After the 2020 Election, Fiscal Challenges Await

The winner of the 2020 presidential election will begin his or her term facing a daunting fiscal situation. High deficits and debt, depleting trust funds, a series of deadlines and expirations, and economic uncertainty will shape the actions that the president can and must take while in office.

US Budget Watch 2020 is a project of the Committee for a Responsible Federal Budget designed to educate the public and hold presidential candidates accountable for the fiscal impact of their promised proposals. Throughout the 2020 election cycle, we will be issuing policy explainers, fiscal fact checks, budgetary scores, and other analyses.

Candidates are currently putting forward many new proposals related to health care, education, the environment, infrastructure, taxes, and other areas. Yet no candidate has explained how they will address the unsustainable fiscal costs of policies already in effect. Even discussion over how new policies or extensions will be paid for is increasingly scarce. Far too often, policymakers and commentators act as if new policies will pay for themselves or can be piled on to an already massive national debt.

The president inaugurated in 2021 will face a number of fiscal challenges, including:

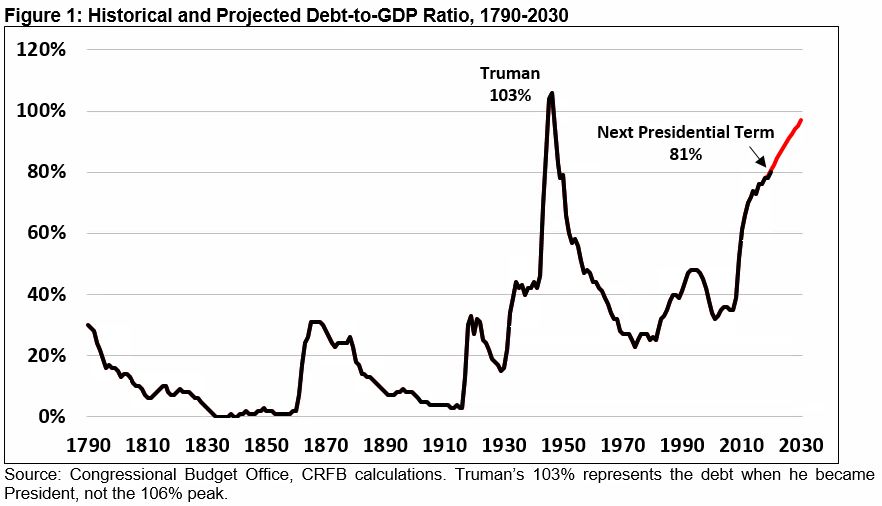

- Record Debt Levels. The next president will enter office with debt at 81 percent of the economy – higher than at any time in history outside of World War II. Under their watch, debt is projected to keep rising toward unprecedented levels.

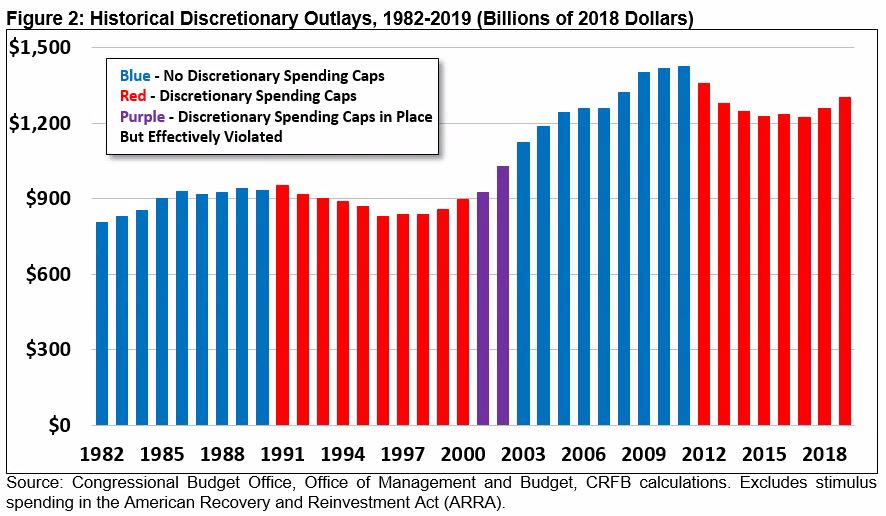

- The End of Discretionary Spending Caps. Since 2012, discretionary spending caps have limited annual appropriations. Those caps will end just eight months into the next presidential term.

