CBO’s Analysis of the President’s FY 2019 Budget

The Congressional Budget Office (CBO) released its estimate of the President’s Fiscal Year (FY) 2019 budget using its own assumptions to evaluate the budget’s policies. While the President’s budget claims to put the debt on a downward path as a share of the economy, CBO’s analysis suggests that these claims are based on a number of unrealistic assumptions and unspecified savings.

Using more realistic economic assumptions and independently evaluating the President’s policies, CBO finds that debt will continue to rise under the President’s budget, though at a slower rate than under current law.

Major findings from CBO’s estimates include:

- The President’s budget would reduce deficits by $2.9 trillion below current law over ten years, including $1.8 trillion of policy savings.

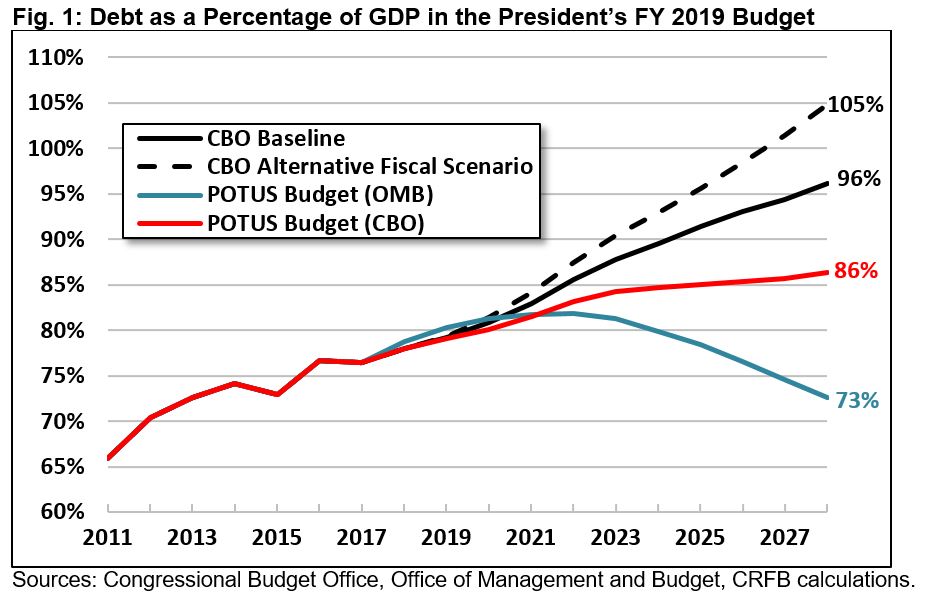

- Debt under the President’s budget would rise from 78 percent of GDP at the end of this year to 86 percent by 2028 rather than falling to 73 percent of GDP as the White House estimates.

- Trillion-dollar deficits would emerge in 2022 and again in 2028 under CBO’s estimate of the President’s budget. Deficits would total $9.5 trillion over the next decade, $2.3 trillion higher than the Administration estimates.

- The President’s budget would reduce revenue by $615 billion and spending by $3.5 trillion relative to current law, with the largest spending cuts coming from health care and non-defense discretionary spending – including roughly $1 trillion of unspecified savings.

- The vast majority of the difference in debt estimates between CBO and the President is due to different economic assumptions. The Office of Management and Budget (OMB) assumes economic growth will average 3 percent over the next decade, whereas CBO estimates 1.8 percent. CBO’s estimates are in line with nearly all public and private estimates, whereas OMB’s are unlikely to materialize.

The President deserves credit for putting forward substantial deficit reduction in his budget, including a number of thoughtful policies that Congress should adopt. However, many of the President’s proposals lack specificity, and too much of the President’s budget is based on extremely rosy assumptions.

Rather than counting on rapid economic growth and unspecified savings, policymakers need a specific and realistic plan to get discretionary spending under control, reform various tax breaks and spending programs, raise revenue, and put Social Security and Medicare on a sustainable long-term path.

Spending, Revenue, Deficits, and Debt under the President’s Budget

CBO estimates that debt would continue to rise over the next ten years under the President’s budget. It projects that debt would reach a new post-World War II-era record of 78 percent of GDP by the end of this year (as it will under current law), rise rapidly to 84 percent by 2023, and continue to rise slowly to 86 percent by 2028.

