Analysis of CBO’s Budget and Economic Outlook (January 2020)

Today, the Congressional Budget Office (CBO) released its January 2020 Budget and Economic Outlook, projecting the return of trillion-dollar deficits as well as high and rising debt and deficits over the next decade and beyond. CBO’s report shows:

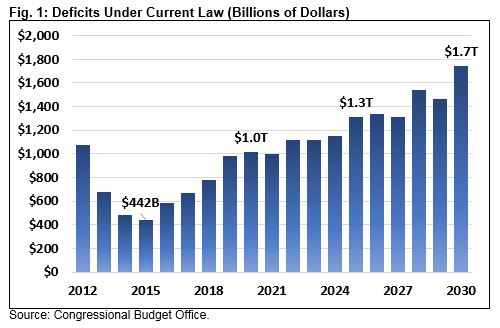

- The budget deficit will total $1.02 trillion (4.6 percent of GDP) this year – the first trillion-dollar deficit in history not caused by the Great Recession. Deficits will further rise under current law to $1.7 trillion (5.4 percent of GDP) by 2030.

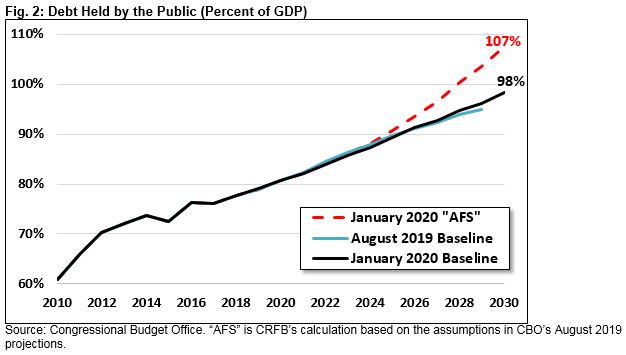

- Under current law, debt held by the public will rise from a post-war record 80 percent of GDP today to above 98 percent by 2030. That represents a $14.3 trillion increase, from $17.2 trillion today to $31.4 trillion in 2030.

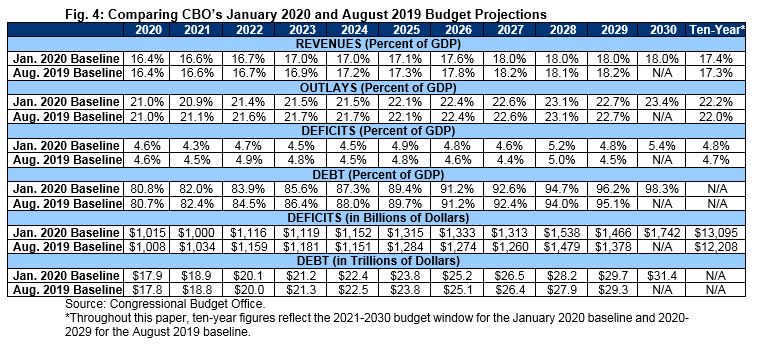

- Deficits are $160 billion higher though 2029 than in CBO’s prior baseline. This is the net effect of roughly $500 billion in new debt from tax cuts in December’s appropriations package, partially offset by economic and technical changes.

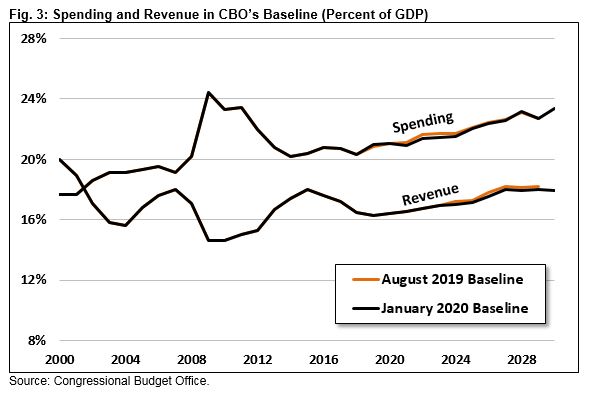

- CBO projects spending to rise from 21.0 percent of GDP this year to 23.4 percent by 2030 and revenue to rise from 16.4 percent of GDP this year to 18.0 percent by 2030. Spending will average nearly two points higher than the 50-year average of 20.4 percent, and revenue will be at its average of 17.4 percent.

- The fiscal situation will continue to deteriorate over the long term. CBO projects budget deficits to average more than 10 percent of GDP in the 2040s and debt to reach 180 percent of GDP by 2050.

- Though CBO did not include an Alternative Fiscal Scenario, we estimate that extending expiring tax cuts and maintaining discretionary spending as a share of GDP would lift debt to 107 percent of GDP by 2030 – an all-time record.

