OBBBA Would Cost More on a Dynamic Basis, Says CBO

The Congressional Budget Office (CBO) released its dynamic score of the House-passed One Big Beautiful Bill Act (OBBBA), finding that the bill would increase deficits by $3.4 trillion including interest – $432 billion more than under the conventional estimate of $3.0 trillion. The increase is driven by the higher interest rates resulting from the bill, which outweigh revenue gains from stronger economic growth.

In line with other credible estimates, CBO finds that OBBBA would:

- Increase deficits by $3.4 trillion over the next decade on a dynamic basis, compared to $3.0 trillion on conventional basis, including interest.

- Increase deficits by $432 billion as a result of economic feedback – with $85 billion of lower primary deficits counteracted by $517 billion of higher interest costs.

- Boost output by 0.5 percent over the decade, including 0.4 percent in 2034.

- Boost the average interest rate on the ten-year Treasury note by 14 basis points.

- Increase total net interest costs by $1.1 trillion over the decade.

OBBBA Would Cost $432 Billion More on a Dynamic Basis

Under its conventional estimate – which accounts for behavioral changes but not macroeconomic changes – CBO estimates OBBBA would add $2.4 trillion to primary deficits, or $3.0 trillion including interest, through 2034. However, this estimate does not incorporate macrodynamic effects, and CBO finds that OBBBA will also boost economic output, inflation, and interest rates as a result of its tax cuts, spending cuts, additional borrowing, and other policy changes.

CBO’s macrodynamic estimate finds these effects will generate an additional $124 billion of revenue, $39 billion in higher noninterest spending, $441 billion of additional interest costs on existing debt as a result of higher interest rates, and $76 billion of additional costs from OBBBA debt service. In total, these changes will increase the deficit impact of the bill by $432 billion, or about 15 percent.

Overall, CBO estimates OBBBA would boost deficits by $3.4 trillion through 2034 on a dynamic basis, compared to $3.0 trillion on a conventional basis. For scorekeeping purposes, CBO’s official dynamic estimates include the effect of interest rate changes, but not debt service. Using this convention, OBBBA will cost $2.8 trillion on a dynamic basis, as opposed to $2.4 trillion on a conventional basis.

Deficit Impact of OBBBA

| Deficit Impact Excluding Debt Service | Full Deficit Impact Including Debt Service | |

|---|---|---|

| Conventional Score | -$2,416 billion | -$2,967 billion |

| Dynamic Revenue Impact | $124 billion | $124 billion |

| Dynamic Spending Feedback | -$39 billion | -$39 billion |

| Dynamic Interest Feedback | -$441 billion | -$517 billion |

| Dynamic Score | -$2,733 billion | -$3,399 billion |

| Memo: Dynamic Feedback Effect | -$356 billion | -$432 billion |

Source: Congressional Budget Office

OBBBA Would Increase Output, Inflation, and Interest Rates

CBO finds OBBBA would boost output by an average of 0.5 percent over the decade. They estimate the bill would generate near-term stimulus to boost output by 0.9 percent in 2026. After 2026, the economy will grow slower as stimulus fades, the negative effects of debt grow, and several pro-growth tax cuts expire. By 2034, CBO estimates output will be 0.4 percent higher than current law – meaning growth will improve by 0.04 percent per year.

In addition to boosting economic growth, CBO estimates that OBBBA would increase price levels and interest rates. As a result of higher borrowing, CBO estimates the bill will boost the ten-year Treasury yield by an average of 14 basis points – and presumably more by the end of the decade.

CBO economic projections are consistent with other credible estimates. On the low end, Yale Budget Lab finds OBBBA would shrink output by 0.1 percent in 2034; on the high end, Tax Foundation finds it would boost long-run output by 0.8 percent. Analysis from Penn Wharton Budget Model (PWBM), Tax Policy Center, and the American Enterprise Institute all find the same 0.4 percent boost as CBO.

CBO’s interest rate projections also appear consistent with outside estimates. Due to a combination of higher debt and higher interest rates, CBO estimates OBBBA will increase total interest costs by $1.1 trillion through 2034.