These debt levels are much higher than OMB’s projection that debt would decline to 73 percent of GDP by 2028, but they are lower than current law, under which CBO estimates debt will reach 96 percent of GDP by 2028. Debt under the President’s budget is also much lower than CBO’s Alternative Fiscal Scenario (AFS), which projects debt of 105 percent of GDP.

CBO’s estimates of the President’s budget include roughly $1 trillion of unspecified spending cuts from applying a “two-penny plan” to future non-defense discretionary spending. Without those savings, debt would rise to roughly 90 percent of GDP by 2028.

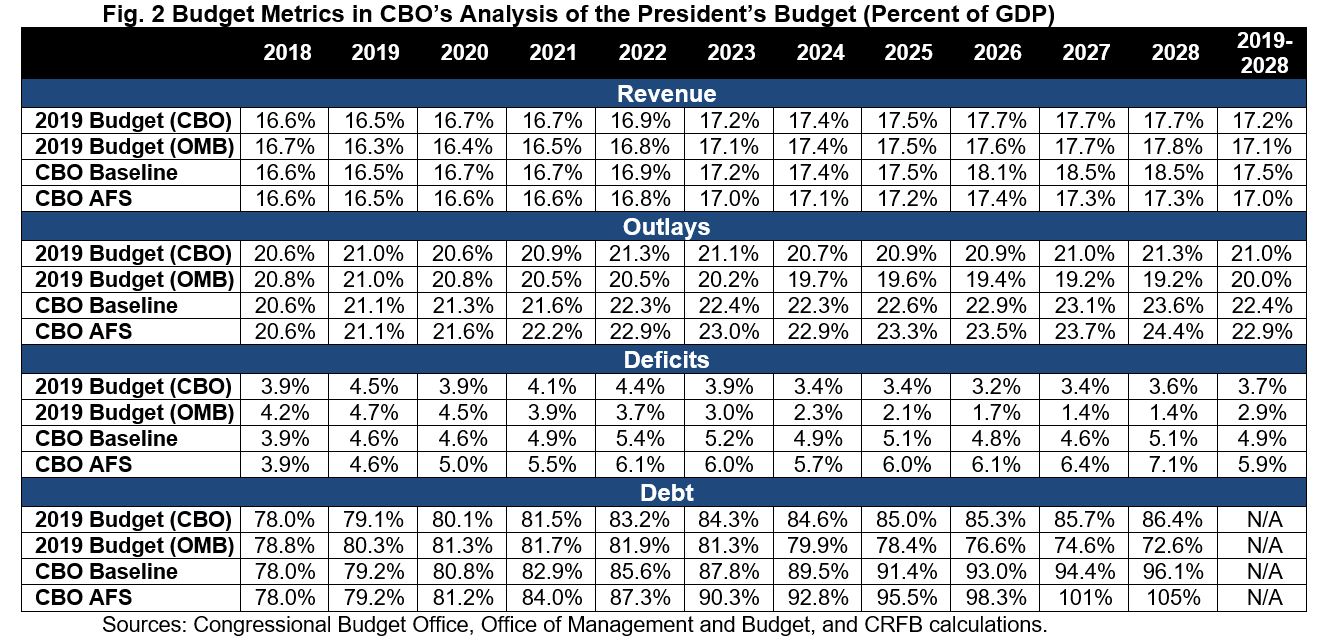

Even counting these unspecified cuts, CBO finds that deficits would total $9.5 trillion (3.7 percent of GDP) from 2019 through 2028, $2.9 trillion less than current law but $2.3 trillion higher than OMB projects.

By 2028, CBO projects the deficit would total $1.1 trillion, or 3.6 percent of GDP. This is a significant improvement relative to the $1.5 trillion (5.1 percent of GDP) deficit projected under current law and the $2.1 trillion (7.1 percent of GDP) deficit under the AFS, but it is much higher than the Administration’s estimate of a $445 billion (1.4 percent of GDP) deficit in 2028.

Deficits in the President’s budget are driven by a sustained (but not growing) wedge between spending and revenue. Spending under the budget would remain relatively stable as a share of GDP at about 21 percent (21.3 percent in 2028) – slightly above the historical average of 20.3 percent. Revenue, meanwhile, would rise slowly from 16.6 percent of GDP in 2018 to 17.7 percent by 2028, roughly in line with the historical average of 17.4 percent.