- CBO projects real economic growth of 2.2 percent this year and an average of 1.7 percent in future years. CBO projects unemployment to rise to 4.4 percent, interest rates to rise above 3 percent, and inflation to remain at 2 percent.

CBO’s latest budget projections confirm our country is on an unsustainable fiscal path due to the rising and underfinanced cost of Social Security, health, and interest spending as well as the passage of multiple rounds of unpaid-for tax cuts and spending increases. Lawmakers must stop making the budgetary situation worse and work together to put the country’s fiscal house back in order.

Permanent Trillion-Dollar Deficits Will Emerge

CBO projects the budget deficit will surpass $1 trillion this year, up from $442 billion in 2015 and higher than any time in history outside of the Great Recession and its aftermath. Over the next decade, CBO projects deficits will grow further, reaching $1.3 trillion in 2025 and a record-high $1.7 trillion in 2030. Deficits will total $13.1 trillion over the next decade.

As a share of GDP, the budget deficit this year will total 4.6 percent of GDP – the highest it has been outside of World War II at this point in the economic cycle. By 2030, CBO projects deficits will reach 5.4 percent of GDP – which would be the second-highest deficit outside of World War II and the Great Recession. Deficits will average 4.8 percent of GDP over the next decade.

Over the long term, the situation will get far worse. CBO projects the deficit will reach 8.4 percent of GDP by 2040 and 11.8 percent of GDP by 2050, eclipsing the previous post-war record set in 2009 during the Great Recession.

If lawmakers continue their recent streak of fiscal irresponsibility, deficits could be higher still. Though CBO’s report does not include an Alternative Fiscal Scenario (AFS), we estimate that an AFS-like scenario that extends various expiring tax cuts and grows discretionary spending with the economy would add $2.8 trillion to deficits over the next decade. As result, the budget deficit would total $2.4 trillion, or 7.4 percent of GDP, by 2030.

Debt Will Approach Record Levels

High and rising deficits will continue to drive the national debt upward. CBO projects debt held by the public will rise by $14.3 trillion over the next decade, from $17.2 trillion today to $31.4 trillion by 2030.

As a share of the economy, debt will rise from its post-war record-high of 80 percent of GDP today – nearly twice its historic average of 43 percent – to 89.4 percent of GDP by 2025 and 98.3 percent by 2030. This level of debt would be virtually unprecedented; debt has only been larger as a share of the economy in two years in U.S. history – 1945 and 1946. Debt would continue rising after that, to 180 percent of GDP by 2050 – nearly 75 percentage points higher than its 1946 peak.

Moreover, debt could be significantly worse if lawmakers continue policies enacted in the last several years. Although CBO did not put forward an Alternative Fiscal Scenario, we estimate that using the assumptions it made in August – holding discretionary spending constant as a share of GDP while extending parts of the Tax Cuts and Jobs Act and other expiring tax policies – debt would grow to above $34 trillion by 2030. Debt would reach 107 percent of GDP in 2030, exceeding the previous record of 106 percent set just after World War II.

As we’ve explained before, high debt has adverse and potentially dangerous consequences. Rising debt slows wage and income growth, increases federal interest payments, hinders our ability to respond to the next recession or emergency, places an undue burden on future generations, and heightens the risk of a fiscal crisis.

Spending and Revenue Will Continue to Diverge

Rising debt and deficits are driven by a disconnect between spending and revenue. This year, CBO projects spending to total $4.6 trillion, while revenue will total $3.6 trillion. The gap between the two will grow as spending continues to rise and revenue fails to keep up.

Specifically, CBO projects spending to rise from 21.0 percent of GDP this year to 22.1 percent by 2025 and 23.4 percent by 2030. Meanwhile, revenue is projected to rise slowly from 16.4 percent of GDP this year to 17.1 percent by 2025 and then rise more quickly to 18.0 percent of GDP in 2027 through 2030, as major parts of the 2017 Tax Cuts and Jobs Act expire.

The bulk of the projected spending increase can be explained by rising health, Social Security, and interest costs. Spending in these three areas is expected to rise from 12.0 percent of GDP ($2.7 trillion) in 2020 to 15.6 percent of GDP ($5.0 trillion) in 2030. This spending increase comprises 82 percent of the projected $2.8 trillion increase in nominal spending and 148 percent of spending growth as a share of the economy through 2030.

While not a major source of future spending growth, discretionary spending has played a significant role in spending growth over the past few years. This category of spending increased by 11 percent between 2017 and 2019 and is expected to increase another 5 percent in 2020.