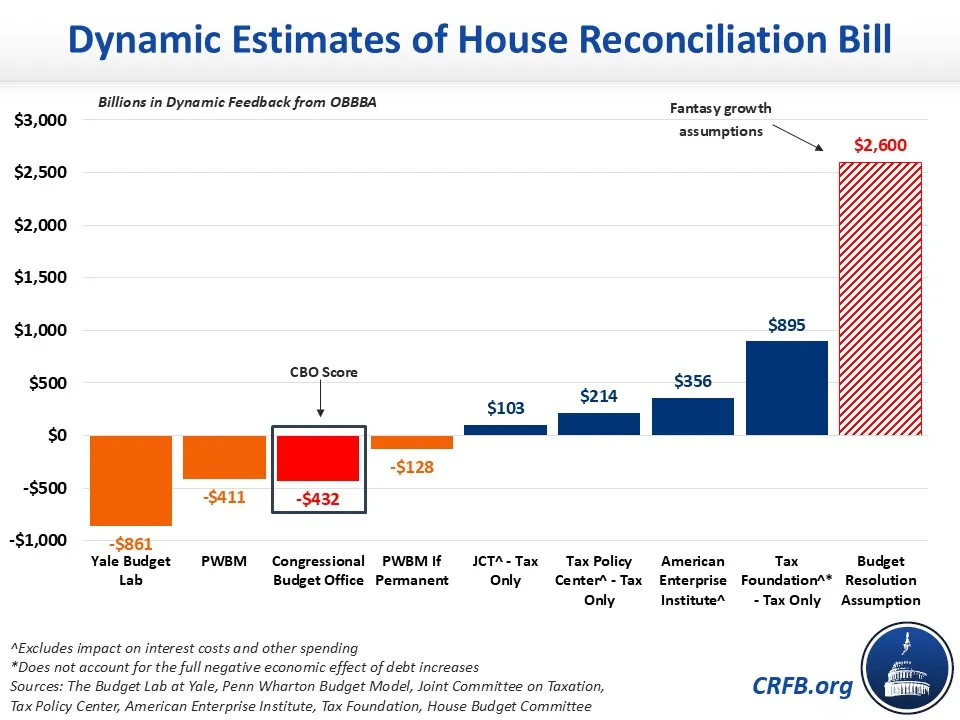

CBO’s Estimates Are Consistent with Other Modelers

CBO’s dynamic estimate is within the range of other modelers, who show a wide gamut of possible outcomes but also use varied methodologies that make it difficult to compare them on an apples-to-apples basis.

On the high end, the Tax Foundation estimates OBBBA will produce nearly $900 billion of dynamic revenue feedback – though their estimates do not account for the impact of debt on either Gross Domestic Product (GDP) or interest rates and costs. Other estimates which find positive feedback range from $100 billion to $360 billion and only include revenue effects. This is similar in magnitude to CBO’s $124 billion estimate for higher revenue.

Estimates which incorporate the effect of OBBBA on interest rates and costs all find negative feedback. The Yale Budget Lab estimates roughly $860 billion of dynamic losses – driven mainly by higher interest costs. Penn Wharton Budget Model finds $411 billion of dynamic losses – though that number might be somewhat higher on a comparable basis with CBO.

No credible estimate finds the OBBBA will pay for itself, as assumed in the budget resolution.

* * *

CBO’s dynamic score confirms that the House-passed OBBBA will not come close to paying for itself with economic growth; in fact, its dynamic feedback will add to the bill’s price tag by pushing up interest rates.

Rather than assuming fantastical growth scenarios, the House and Senate should add offsets to the bill to ensure that it does not increase already-unsustainable national debt and should replace the many temporary provisions in the bill with a few permanent ones. A permanent bill with more offsets than costs will not only reduce deficits and debt, but also help to grow the economy rather than shrinking it.

Dynamic Estimates of OBBBA (FY 2025-2034, billions)

| Conventional Estimate | Dynamic Estimate | Dynamic Feedback | % Dynamic Feedback | GDP Impact (2034) | |

|---|---|---|---|---|---|

| Congressional Budget Office | -$2,967 billion | -$3,399 billion | -$432 billion | -15% | +0.4% |

| Joint Committee on Taxation – Tax Only^ | -$3,819 | -$3,716 | +$103 | 3% | +0.2%* |

| Yale Budget Lab | -$2,677 | -$3,538 | -$861 | -32% | -0.1% |

| Penn Wharton Budget Model | -$2,787 | -$3,198 | -$411 | -15% | +0.4% |

| Penn Wharton Budget Model – If Permanent | -$4,425 | -$4,553 | -$128 | -3% | +0.2% |

| Tax Foundation - Tax Only^ | -$4,007 | -$3,112 | +$895 | 22% | +0.8%* |

| American Enterprise Institute^ | -$2,416 | -$2,060 | +$356 | 15% | +0.4%* |

| Tax Policy Center - Tax Only^ | -$3,798 | -$3,584 | +$214 | 6% | +0.4% |

Sources: CBO, JCT, The Budget Lab at Yale, Penn Wharton Budget Model, Tax Foundation, the American Enterprise Institute, and the Tax Policy Center. Estimates are of primary deficit, unless specified otherwise.

*JCT's GDP impact is over 2030-2034, Tax Foundation's GDP impact is "long-run, and AEI GDP impact is in 2035.

^Estimates exclude interest costs on new debt for OBBBA.