Raising the Retirement Age Still Is a Good Idea

Update: Chuck Blahous joined the debate today in a piece over at e21, setting the facts straight on longevity increases, the retirement age, and how exactly the Fiscal Commission's plan would affect retirement benefits.

Several months ago, CRFB responded to a growing chorus of voices who were arguing against raising the retirement age. Well, it seems like we’re back at it again in support of raising the retirement age (click here to read the original post from September).

The blogosphere is alive with another round of attacks on CRFB board member and Fiscal Commission co-chair Alan Simpson for speaking out about the need for Social Security reform regarding changes in life expectancy. The current line of criticism is based on statements he has made regarding changes in life expectancy since Social Security was created, with some critics going so far as to suggest that his use of statistics they don’t like should disqualify him from being part of the discussion regarding Social Security reform.

In his comments, Simpson stated that average life expectancy was when 63 in 1940 and has increased to over 77 now. None of his critics actually dispute that statement, because they are factually accurate. Rather, he is being attacked because he is not using the measure of life expectancy that his critics prefer. They argue that instead of looking at average life expectancy at birth, which is affected by children who die in infancy, the appropriate measure is to look at life expectancy at age 65. But that measure has drawbacks when discussing Social Security as well since it does not account for the many adults who did not make it to retirement.

As the Social Security Administration historian has suggested “a more appropriate measure is probably life expectancy after attainment of adulthood.” Social Security was created as a social insurance program, to insure against the risk that one would outlive his or her savings. In 1940, less than 60 percent of the population survived from age 21 to age 65, meaning that even when infant mortality is removed from the equation, many adults never made it to the retirement age. Today, roughly 80 percent of the population survives from age 21 to 65. This is an important point that is missed by only looking at life expectancy at age 65.

The increase in longevity has been a great accomplishment of modern society, and is in no way the problem. The point that Simpson was making is that Social Security has not kept up with demographic changes since the program was created. Reforms to strengthen Social Security should take these demographic changes into account.

And whether you look at life expectancy at birth, after attaining adulthood, or at age sixty five, the fundamental conclusion remains the same – life expectancy has increased much faster than the normal retirement age for Social Security, resulting in a greater proportion of society receiving benefits, not to mention more people receiving benefits for a longer period of time than was the case when Social Security was created. Simpson did not suggest that this meant the creators of Social Security didn’t expect anybody to collect benefits when it was created, as some have suggested.

This point remains true even using his critics preferred approach of looking at life expectancy at age 65. The average life expectancy of a male turning 65 in 1940 was 12.7 years, while a male turning 65 today will on average live another 18.1 years (age 83.1). That is an increase of more than 40% in life expectancy at age 65 from 1940 until now. Put another way, the average man claiming benefits at the Normal Retirement Age in 1940 would receive benefits for less than 13 years, while the average man claiming benefits at the Normal Retirement Age of 66 today will receive benefits for over 17 years.

The increased number of years the average worker will receive benefits is even more pronounced when using life expectancy at age 20. Life expectancy at age 20 has increased by about 9 years for men and 10 years for women from 1940 compared to recent years. This means that even with the NRA increase under the Fiscal Commission plan, the average twenty year old a male will receive benefits for six more years than was the case in 1940 and the average twenty year old female would receive benefits for seven more years.

| Life Expectancy | At Birth | At Age 20 | At Age 65 | |||

| Men | Women | Men | Women | Men | Women | |

| 1940 | 61 | 66 | 67 | 71 | 77 | 78 |

| 2006 | 75 | 80 | 76 | 81 | 82 | 85 |

| 2050 (Projected) | 80 | 84 | n/a | n/a | 85 | 87 |

In light of continued increasing longevity, it only makes sense that individuals would work longer. As we’ve noted before, in addition to the fiscal benefits, working longer is probably the single best thing people can do for their retirement security. Staying in the workforce allows workers to save more money before retiring and go without wages for a shorter period of time.

There is a legitimate concern that some individuals may be physically unable to work longer. But that still remains an issue whether we raise the retirement age or not. We are better off providing more targeted relief rather than maintaining unaffordable benefits for 100 percent of the population in order to protect the 20 percent who can’t work longer. The Fiscal Commission provided this through a “hardship exemption”, while others have suggested using the disability program, supplemental security income (SSI), or through other means.

It is also worth noting that as life expectancy has gone up, average age of retirement has continued to fall. As Chuck Blahous, one of the Social Security Public Trustees, has noted, “the empirical evidence is clear that a physical inability to work is not the sole or even the primary determinant of workforce participation rates for those in their 60s.” In 1955, before the lower early eligibility age of 62 was established, 57 percent of American males aged 65-69 were in paid employment. By 2007 this had declined to 35 percent. Does anyone believe that American men are working in more physically demanding jobs or in worse health now than they were in 1955?

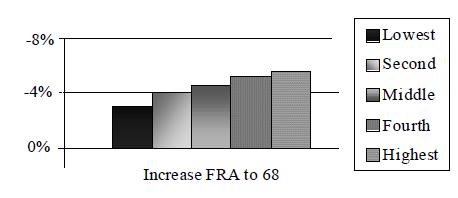

Finally, there are concerns that raising the retirement age would be regressive and unfair. Not so. When looking at the entire Social Security system, the Urban Institute actually found that raising the NRA is progressive showing that “benefit reductions from an increase in the [NRA] would increase with lifetime earnings.”

Benefit Reductions by Quintile in 2050 (percent relative to scheduled benefits)

Raising the retirement age is a broadly supported policy change which would not only improve Social Security’s finances, but also encourage economic growth and lead to higher income tax revenues. It has been endorsed by the Fiscal Commission, the Academy of Actuaries, Third Way, Speaker of the House John Boehner, Minority Whip Steny Hoyer, and a long list of other people with Social Security plans. The increase in Simpson-Bowles Fiscal Commission is, if anything, too modest, increasing the retirement age at a slower rate than life expectancy is expected to increase – lifting it only two years over the next 75.

Let’s stop fighting over semantics and start enacting policies to put our country on a sustainable path.