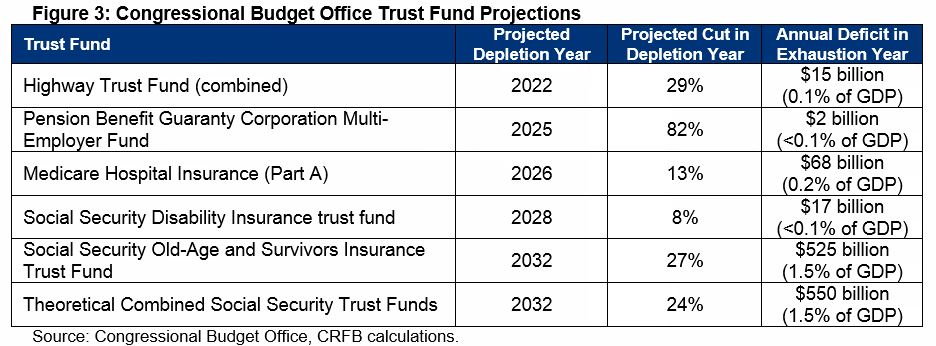

- Trust Funds Headed Toward Insolvency. The Highway Trust Fund, Pension Benefit Guaranty Corporation (PBGC) Multi-Employer fund, and Medicare Hospital Insurance (HI) trust fund are all projected to be exhausted by 2026. The Social Security trust funds are projected to be depleted between 2032 and 2035.

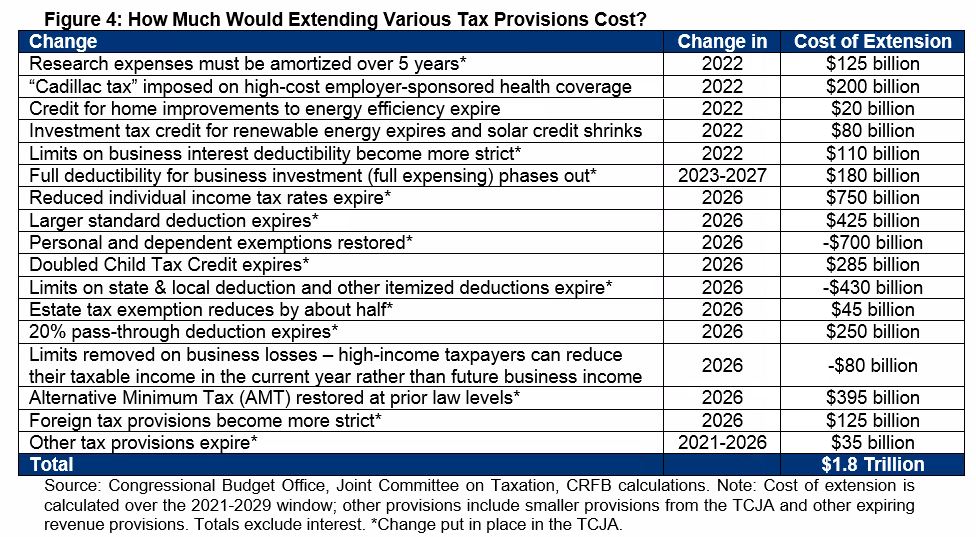

- Risk of Costly Tax Cut Extensions. Various tax changes are scheduled to take effect in the coming years, including the expiration of large parts of the Tax Cuts and Jobs Act (TCJA). Extending current tax policies would cost $1.8 trillion.

Though the president will want to focus on his or her own priorities, they will not be able to ignore the current fiscal situation. Presidential candidates should put forward plans to address these unprecedented budgetary challenges before the 2020 election.

Record Debt Levels

The next presidential term will begin with the country deeper in debt, relative to the economy, than at the start of any presidency besides Harry Truman. At about $18 trillion, debt held by the public will total about 81 percent of Gross Domestic Product (GDP) in early 2021. Based on the Congressional Budget Office’s (CBO) projections, debt will rise to 90 percent of GDP by 2025 and 95 percent by 2029 – the highest level since 1946 and third-highest year-end total in U.S. history.

The president in 2021 will face large annual deficits every year of their presidency. Under current law, assuming no recession, deficits will exceed $1 trillion every year and average $1.2 trillion – or 4.7 percent of GDP – between 2021 and 2025. Deficits will dramatically exceed the 50-year average of 2.9 percent of GDP and be larger than any time over the past three decades outside of the Great Recession, when deficits peaked at 9.8 percent of GDP.

These high deficit and debt levels will have considerable negative consequences that the president must contend with. They will leave the country with less fiscal space to combat the next recession, cause interest spending to rise rapidly and crowd out other priorities, permanently slow the rate of economic and income growth, put the country in a weaker global position, and increase the risk of an eventual fiscal crisis.

Debt cannot indefinitely grow faster than the economy, so the president will inherit a fiscal situation that is, by definition, unsustainable. Whoever is president in the early 2020s should take steps to place the country on solid fiscal ground.

The End of Discretionary Spending Caps

About 30 percent of federal spending is classified as discretionary and is appropriated every year by Congress. Throughout the 1990s and since 2012, the amount Congress spends on defense and non-defense discretionary programs has been limited through statutory spending caps. The caps in place since 2012 were set in the Budget Control Act (BCA) of 2011 and amended through various pieces of legislation – most recently the Bipartisan Budget Act (BBA) of 2019.

On September 30, 2021, about eight months into the next presidential term, discretionary spending caps are scheduled to disappear. In other words, there will be no legal constraint on discretionary spending beginning in fiscal year 2022 – the first full fiscal year in the next presidential term.

When no statutory caps are in place, discretionary spending levels are supposed to be set by a concurrent budget resolution as part of an overall budget plan – but for a variety of reasons, that too has not occurred much in recent years. Absent caps or a budget resolution, each chamber can essentially set its own discretionary spending levels without regard to the overall fiscal picture.

After the caps expire in 2021, it will be up to Congress and the president to decide how high to set spending levels and whether or not to establish a new set of discretionary spending caps or some alternative practice for setting spending levels. This decision has important consequences: there is a $1.6 trillion spending difference over ten years between freezing discretionary spending at 2021 levels or growing them with the economy. Without any constraint or context, there is high risk of a fiscal-free-for-all.

Trust Funds Headed Toward Insolvency

A number of important federal programs are financed through dedicated revenue sources and managed through federal trust funds. Several of these trust funds are scheduled to deplete their reserves in the coming years, and the next president must address their looming insolvencies.

CBO projects the Highway Trust Fund will be depleted by 2022, the Pension Benefit Guaranty Corporation (PBGC) Multi-Employer fund by 2025, and the Medicare Hospital Insurance (HI) trust fund by 2026. The president should deal with all three of these funds, each of which faces a large shortfall.

For example, Highway Trust Fund spending will exceed revenue by about $15 billion in 2022; closing that gap would require the equivalent of cutting spending by almost 30 percent or raising the gas tax by 60 percent (11 cents).

The Medicare Hospital Insurance (HI) trust fund, meanwhile, is projected to run a deficit of roughly $68 billion when its reserves are exhausted – meaning spending would need to be cut by 13 percent or the payroll tax rate increased by 28 percent (0.8 percentage points) immediately.

The Social Security trust funds will also approach the point of no return during the next presidential term. According to CBO, the theoretically combined old-age and disability trust funds will run out of reserves by 2032 – when the youngest retirees at the start of the next term turn 73. Social Security’s Trustees project trust fund depletion by 2035, when those retirees turn 76. Either way, Social Security will be unable to pay full benefits to most people who begin collecting during the next Administration without reform.

Absent legislative action, all Social Security benefits will be cut by 20 to 25 percent upon trust fund exhaustion. The next president has the opportunity to enact gradual adjustments to avoid this cut – future presidents will have a much smaller set of options at their disposal.

Risk of Costly Tax Cut Extensions

A number of provisions in the current tax code are scheduled to change in the coming years that, if allowed to take effect, will restore revenue to its historic levels and allow it to grow modestly over time. However, the president in office during the next term will face significant pressure to extend current tax policies. Ceding to this would cost $1.8 trillion through 2029, before interest.

Over the next presidential term, scheduled changes include the end of expensing of research costs, the initiation of a (twice delayed) Cadillac tax on high-cost health insurance plans, the expiration of clean energy tax credits, a tightening of limits on deducting business interest in 2022, and the phase-out of full expensing for business equipment in 2023. Avoiding these current law changes would cost $700 billion through 2029.

In the following presidential term, nearly all of the TCJA’s individual income tax provisions will expire. These include reductions in individual income tax rates, large expansions of the Child Tax Credit and standard deduction, a new deduction for business income, a reduction in the taxpayers affected by the estate tax and Alternative Minimum Tax (AMT), the elimination of personal and dependent exemptions, and limits to various deductions such as the $10,000 cap on the state and local tax deduction. Extending these policies would cost another $1.1 trillion.

The president will need to confront these changes in tax policy and lead the effort to decide which policies are allowed to occur, which are avoided or modified, and how to ensure any new costs don’t worsen an already dismal fiscal picture.

Conclusion

Whoever wins the 2020 presidential election will enter the next presidential term facing a fiscal situation unlike any other. With debt and deficits rising rapidly, major trust funds facing shortfalls, and significant pieces of legislation nearing expiration, it is imperative that he or she takes steps to address these and other fiscal challenges.

In recent years, policymakers have ignored the need to pay for new legislation, resulting in a significantly worse fiscal outlook than only a few years ago. Over the last term, $4 trillion has been added to the debt through 2029. And if these and other temporary policies are continued, debt will exceed record levels as a share of the economy by 2030.

The unprecedented challenges we face should motivate the president to fully pay for all new legislation and work to pass a plan to control our mounting debt and place it on a downward path, while also advancing policies that foster significant long-term deficit reduction. Doing so is critical to securing both our fiscal and economic future, and it will help restore the resources and flexibility needed to address other critical priorities.

As the 2020 presidential campaign ramps up, US Budget Watch 2020 will bring information and accountability to the 2020 presidential campaign by analyzing candidates’ proposals, factchecking their claims, and scoring the fiscal cost of their agendas.

By injecting an impartial, fact-based approach into the national conversation, US Budget Watch 2020 will help voters better understand the implications of the candidates' policies and what they will mean for the country’s economic and fiscal future.