At the same time as discretionary spending has risen, revenue as a share of GDP has fallen – from 18 percent of GDP in 2015 to just 16.4 percent this year. CBO expects revenue to grow going forward but at a much slower rate than spending – and mostly between 2025 and 2027 as various tax cuts are scheduled to expire.

The bulk of projected revenue growth will come from individual income tax receipts. Individual income tax revenue is projected to rise slightly, from 8.1 percent of GDP this year to 8.5 percent of GDP by 2025, and then rise sharply to 9.5 percent of GDP by 2027 due to expiration of the individual income tax cuts in the 2017 Tax Cuts and Jobs Act at the end of (calendar year) 2025.

Also due in part to features of the Tax Cuts and Jobs Act, corporate tax revenue is projected to rise from 1.1 percent of GDP in 2020 (down from 1.5 percent in 2017) to between 1.3 and 1.4 percent starting in 2023. Other sources of revenue – including payroll and excise taxes – will remain relatively steady as a share of the economy through 2030.

Over the next decade, spending will average 22.2 percent of GDP – which is nearly two percentage points higher than its 50-year historical average of 20.4 percent of GDP. Average revenue will be 17.4 percent of GDP in line with its historic average.

Looking into the more distant future, CBO projects spending will be 30.4 percent of GDP in 2050, while revenue will be 18.6 percent. More than the entirety of long-term spending growth will come from Social Security, health care, and interest on the debt, while virtually all revenue growth will come from individual income tax revenue.

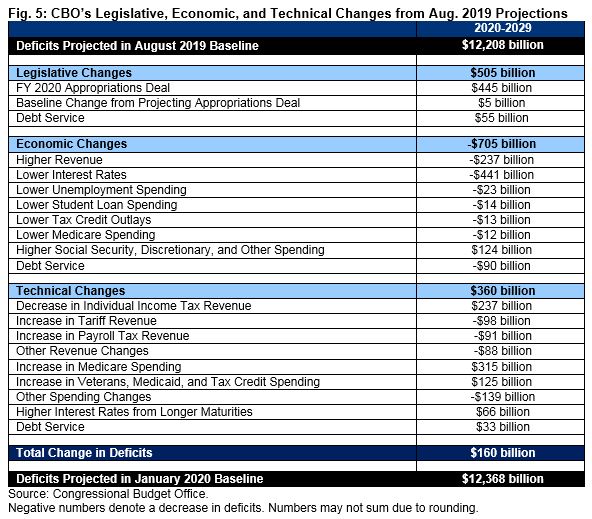

Legislative, Economic, and Technical Changes Worsened the Budget Outlook

CBO’s projections have worsened since its last baseline in August. In total, CBO projects deficits will total $12.4 trillion from 2020 through 2029, a $160 billion increase from its previous estimate of $12.2 trillion. As a result, CBO expects debt to reach 96 percent of GDP in 2029, compared to its prior estimate of 95 percent. Similarly, the deficit will be 4.8 percent of GDP in 2029, 0.3 percentage points higher than the August 2019 projection of 4.5 percent.

The largest contributor to the projected increase is the appropriations package enacted in December, which included a permanent repeal of taxes enacted to finance the Affordable Care Act and the revival of various zombie extenders. That package added $500 billion to deficits through 2029, with interest. Other legislative changes added an additional $5 billion.

Economic and technical changes offset nearly $350 billion of these legislative increases.

On the economic side, CBO projects a net improvement. Higher revenues from stronger growth reduced projected deficits by $237 billion, while lower interest rate projections reduced them by $441 billion. Lower unemployment insurance, student loan, tax credit (Earned Income and Child Tax Credits), and Medicare payments decreased projected deficits by $61 billion. Other spending changes – including higher estimated discretionary outlays and higher Social Security payments – increased projected deficits by $124 billion, largely due to stronger economic growth raising Social Security benefits and employment costs for discretionary programs.

On the technical side, CBO projects a net deterioration. CBO’s latest projections assume a smaller share of income will go to high earners, which means lower individual income tax receipts and higher payroll tax receipts. In total, CBO projects $237 billion less from individual income taxes and $91 billion more from payroll taxes. On top of that, CBO projects $98 billion in additional revenue from tariffs imposed by the Administration and $88 billion from other revenue sources.

At the same time, CBO projects Medicare will spend $315 billion more than previously projected, mostly stemming from higher Medicare Advantage payments that CBO believes will continue permanently. Higher spending on veterans’ benefits, Medicaid spending, tax credit outlays, and appropriations will add another $125 billion to deficits. Lower spending on health care premium tax credits, the Pension Benefit Guaranty Corporation, and other spending will reduce deficits by $139 billion. Finally, Treasury began issuing more longer-term debt, which carries higher interest rates. CBO projects that will add $66 billion to deficits. The resulting increase in primary deficits from technical changes will add $33 billion in higher debt service costs.

