Medicare Advantage Costs Continue to Rise

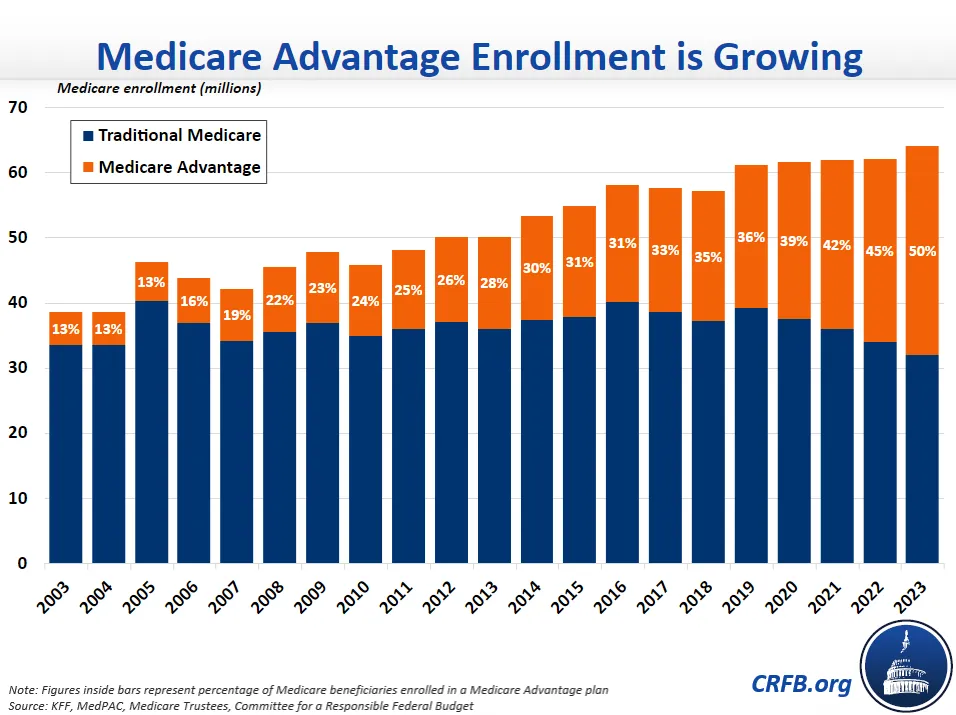

The Centers for Medicare and Medicaid Services (CMS) recently announced that Medicare Advantage (MA) plans will receive an 8.5 percent payment increase in calendar year 2023. This large increase comes as the Medicare Payment Advisory Commission (MedPAC) projects that 2023 will mark the first time that over half of all Medicare beneficiaries will be enrolled in the program’s private insurance plans. It also comes as the Medicare Hospital Insurance Trust fund is just four years from insolvency.

According to CMS, the payment increases are the result of underlying Medicare cost growth (4.9 percent) and risk score increases (3.5 percent). As we explain in our Health Savers Initiative brief on reducing MA overpayments, the risk score growth is partially the result of incentives that lead MA plans to report enrollee health diagnoses in ways that make their beneficiaries appear sicker than they are relative to similar traditional fee-for-service (FFS) Medicare beneficiaries, which leads to growing risk scores and higher payments.

CMS has the authority to account for this behavior through what is called a “coding intensity adjustment.” CMS is required by law to make a minimum adjustment, but that adjustment hasn’t changed since 2018 and CMS has never increased it above the minimum amount, despite evidence that the problem is large and getting worse. With the large payment increase set for 2023, it might have been an opportune time for CMS to start ramping up the adjustment.

Two recent letters from members of Congress expressed concern with the recent MA payment increase and with MA overpayments in general. A letter to the Administrator of CMS, led by Representatives Katie Porter (D-CA), Rosa DeLauro (D-CT), and Jan Schakowsky (D-IL), and Senator Elizabeth Warren (D-MA), expressed worry over the approaching insolvency of the Medicare trust fund and the MA program. It accurately pointed out that most evidence suggests MA has failed to achieve overall health savings for the federal government and that FFS Medicare beneficiaries are subsidizing the profits of MA private insurance plans.

A letter to the Secretary of the Department of Health and Human Services (HHS), led by Representative Pramila Jayapal (D-WA), pointed specifically to concerns about risk scores and the need for a larger coding intensity adjustment. The letter directly cited the work of our Health Savers Initiative and called for implementing our suggested method for determining the level of adjustment to more accurately reflect the health of MA beneficiaries. Doing so would save Medicare $355 billion over a decade and close over half of the Medicare trust fund's solvency gap.

A recent Health Affairs Forefront article by Dr. J. Michael McWilliams, titled “Don’t Look Up? Medicare Advantage’s Trajectory And The Future Of Medicare,” does an excellent job of diving into the crucial importance of the growth in both MA beneficiaries and costs to the future of the Medicare program.

McWilliams explains how MA was built on top of FFS Medicare: the design was to create a competition to test whether private plans could provide the same or better benefits at lower costs. Yet, that program design won’t be fiscally sustainable if a majority of beneficiaries are in MA plans that get paid more per beneficiary, and the “competition” is to allow MA to provide more benefits at higher costs.

He provides two legislative paths forward. The first is to even the playing field by increasing benefits in FFS Medicare – which would make them mandatory for MA enrollees as well instead of optional – and financing those benefits through the elimination of MA subsidies. Unfortunately, recent proposals to expand Medicare benefits would do so without financing the benefits by reducing MA subsidies, which could have cut their costs nearly in half.

The second path is to make modest cuts in MA payments, to control payment growth, and to promote adequate competition amongst MA plans but without increasing FFS Medicare benefits. This path would lock in MA’s substantial role in Medicare while reducing Medicare spending rather than shifting it from MA to FFS Medicare.

As the Medicare trust fund approaches insolvency in 2026, MA reforms present an opportunity to save the trust fund. Ultimately, to reduce the strain of federal health care programs on the federal budget and to ensure Medicare solvency, the rapid growth of MA will need to be addressed. Hopefully, more members of Congress will join their colleagues in promoting the need to reduce MA overpayments.