ARCHIVE: How Long Before Cancelled Student Debt Would Return?

Note: (7/6/2022): This analysis is now out of date. We released an updated version of this analysis, available here, which includes updated estimates of the time it would take for the amount of student debt owed to the federal government to return to $1.6 trillion if $10,000 or $50,000 per borrower is cancelled, or if all student debt owed to the federal government is cancelled.

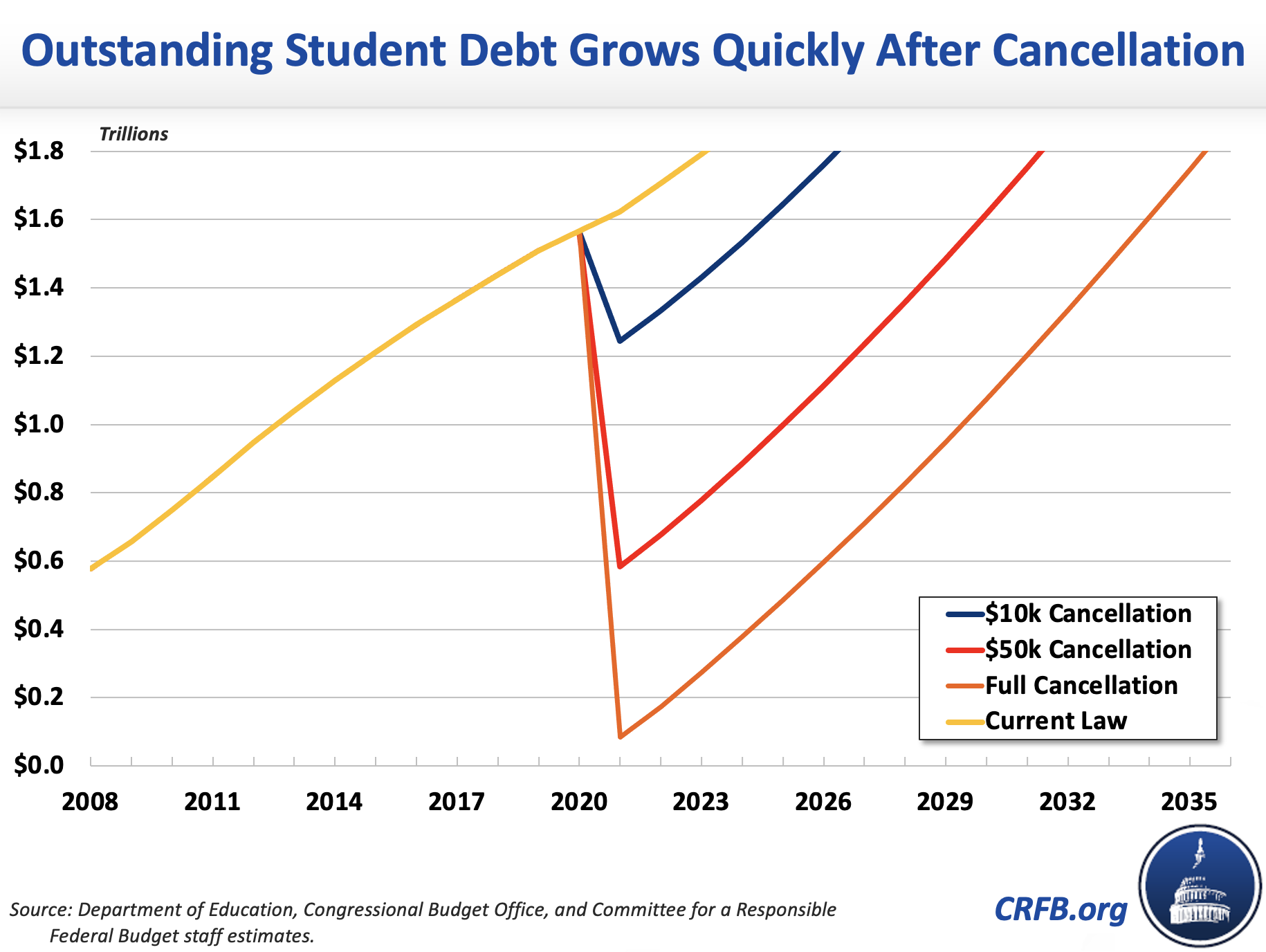

Federal student loan borrowers currently owe $1.6 trillion of student debt to the federal government. Cancelling some or all debt for current borrowers would reduce the debt burden. However, without underlying reforms to reduce the overall cost of, or the amount borrowed for, education, this reduction would only be temporary.

We estimate that absent other reforms in federal financial aid, outstanding federal student loan debt would return to the current $1.6 trillion level relatively soon after cancellation.1With conservative assumptions, we find:

- Debt would return to $1.6 trillion by fiscal year 2025 if $10,000 per borrower was cancelled.

- Debt would return to $1.6 trillion by 2030 if $50,000 per borrower was cancelled.

- Debt would return to $1.6 trillion by 2035 if all debt was cancelled.