As a result of cuts in the President’s budget, overall spending growth would be much slower than current law, where CBO projects outlays of 23.6 percent of GDP by 2028. Revenue in 2028 would be below the current law projected level of 18.5 percent of GDP, mainly because the budget extends the expiring provisions of the 2017 tax law.

Policy Changes in the President’s Budget

Although the President’s budget falls short of putting the debt on a downward path, it does incorporate significant deficit reduction, including a number of thoughtful spending cuts and reforms. On the other hand, it contains a large amount of unspecified savings.

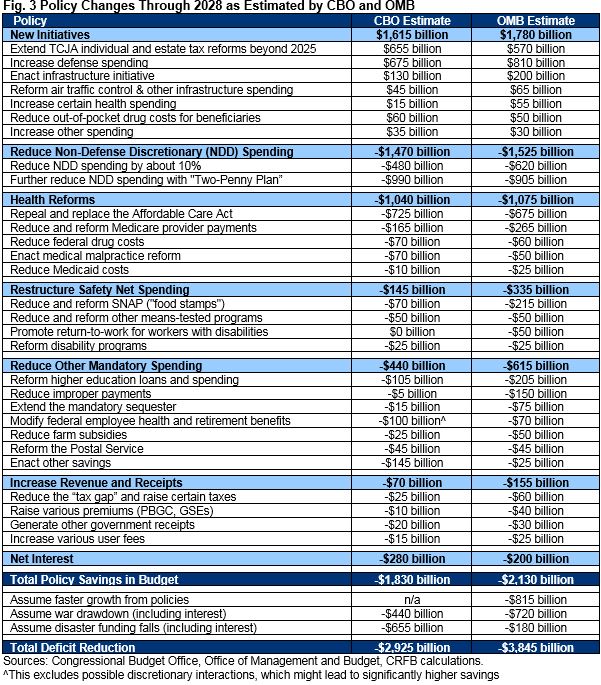

CBO estimates the budget would reduce deficits by $2.9 trillion relative to current law, of which $1.8 trillion represents policy savings (the remainder comes from a war drawdown and removal of excessive disaster spending assumptions). That $1.8 trillion in savings is similar though somewhat smaller than OMB’s estimate of $2.1 trillion – though OMB also assumes $815 billion of savings from faster economic growth that is unlikely to occur.

That net reduction is the result of $1.6 trillion in new spending and tax cuts; $3.2 trillion in spending cuts, receipts and reforms; and $280 billion of interest savings.

The $1.6 trillion of gross costs comes mainly from extending many expiring provisions in the 2017 tax law and from increasing defense spending.

Of the $3.2 trillion in savings, almost $1 trillion are from unspecified future non-defense discretionary (NDD) reductions. After proposing specific reductions to NDD spending in 2019, the budget assumes further nominal cuts of 2 percent per year through its “two-penny plan”.

The remaining savings come from the initial NDD cuts, repealing and replacing the Affordable Care Act, limiting Medicaid growth, reducing Medicare costs, reducing and reforming Supplemental Nutrition Assistance Program (SNAP) benefits, reforming student loan subsidies, reducing the generosity of federal retirement benefits, and a variety of other proposals. Details of the policies are available here.

Among deficit reduction policies – including unspecified NDD cuts – CBO’s savings estimates are somewhat lower than OMB’s estimates ($1.8 trillion versus $2.1 trillion). The biggest differences between CBO and OMB’s estimates come from CBO disregarding unspecified or unachievable savings from reducing improper payments, transforming SNAP benefits into a USDA “food box,” reforming financial regulations, and piloting remain-at-work and return-to-work initiatives for Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI).

OMB scored these policies as saving a combined $350 billion in OMB’s estimates. However, CBO scores them without savings due to lack of detail and a likelihood that such levels of savings could not be achieved.1

In addition, CBO estimates lower savings from the student loan changes ($100 billion), Medicare provider payment changes ($100 billion), and farm subsidy changes ($25 billion). On the other hand, it finds $50 billion greater savings from the budget’s repeal and replacement of the Affordable Care Act, at least $30 billion more from federal employee retirement and health changes, and $20 billion greater savings from medical malpractice reform.

CBO also did not count the $815 billion of savings that OMB estimated for the implausibly large boost to economic growth it anticipated from the budget’s policies. However, it is possible the budget would produce some improvements in economic growth, which could modestly reduce projected deficit and debt levels.

