Updating the U.S. Budget Outlook

Note (4/30/2018): This paper was published before CBO's April 2018 baseline, which provides official estimates of the fiscal situation. For the official estimates, read our analysis of CBO's April 2018 baseline here.

The national debt is currently higher than at any time in history outside of World War II and the years immediately after, and it is rising unsustainably. Moreover, recent tax and spending legislation have made a bad situation even worse.

For an Excel of our updated budget projections, click here.

Because of the rapid pace of legislative change, the Congressional Budget Office (CBO) has not had the opportunity to update its projections since June 2017. In this paper, we construct our own rough budget projections based on CBO’s methods.

Our projections show that under current law, trillion-dollar deficits will return permanently by next year and debt will exceed the size of the economy within a decade. Under potentially more realistic policy assumptions, the country will be facing a $2.4 trillion deficit and debt of 113 percent of Gross Domestic Product (GDP) by 2028. These projections show a fiscal situation that is clearly unsustainable.

In this paper, we show:

- Legislation passed since June 2017 will add roughly $2.4 trillion to the baseline debt through 2028; continuing various expiring policies will add another $3.6 trillion to the debt.

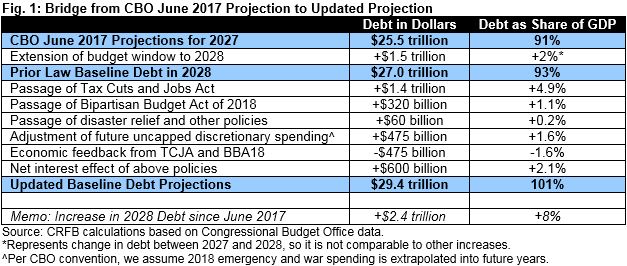

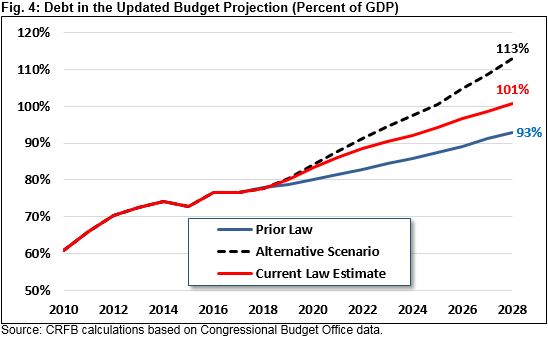

- Under our baseline projection, debt will rise from 76 percent of GDP ($14.7 trillion) at the end of 2017 to 101 percent of GDP ($29.4 trillion) by 2028. Previously, projections suggested debt would reach 93 percent ($27 trillion).

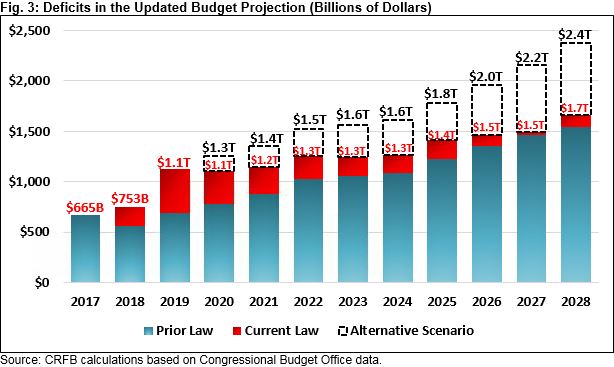

- Our baseline projections also show deficits rising from $665 billion in 2017 to $1.1 trillion by 2019 and $1.7 trillion by 2028. Previous projections showed trillion-dollar deficits returning in 2022 and a $1.5 trillion deficit in 2028. As a percent of GDP, the deficit will rise from 3.5 percent in 2017 to 5.3 percent in 2019 and 5.7 percent by 2028. It was previously expected to reach 3.3 and 5.3 percent of GDP in those years.

- Debt and deficits would be much worse if temporary spending increases and tax cuts are made permanent. Under our alternative scenario, debt will reach 113 percent of GDP ($33 trillion) by 2028, and the deficit will total $2.4 trillion (8.2 percent of GDP) in 2028.