- In real dollars, student debt would return to its current level in 2027 assuming $10,000 in cancellation, 2034 with $50,000 cancelled, and 2039 for full cancellation.2

Importantly, these projections assume no change in borrower behavior. In reality, debt cancellation would likely lead to increased borrowing, slower repayment, and larger tuition increases as borrowers and schools would expect another round of cancellation in the future. Any behavioral changes would mean the portfolio would return even faster to its current size.

Projected Student Debt Growth After Cancellation

The total outstanding federal student loan portfolio is on track exceed $1.6 trillion by the end of the fiscal year. Using data from the Department of Education, we estimate that cancelling $10,000 of student debt would reduce the portfolio to just under $1.2 trillion, cancelling $50,000 would reduce it to a little over $500 billion and cancelling all debt would, of course, reduce the portfolio to $0. But after cancellation, the loan portfolio would grow quickly and soon return to its current level in each scenario.

Two factors drive the rapid expected portfolio growth. First, lower balances resulting from debt cancellation would also reduce the pace of repayment relative to the current student loan portfolio. We estimate that the amount would drop from $80 billion to $62 billion in the years immediately following the $10,000 per borrower cancellation and then will slowly build back up. There is a lag in the increase in repayments because the portfolio would be comparatively younger, with a higher proportion of debt being in school or grace compared to before cancellation. For $50,000, it would drop to $25 billion, and for full cancellation, it would drop to $0.

The lower repayment amount would exacerbate the growth in the first few years because interest will still be accruing on the new loans that are not being paid back. That means faster growth for the portfolio than during normal circumstances. As a result, the more debt that is cancelled, the faster the portfolio grows after cancellation.

Secondly, new borrowing would continue to accrue at at least the previous pace (in reality, it would likely accrue faster due to moral hazard). We estimate that starting in 2022 loan origination volume will grow at a rate of 3% from $89 billion, which is in line with the Congressional Budget Office’s (CBO’s) baseline after adjusting for lower volumes due to the pandemic.3

Instead of focusing on nominal portfolio values, one could look at outstanding debt in real (inflation-adjusted) values. This becomes especially useful as we look beyond this decade, as comparing dollar values becomes less meaningful over time.

In real dollars, using the GDP deflator, we project outstanding debt would return to its current level in 2027 for $10,000 of forgiveness, in 2034 for $50,000 of forgiveness, and in 2039 for full cancellation.

Behavior Effects Will Worsen Student Debt Estimates

While our estimates show that after cancellation student debt would grow rapidly, our methodology is conservative and assumes no behavioral changes. In reality, debt is likely to increase even faster than we project due to the moral hazard effect associated with debt forgiveness.

Specifically, we expect one-time debt cancellation to lead to faster debt accumulation as borrowers expect a higher likelihood of further cancellation down the road. We expect this to manifest in two ways.

First, debt cancellation would likely lead to additional borrowing. Both non-borrowers and those borrowing below the maximum allowed (especially graduate students) may be more willing to increase their borrowing if they think there is a chance their debt will be forgiven.

Second, some borrowers would pay down their loans more slowly in hope of further forgiveness down the line. Those borrowers who are paying more than their required payment to reduce their debt, for example, are more likely to reduce their payments closer to the required amount. Others may enter Income-Driven Repayment (IDR) programs or consolidate debt in order to extend their repayment term. Absent a future jubilee, these choices would often lead to higher overall debt repayment costs due to accrued interest, but they may be advantageous if there is a reasonable chance of further debt cancellation.

These behavioral changes don’t need to be massive or widespread to meaningfully reduce the amount being repaid per year. Even if some borrowers make some adjustments, it could advance the date by which student debt returns to today’s levels.

A Short-Term Fix to a Structural Problem

We’ve previously shown that student debt cancellation would be regressive and would fail to stimulate the economy, and this new analysis shows that debt cancellation would at best be a temporary fix. Whether the federal government were to cancel $10,000 per borrower, $50,000 per borrower, or all outstanding federal student loan debt, the overall portfolio would return to its current size in a relatively short amount of time. Rather than blanket debt cancellation, policymakers should focus on reducing the cost growth associated with higher education itself. Such reforms could be coupled with targeted relief and support for borrowers and students with serious financial need or hardship.

1 To arrive at this estimate, we used a combination of our estimates for repayment with CBO’s projected growth of loan originations in the coming decade. We use CBO’s projected growth rate for the next decade, but start from a lower base to account for new data that has come out since CBO’s February 2020 projection. We assume a slightly lower growth rate in the following decade. We project that outstanding federal student loan debt will reach $1.62 trillion by the end of FY 2021. All calculations are in fiscal years.

2 Real dollar estimate based on GDP deflator from CBO’s February 2021 economic forecast.

3 Based on data from the Department of Education, we estimate $85 billion in loan originations for FY 2021, which is lower than usual and likely due to the pandemic. We expect originations will bounce back to $89 billion in FY 2022.

What's Next

-

Image

-

Image

-

Image