the caps temporarily. One wrench in this strategy is that the current caps end in 2021, and under scoring conventions, the Congressional Budget Office (CBO) assumes that spending will grow with inflation after that. Therefore, an increase in 2021 caps would lead CBO to assume spending increases in 2022 and beyond.

Politicians could identify new budget gimmicks or workarounds to make these costs seem lower – for example, setting a sequester-level cap for 2022. However, manipulating budget scoring rules would do nothing to avoid the massive fiscal impact of extending current discretionary levels without paying for the cost of doing so.

Policymakers Should Enact Responsible Caps Going Forward

While extending current spending caps would be expensive, maintaining current law would mean a 10-percent ($126 billion) drop in spending between 2019 and 2020. Moreover, discretionary spending caps would disappear entirely starting in 2022, allowing for higher spending without lawmakers having to acknowledge the cost.

Rather than enacting a massive spending increase without offsets or allowing an abrupt reduction in military spending and domestic government services, policymakers should aim to strike a balance that ensures adequate spending but does not add to the debt. The best approach would be to establish a new set of caps over the next decade to smooth the transition from current levels of spending to ones that policymakers could more easily pay for. Lawmakers should fully offset the cost of these cap adjustments with mandatory spending reductions and/or revenue increases.

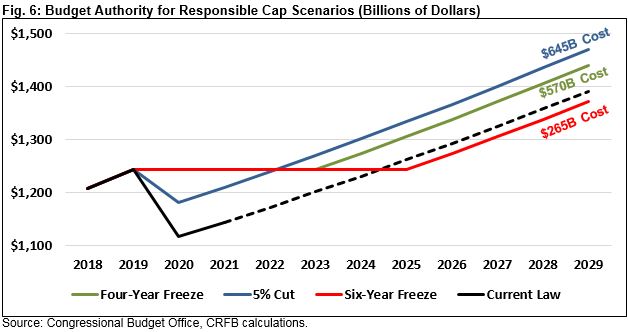

Policymakers could select any number of paths to achieve this goal. For example, a four-year spending freeze would cost $570 billion over the next decade, while a six-year spending freeze would cost $265 billion over ten years – and actually save money in the final few years. A 5-percent reduction in spending between this year and next – which would reverse about one-third of the nominal increase over the past two years – would cost $645 billion over the next decade, leaving spending about $65 billion to $80 billion per year above sequester levels.

While each of these options would set discretionary spending at lower levels than today, they would also all cost more than current law. Lawmakers should pay for this cost by reducing low-priority spending, slowing the growth of health care costs, cutting tax breaks and loopholes, and/or raising other revenue and receipts. We’ve identified a number of options to generate these savings, including many with bipartisan support.

Conclusion

The Bipartisan Budget Act of 2018 increased discretionary spending dramatically to high levels by historical standards, with very few offsets. This increase – along with recent tax cuts – has been a significant driver of the near-term growth of deficits since 2017.

Since the BBA’s cap increases were only for two years, they also created a cliff that lawmakers will have to resolve this year. Yet simply extending the caps would be very costly and add substantially to an already rising national debt.

Any discretionary spending deal should extend the caps beyond 2021, set affordable and achievable limits on discretionary spending, and, most importantly, offset the cost of spending increases relative to current law. This will prevent lawmakers from digging a deeper hole than they already did with the BBA 2018.

Lawmakers should then move on to fixing the problems that truly drive our long-term debt situation: rising health and retirement costs and lack of revenue to fully finance them.

What's Next

-

Image

-

Image

-

Image