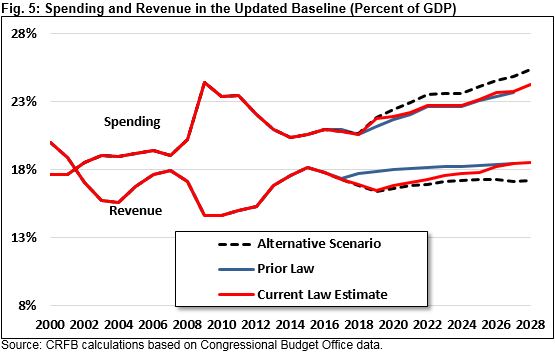

- Spending under our baseline projections will rise from 20.8 percent of GDP in 2017 to 24.3 percent by 2028 (25.3 percent in our alternative scenario), the second highest level in modern history. Revenue will remain between 16 and 18 percent of GDP until the recent tax cuts expire (and beyond that under our alternative scenario), which is unusually low for a healthy economy.

While our specific projections are uncertain, they make clear that the country faces an unsustainable fiscal situation that has significantly deteriorated in the last year.

Constructing Our Updated Projections

Much has happened since June 2017. Our projections begin with CBO’s prior baseline and incorporate the effects of recent legislative and administrative changes – most significantly the Tax Cuts and Jobs Act (TCJA) and the Bipartisan Budget Act of 2018 (BBA18). We also attempted to adjust GDP projections and economic feedback based on new legislation. Importantly, our estimates do not attempt to incorporate other economic or technical changes that are likely to further impact baseline projections.

In June 2017, CBO projected debt would reach $25.5 trillion or 91 percent of GDP by 2027, which suggests debt of about $27 trillion or 93 percent of GDP by 2028. We estimate that legislative and administrative changes since June will increase debt in 2028 by $2.4 trillion or 8 percent of GDP by 2028, for a total of $29.4 trillion or 101 percent of GDP.

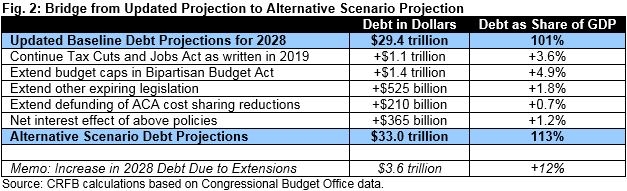

We estimate debt would grow by an additional $3.6 trillion if various expiring policies were extended. Under that alternative scenario, debt would reach $33 trillion and 113 percent of GDP by 2028.

Deficit Projections

Under current law, we expect the permanent return of trillion-dollar deficits next year. Specifically, we expect deficits to rise from last year’s $665 billion to more than $1.1 trillion in fiscal year 2019 and to $1.7 trillion by 2028. As a share of GDP, we project the deficit to increase from 3.5 percent of GDP in 2017 to 5.3 percent in 2019 and to 5.7 percent by 2028.

These deficits are significantly worse than those in CBO’s June projections, which saw trillion-dollar deficits returning in 2022 and remaining a full percentage point of GDP lower, on average, throughout the budget window.

Under our alternative scenario, deficits would grow even higher, reaching $2.4 trillion or 8.2 percent of GDP by 2028. Deficits have only reached that percent of GDP three times since World War II – all during the Great Recession.

Debt Projections

Rising deficits will put pressure on today’s post-war record levels of debt. Previously, CBO projected debt to rise from 76 percent of GDP ($14.7 trillion) in 2017 to 91 percent ($25.5 trillion) in 2027, which would have meant debt of roughly 93 percent of GDP by 2028.

Under our updated baseline projections, debt will exceed the size of the economy within a decade, growing by nearly $15 trillion to 101 percent of GDP ($29.4 trillion) by 2028. This is within 5 percentage points of the all-time record set in 1946 just after World War II and is far higher than any other peacetime level of debt.

Under our alternative scenario, debt will exceed its historic record by 2027 and reach 113 percent of GDP ($33 trillion) by 2028. Although we have not yet run long-term projections, debt would likely continue to grow rapidly beyond 2028 and could be twice the size of the economy in about 25 years.

While our high and rising debt was already on an unsustainable path a year ago, our updated projections show substantial fiscal deterioration since then and suggest the country is approaching uncharted territory. These high levels of debt will most likely crowd out productive investment, slow wage growth, and could increase the likelihood of an eventual fiscal crisis.

