The Tax Cuts and Jobs Act Doesn't Comply with the Byrd Rule

While the Tax Cuts and Jobs Act (TCJA) under consideration in the House would satisfy reconciliation instructions requiring it add no more than $1.5 trillion to the deficit (which is far too much), as written it would violate the "Byrd rule" and thus would require 60 votes to pass in the Senate.

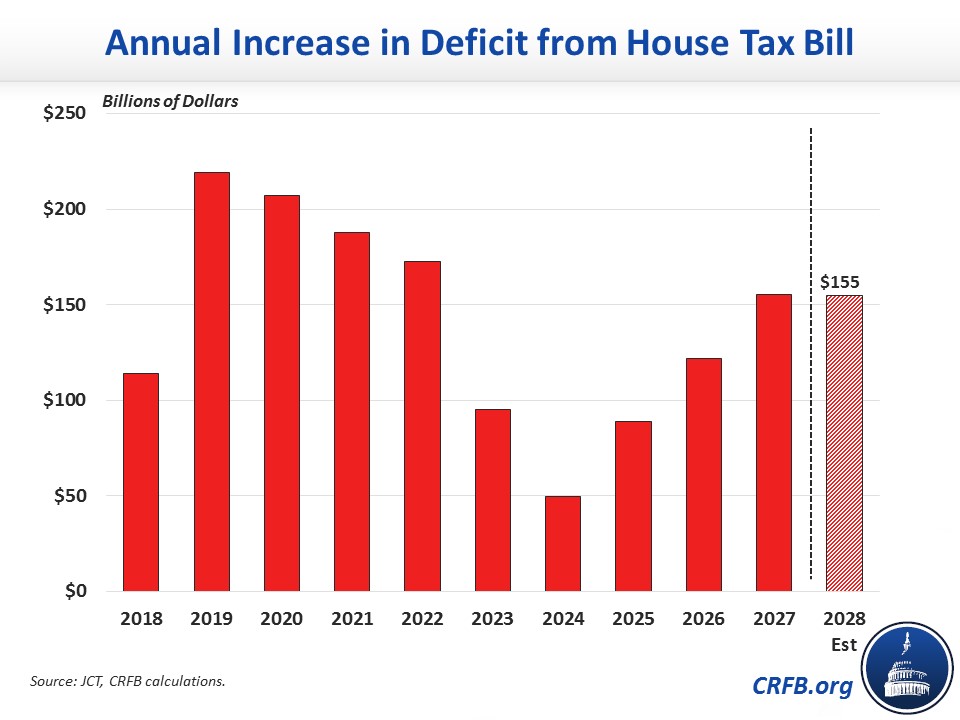

Most significantly, we estimate the legislation would add about $155 billion to the deficit in 2028; the Byrd rule does not allow reconciliation legislation to add to the deficit at all beyond the budget window (which currently ends in 2027).

Unfortunately, the "easy" options to solve for this problem – namely, allowing the corporate, individual or pass-through tax rate cuts to expire – would undermine much of the purpose of the bill and reduce or reverse any effects it may have on economic growth. The only reasonable way to pass real pro-growth pass tax reform in the Senate, therefore, is to put forward a bill significantly more fiscally responsible than the Tax Cuts and Jobs Act as currently written.

The Tax Cuts and Jobs Act Would Violate the Senate Byrd Rule

Reconciliation instructions provide for fast-track consideration of legislation in the Senate, allowing such legislation to be passed with a simple majority rather than a filibuster-proof 60-vote super majority. However, the Byrd rule places some restrictions on what can be considered under reconciliation; reconciliation can only include policies that directly impact the budget, cannot make direct changes to Social Security, and must not add to the deficit in future years outside the budget window. Appendix I below explains the Byrd rule in more detail.

The TCJA clearly violates the Byrd rule, most significantly by adding to the deficit beyond the budget window. In 2027, the TCJA would cost $156 billion. By our estimate, the TCJA will cost $155 billion in 2028 alone – which is a significant violation of the Byrd rule and cannot be attributed to an estimating error or fixed with slight adjustments to the legislation. If the TCJA were introduced on the Senate floor, senators could therefore raise points of order against any provisions that add to the debt beyond the budget window.

The TCJA may also include other smaller Byrd violations. For example, it generates $74 billion in "off-budget" revenue for Social Security, including $53 billion in additional revenue from certain business income being reclassified as wage income as well as other smaller provisions increasing the amount of taxable wage income. The Senate Parliamentarian may rule some of these provisions to be direct enough changes to the Social Security payroll tax that they cannot remain in the legislation without it losing privilege.

Complying With the Byrd Rule Will Require Making the TCJA Either Much Worse or Much Better

