Yes, Actually, Raising the Retirement Age IS a Good Idea

The knives are out, and they’re pointing at Social Security reform.

There is no one “right” way to fix the fiscal problems facing the country, but if there is one thing experts from all ideological perspectives tend to agree on, it is that with Americans living longer, we should raise the retirement age. Just ask House Majority Leader Steny Hoyer or House Minority Leader John Boehner. Or ask any member of the American Academy of Actuaries, for that matter.

So why then the slew of recent attacks on raising the retirement age? Sure, some are depressingly predictable made by groups determined to prevent any changes to Social Security benefits – actuaries’ warnings be damned. But others show that the pushback against raising the retirement age is gaining momentum even by those who previously supported it. If fixing the budget is a one-step-forward three-steps-back kind of process, markets are going to lose patience sooner than we were expecting.

Working longer is probably the single best thing people can do for their retirement security. The stock market’s plunge left savings pummeled and companies have pulled back from providing defined benefit plans. Staying in the workforce allows workers to save more money before retiring and go without wages for a shorter period of time. Importantly, it also improves the overall fiscal picture through higher income tax revenues and improved labor market incentives, helping to grow the economy, which benefits everyone.

When Social Security began, the retirement age was 65. Today, 75 years later, it is 66, moving up to 67. The good news is that life expectancy has improved greatly since then – by 17 years for men and 20 for women. In his recent piece in the Washington Post, Ezra Klein points out that these numbers are influenced in part by improvements in infant mortality. Yet even life expectancy at age 20 has increased by 9 years for men and 10 years for women.

| At Birth | At Age 20 | At Age 65 | ||||

| Men | Women | Men | Women | Men | Women | |

| 1940 | 61 | 66 | 67 | 71 | 77 | 78 |

| 2006 | 75 | 80 | 76 | 81 | 82 | 85 |

| 2050 (projected) | 80 | 84 | n/a | n/a | 85 | 87 |

In light of continued increasing longevity, it only makes sense that individuals would work longer. Raising the normal retirement age would serve as an important signal to encourage them to do so, and raising the early retirement age would go even further to promote longer working lives.

So why all the pushback on turning to the retirement age as part of the problem?

There are concerns that it would be regressive and unfair. Not so.

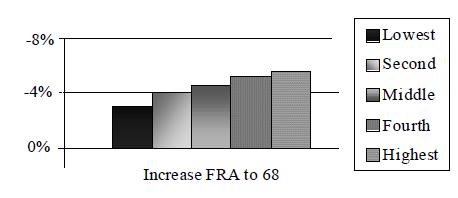

Even reform-opponent Dean Baker admits that “an increase in the NRA reduces benefits by the same percent for all workers” – and that analysis doesn’t account for disability benefits, which are completely protected from changes to the retirement age. When looking at the entire Social Security system, the Urban Institute finds that raising the NRA is in fact a progressive option and “benefit reductions from an increase in the [NRA] would increase with lifetime earnings.”

Benefit Reductions by Quintile in 2050 (percent relative to scheduled benefits)

Then there is the concern that some individuals may be physically unable to continue working past the current early retirement age of 62. This is a legitimate concern for about a fifth of young retirees today, but we shouldn't design the entire retirement piece of program around them since they can largely be assisted through the disability program, SSI, or other means. We need to be targeting benefits toward the old-old who have outlived their savings and really can’t work. Maintaining unaffordable benefits for 100 percent of people in order to protect 20 percent of people is like putting out a match with a fire extinguisher.

Back in 1950, the average retirement age was over 67, and more than 70 percent of 65 year olds worked. Today, the average retirement age is 62 and only 30 percent of 65 year olds work (this was true before the recession as well). Are we really going to argue that jobs are more physically intensive and people less able to work than back in 1950?

The barrage of arguments against Social Security reform aren't limited to the retirement age.

In his article, Ezra also argues that the Social Security gap isn’t that large -- and that we are better off letting the Bush tax cuts expire on high income earners than we are going after Social Security.

Yet Social Security and the higher-income tax cuts don’t actually have the same impact on the debt at all though there have been repeated attempts to equate them. From about 2021 on, the Social Security cash shortfall will grow larger than the value of those cuts – much larger as time goes on. (We’ll discuss this more in a future blog). Realistically, we should be talking about letting the tax cuts for the well off expire AND reforming Social Security. We’re going to have to do both, and much, much, more, if we really want to stabilize the debt.

Finally, Ezra makes the argument against Social Security changes in general because of the high level of efficiency, which he argues would make changes a zero-sum game. Ezra uses the low administrative costs of the system to make his case. But saying Social Security is efficient because SSA can cut checks on the cheap is like saying dropping money from a helicopter is efficient as long as we get a good price on the helicopter.

The real measure of efficiency should be how effectively Social Security meets its goal of improving retirement security, and at what cost to society. It’s an open question as to whether a program which gives some seniors more than $30,000 a year and leaves others in poverty is efficient, especially if it encourages under-savings and premature retirement in the process.

Done right, Social Security reform need not be zero-sum at all. If we can encourage people to work longer and save more, we can improve their personal retirement security, increase income tax revenue, and (by increasing labor and capital supply) improve overall economic growth, all while preserving Social Security for future generations.

This approach to shooting down all possible changes to strengthen Social Security presents a serious danger to our nation’s fiscal sustainability. Instead, it would be helpful for those who don’t want to touch Social Security benefits to show how they would fix the program on the tax side, and for those who don’t want to address it at all to show how they would fix the budget without changes to Social Security. There are ways to do both (though probably not ones most people would like when presented with the facts), but this effort at shooting arrows at all ideas is not the way to succeed in putting the program back on sound footing.