Spending and Revenue Projections

Recent legislation has significantly changed spending and revenue levels over the next decade, especially in the near term. Not surprisingly, these changes have widened the gap between spending and revenue compared to CBO’s June baseline.

We project revenue will fall in the next few years but eventually recover to prior-law levels as much of the recent tax bill expires. Specifically, we estimate that as the tax law takes effect, revenue will drop from 17.3 percent of GDP in 2017 to 16.4 percent in 2019 – lower than it has ever been in the last 50 years other than in the aftermath of the last two recessions. We project revenue will remain below 2017 levels until 2022. After that, revenue will rise rapidly as a result of various expirations and future tax increases in the bill, reaching 18.5 percent of GDP by 2028. Without these expirations, we project revenue will remain below 17.3 percent of GDP through the entire budget window.

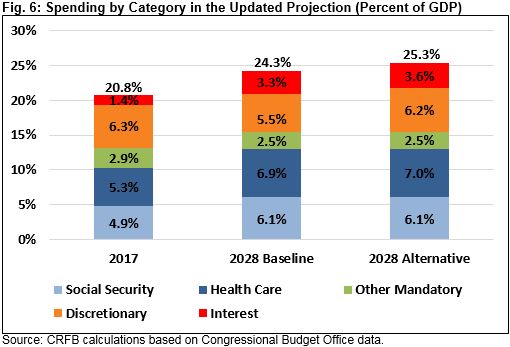

Meanwhile, spending is projected to rise rapidly. We estimate that spending will jump from 20.8 percent of GDP in 2017 to 21.8 percent in 2019, in part because of the budget deal’s near-term increase in discretionary spending. Spending will then gradually rise to 24.3 percent of GDP by 2028, the second-highest level as a share of GDP since World War II. Under our alternative scenario, spending will reach 25.3 percent of GDP by 2028, which would represent a new post-war record.

While the near-term spending increase is largely due to increased discretionary spending in the Bipartisan Budget Act, that spending eventually disappears under current law. Long-term spending growth is driven largely by the rising costs of Social Security, health care, and interest on the debt. Even under prior law, outlays would have totaled about 23.7 percent of GDP by 2028.

In fact, under our current law projections, Social Security and health care spending will rise from 10.2 percent of GDP in 2017 to 13 percent of GDP by 2028, while discretionary spending will fall from 6.3 to 5.5 percent (under our alternative scenario, it will fall only slightly to 6.2 percent).

Perhaps more troubling, rising debt and interest rates means that interest costs will be the fastest growing part of the budget. Under current law, we project interest will grow from $263 billion (1.4 percent of GDP) in 2017 to $965 billion (3.3 percent of GDP) by 2028, at which point it would be 14 percent of the budget. Under our alternative scenario, interest costs will exceed $1 trillion (3.6 percent of GDP), and the country will spend more on interest than defense or Medicaid.

Conclusion

Much has changed since CBO last published its budget and economic projections in June of last year, but much has also stayed the same. Debt remains at post-war record high levels, structural deficits remain large, and entitlement programs are slated to grow at an unsustainable pace as the population continues to age.

Yet legislation enacted since June 2017 has turned a dismal fiscal situation into a dire one. Revenue is lower, spending is higher, deficits are larger, and the national debt is rapidly headed toward a new record. To make matters worse, the pressure for policymakers to further increase deficits through various policy extensions has intensified.

Importantly, these projections also do not supplant the need for CBO's thorough budget outlook scheduled to be released in April. CBO does a much more rigorous analysis than we are able to with access to crucial data and sophisticated modeling. We merely seek to inform the conversation until CBO has a chance to release its full report.

A year ago, paying for new legislation and securing the solvency of various trust funds would have been sufficient to prevent debt from rising rapidly as a share of GDP. Unfortunately, lawmakers chose instead to ignore impending trust fund insolvencies and charge significant new tax cuts and spending hikes to the national credit card.

The complete disregard for budgetary constraints that lawmakers have shown in the past year – and in the past few years before that as well – have largely undone the progress made on deficits earlier in the decade.

As a result, an aggressive combination of spending reductions, revenue increases, and entitlement reform will be needed. Hopefully, lawmakers will quickly re-focus on deficit reduction to prevent debt from reaching unprecedented levels.