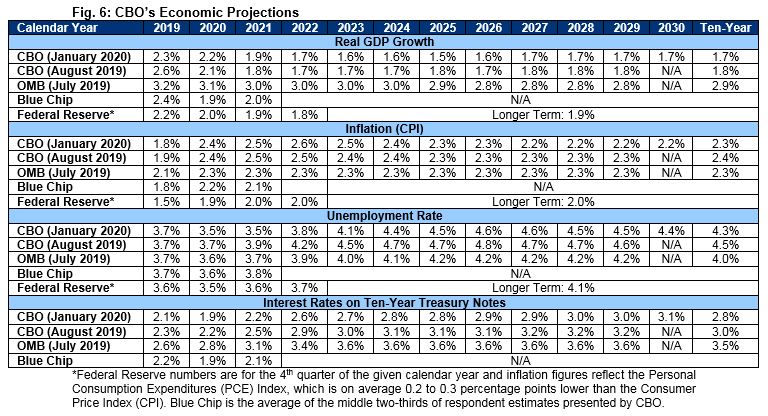

Economic Growth Will Slow

In addition to budget projections, CBO’s baseline includes a set of economic projections that forecast growth in real Gross Domestic Product (GDP), inflation, unemployment, and interest rates over the next ten years, amongst other factors. Importantly, CBO does not try to forecast the business cycle.

Whereas the economy (as defined by GDP) grew by 2.9 percent in 2018 and 2.3 percent in 2019, CBO projects slower growth in the future. Specifically, CBO projects GDP growth of 2.2 percent this year, 1.9 percent next year, and an average of 1.7 percent over the next decade.

Overall, CBO’s projections are in line with projections from the Federal Reserve, Blue Chip, and other forecasters. The Trump Administration’s forecast of nearly 3 percent sustained growth over the next decade is outside the consensus and highly unlikely based on economic evidence.

In terms of inflation, CBO projects Consumer Price Index (CPI) growth of 2.2 to 2.6 percent per year over the next decade. Other chain-weighted measures of economy-wide inflation are expected to rise by about 2 percent per year, in line with the Federal Reserve’s target.

The unemployment rate is projected to decrease from 3.7 percent in 2019 to 3.5 percent this year before rising to 3.8 percent in 2022 and ultimately reaching 4.4 percent by 2030. CBO estimates that the current unemployment rate is below the natural rate that can be sustained and will eventually drift back toward the natural rate.

As deficits grow and the economy expands, CBO expects interest rates to rise modestly. The interest rate on three-month Treasury bills is expected to increase from 1.6 percent this year to 2.3 percent by 2025 and 2.4 percent by 2030. The ten-year bond rate is estimated to rise from 1.9 percent this year to 2.8 percent by 2025 and 3.1 percent by 2030. Interest rates are generally lower in the short term than in CBO’s August 2019 forecast but only slightly lower later in the decade.

Conclusion

CBO’s latest budget projections confirm what we’ve warned about for some time: our country is on an unsustainable fiscal path, and the budget outlook continues to deteriorate. Trillion-dollar budget deficits are the new normal, and debt is projected to grow rapidly as a share of the economy over the next decade and over the long term.

Driving this growth is the disconnect between the rising costs of Social Security, health care, and interest on the debt and the lack of revenue to cover these costs. Instead of taking steps to control or finance this cost growth, policymakers choose to worsen our fiscal outlook by continuously enacting unpaid-for tax cuts and massive spending increases. The recently enacted spending deal added $500 billion to projected debt levels by tacking a number of tax cuts onto ordinary appropriations.

As we’ve explained before, rising debt slows income growth, increases interest payments that crowd out other priorities, places upward pressure on interest rates, weakens our ability to respond to the next recession or emergency, places an undue burden on future generations, and heightens the risk of a fiscal crisis.

The first step toward a sustainable fiscal outlook is to stop making the situation worse. Policymakers must offset the cost of new legislation and any extensions to current policy. To see a menu of available policy options to finance new proposals, visit the Budget Offsets Bank (www.crfb.org/offsets).

Furthermore, lawmakers must secure the Social Security, Medicare, Highway, and other trust funds headed toward insolvency, curb the growth of health care costs, increase revenue, reduce spending, and pursue a pro-growth economic agenda. Without including all of these elements, it will be difficult to address our nation’s budgetary challenges and get our fiscal house in order.