Differences Between CBO and OMB Estimates

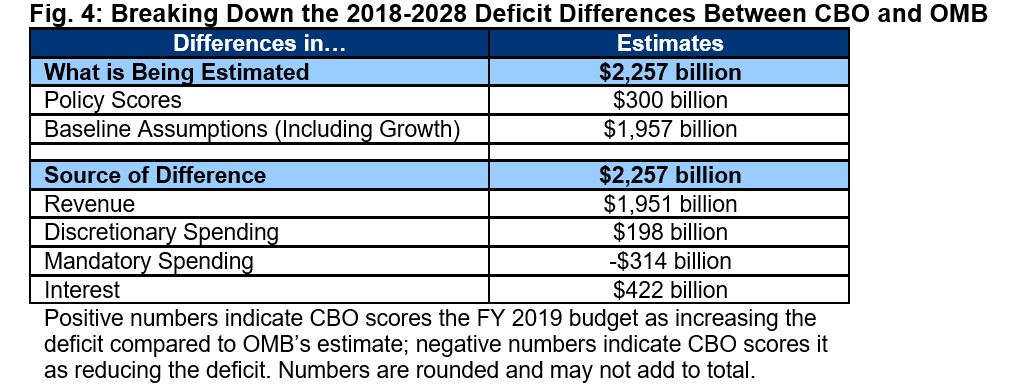

CBO’s estimates paint a far less rosy picture than those from OMB. In total, CBO estimates $9.5 trillion of deficits over the next decade under the President’s budget, $2.3 trillion higher than OMB’s estimate. CBO finds debt would reach 86 percent of GDP in 2028, nearly 14 percentage points of GDP higher than OMB estimates.

Much of the difference arises from different economic assumptions used by each agency. OMB projects that real GDP will grow by an average of 3.0 percent annually from 2018 to 2028, while CBO projects a more realistic 1.8 percent. This difference is the main driver of the $1.95 trillion difference in revenue under CBO’s estimates,2 which itself explains most of the $2.26 trillion difference in total projected deficits.

Of the remaining difference, $198 billion is the result of higher projected discretionary spending and $422 billion is due to higher interest spending. Partially offsetting this is $314 billion less in mandatory spending through 2028.

OMB’s higher growth estimates also mean that the same dollar amount of debt appears lower as a share of GDP. For example, if OMB’s dollar amount of debt was divided by CBO’s GDP, debt would be 79 percent of GDP instead of 73 percent in 2028.

Another way to understand the difference between CBO and OMB’s estimates is how much is attributable to estimates of policy changes versus how much is attributable to differences in baseline projections prior to policy action. By our estimate, $2 trillion of the difference in 2018-2028 deficits is due to baseline projections including growth, while $300 billion is due to differences in policy estimates.

Conclusion

CBO’s analysis shows that with realistic economic assumptions, even the President’s aggressive package of spending cuts would not be enough to prevent the debt from rising as a share of the economy nor to avoid the return of trillion-dollar deficits.

Unfortunately, the recent tax cuts and spending bills have made an unsustainable fiscal situation even harder to bring under control, especially without major changes to Social Security, Medicare, defense, and the tax code.

To the President’s credit, his budget would result in a significant fiscal improvement relative to our current path, and his budget includes a number of thoughtful and worthwhile cuts and reforms. However, the budget relies on huge cuts to non-discretionary programs that run counter to the large spending increases the President signed into law earlier this year. In addition, these changes simply are not sufficient when using realistic economic growth assumptions.

Policymakers should take seriously many of the proposed spending cuts in the President’s budget. But they should combine them with reasonable and responsible discretionary spending caps, improvements to the tax law, significant reforms to slow the rapid growth of Social Security and Medicare, new tax revenue, spending cuts, and a comprehensive economic

1 Properly designed SSDI and SSI reforms to support and encourage work can ultimately lead to savings, but substantial savings will take a number of years to materialize and will not begin to accrue until pilot programs are implemented broadly. CRFB’s McCrery-Pomeroy SSDI Solutions Initiative has developed and continues to develop potential reforms.

2 According to CBO, “JCT and CBO’s estimates of revenues differ from the Administration’s largely because of differences in economic forecasts.”