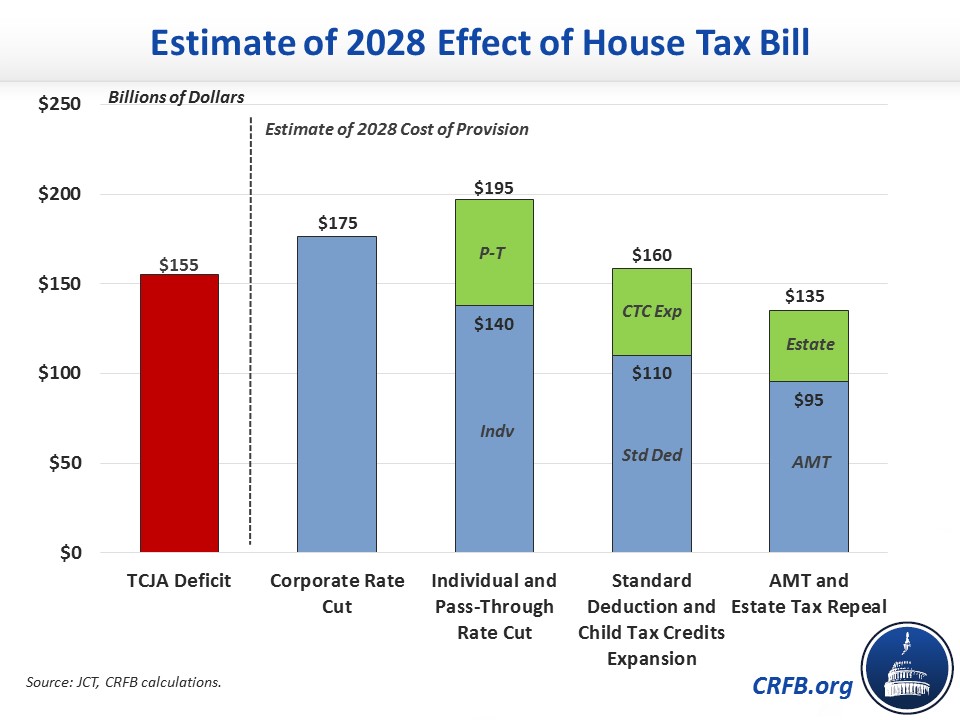

Because the TCJA adds so much to the deficit in 2028, significant changes would be required to make it Byrd-rule compliant. One oft-discussed option is to take a page out of the book from the 2001/2003 tax cuts and sunset parts of the tax cuts after a decade. However, these sunsets would need to be quite significant.

One option would involve letting the corporate tax rate cut expire in 2027 while retaining the corporate base broadening. We estimate the corporate rate cut costs about $175 billion in 2028, suggesting its expiration would cover the TCJA's 2028 deficit (actual revenue from expiration will differ some). However, as the Tax Foundation and the American Enterprise Institute's Alan Viard have both pointed out, a temporary corporate tax cut would undermine the inventive for businesses to invest and may even be more anti-growth than no corporate tax cut at all.

If tax reform fails to grow the economy, arguments that it will be paid for with dynamic scoring also go out the window.

Other possible expirations are also unattractive. Lawmakers could let all the individual and pass-through rate cuts expire, setting the stage for a large future tax increase on all individuals and many businesses. Or they could allow all the low-income and middle-class tax cuts to expire by ending the expanded standard deduction and child tax credit (while retaining the repeal of the personal exemption). Or they could combine policies – for example, restoring the estate tax and the alternative minimum tax while also letting other tax cuts expire.

Any of these expirations would fundamentally undermine the tax reform package and create a huge new "fiscal cliff" a decade from now.

A preferable alternative would be to make the legislation itself fiscally responsible so that it doesn't add to future deficits even when made permanent. Options for doing this include adding an across-the-board tax expenditure cap for higher earners, identifying more tax breaks to repeal or reform, trade temporary expensing and the modest interest deduction limit with a more aggressive and permanent expensing-for-interest swap that raises revenue over the long term, cutting spending, scaling back some of the bill's rate reductions, or including a combination of these approaches.

Tax reform that is permanent and fiscally responsible is much more likely to grow the economy than temporary, debt-financed tax cuts. Taking a fiscally responsible approach, policymakers would not only comply with the Byrd rule but also put forward a better and more pro-growth tax reform plan.

Appendix I: What is the Byrd Rule?

Although reconciliation bills are granted many privileges that are not available to most other legislation (see Reconciliation 101), they remain bound by several conditions. Some of these restrictions were championed by the late Senator Robert Byrd (D-WV) and established in Section 313 of the Budget Act, jointly referred to as the “Byrd Rule.” The Byrd Rule disallows “extraneous matter” from being included in a reconciliation bill – extraneous matter being defined by three main categories of restrictions.

First, reconciliation legislation must only involve budget-related changes and cannot include policies that have no fiscal impact, that have “merely incidental” fiscal impact, or that increase the deficit if the committee did not follow its reconciliation instructions (including proposals outside of a committee's proper jurisdiction – see more on this below). Second, reconciliation bills cannot change Social Security spending or dedicated revenue, which are considered “off-budget.” However, provisions that make incidental changes to Social Security spending or revenue are likely okay.

Finally, and most relevant to the current tax debate, provisions in a reconciliation bill cannot increase the deficit in any fiscal year after the window of the reconciliation bill (usually ten years in the future). This means that every year outside of the budget window must have any revenue cuts offset by equal amounts of spending cuts or revenue increases.

The Byrd Rule provides a "surgical" point of order that senators can raise to strike any provision in violation of the rule without blocking the entire bill. However, the Byrd Rule can also be waived by 60 votes. Even though this point of order only exists in the Senate, it can de facto govern the House too since it can be applied to any conference report. The House can pass an initial bill in violation of the Byrd Rule and the Senate could take up that bill under the expedited reconciliation procedures (i.e. the violations would not be "fatal" to the reconciliation bill), but any Byrd rule violations would need to be corrected by amendments or removed through a point of order so that any bill approved by the Senate and thus being able to become law will need Byrd Rule compliance or 60 votes to waive it.

Appendix II: Where to Read More

For more information on reconciliation and tax reform, read the following: