Playing By the (Budget) Rules: Understanding and Preventing Budget Gimmicks

The breakdown in the federal budget process and erosion of budget discipline have led to the increasingly pervasive reliance on budget gimmicks. While a number of budget rules and norms exist to enforce fiscal discipline, budget gimmicks provide legal workarounds to these rules and norms.

Increasingly, lawmakers have relied on budget gimmicks to circumvent discretionary budget caps, pay-as-you-go budget rules, and a variety of other budget enforcement mechanisms. Budget gimmicks are also used to paint more favorable fiscal and budgetary outcomes than are likely to be the case, to hide long-term debt increases, and to allow lawmakers to take credit for savings that will not materialize.

In this paper we discuss 20 types of budget gimmicks, describe how they have been used in the past, and offer suggestions to limit or prohibit their future use. The types of gimmicks we discuss include:

Assumption Gimmicks

- Unrealistic Policy Assumptions

- Rosy Economic Scenarios

- Magic Asterisks and Unspecified Savings

- Inflated Savings Estimates

- Shopping for Estimates

Manipulating the Budget Window

- Arbitrary Phase-Ins

- Front-Loading Costs, Back-Loading Savings

- Pushing Costs Outside the Budget Window or Savings Inside the Window

- Using Temporary Savings to Offset Permanent Costs

- Arbitrary Policy Sunsets

- Back-Loading Costs Beyond the Ten-Year Window

- Changing the Ten-Year Window to Evade Fiscal Responsibility

- Counting Timing Shifts as Budgetary Savings

Discretionary Spending Gimmicks

- Using OCO to Circumvent Discretionary Spending Caps

- Counting Planned War Spending Reductions as Savings

- Phantom Savings from Uncapped Discretionary Spending

- Counting Savings from Extending Discretionary Spending Caps

- Phony Changes in Mandatory Programs (CHIMPs)

Other Gimmicks

Ultimately, the best way to prevent budget gimmicks is through a combination of sunlight and political will. Policymakers and the public must be aware when gimmicks are used and must be serious about true fiscal discipline.

At the same time, improvements to the budget process can help close loopholes exploited for gimmicks, shine sunlight on them, and nudge policymakers to make fiscally responsible choices.

As the nation begins to debate changes to the budget process, comprehensive reforms should be coupled with improvements to limit the use of budget gimmicks.

Assumption Gimmicks

Gimmick 1: Unrealistic Policy Assumptions

Description:

In drafting their respective budgets, both the President and Congress must put forward proposals as to how they would like federal funds to be raised and spent. These proposals are meant to reflect what budget drafters would like to enact into law – not necessarily what they will succeed at enacting into law. However, there is a line between putting forward an ambitious policy proposal and putting forward a completely unrealistic proposal.

Sometimes, budget authors will propose or assume policies they know can never actually be realized – often policies that they themselves don’t even support – in order to make their budget appear more fiscally responsible. Doing so is a clear budget gimmick.

Examples:

The President’s Fiscal Year (FY) 2019 budget includes a number of unrealistic policy assumptions. As one example, the budget assumes $1.5 trillion in cuts to non-defense discretionary spending despite the fact that Congress had passed and the President signed an agreement to raise discretionary spending, including non-defense discretionary spending, for 2018 and 2019. Given that every year it had been in place, the sequester-level cuts to discretionary spending have been raised and offset to varying degrees, it is unrealistic to assume cuts to discretionary spending of a significantly larger magnitude.

In addition, many past budgets of both parties used similar unrealistic assumptions – proposing only short-term "doc fixes" and Alternative Minimum Tax (AMT) patches, even though policymakers almost certainly intended to extend these politically-popular policies each year.

Solutions:

It is almost impossible to prevent administrations from making whatever policy assumptions they want in their budgets, regardless of whether the President stands by such proposals. However, the Congressional Budget Office’s (CBO) Analysis of the President’s Budget could shine light these gimmicks by showing alternate projections of the President’s budget that assume certain expirations or other changes do not occur.

Unrealistic policy assumptions could be curbed more easily in the congressional budget resolution by amending the Congressional Budget Act. One option would be to require that any savings in the budget resolution be included in reconciliation instructions – this would discourage lawmakers from claiming savings from policies they had no intention of enacting because reconciliation instructions lose privilege when they don’t achieve their minimum required savings.

If policymakers view the option above as too hard or restrictive, another alternative would be to split the budget resolution into an aspirational section that identifies a fiscal goal and an enforceable section that focuses on concrete policy changes that would move toward that goal. The requirement described above could apply to the enforceable section but not the aspirational one.

More Readings:

- All the President's Budget Gimmicks

- The FY 2018 House Budget and Budget Gimmicks

- The Better Budget Process Initiative: Strengthening the Budget Resolution

Gimmick 2: Rosy Economic Assumptions

Description:

Economic assumptions and projections underlie every budget put forward by the President and Congress – and in some cases the fiscal impact of legislation. These projections can be a deciding factor in whether or not a budget or bill meets a given fiscal goal. A 0.1 percent difference in Gross Domestic Product (GDP) growth can mean a roughly $300 billion difference in ten-year deficits and 2 percent of GDP difference in debt after a decade.

Because there is no requirement that Congress or the President use impartial economic projections, either can use their own “rosy economic assumptions” in their budget proposals that assume much stronger growth than is likely to be the case. Perhaps more troubling, Congress could direct the nonpartisan staff at CBO or the Joint Committee on Taxation (JCT) to make particular economic assumptions or to use specific models in generating their economic estimates.

By putting their thumb on the scale, however, policymakers can undermine the scorekeeping and estimating process and paint a fiscal picture out of line with reality. This could alleviate pressure to propose much-needed deficit reduction and increase the opportunity to propose new debt-financed spending or tax cuts.

Examples:

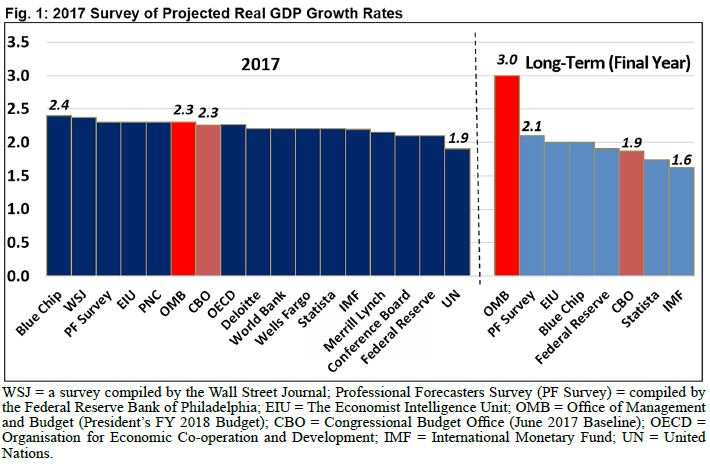

The President’s FY 2019 budget assumes growth rates massively higher than CBO or the mainstream consensus. Presidents’ budgets typically incorporate more optimistic economic assumptions than projected by the nonpartisan CBO or the Federal Reserve – in part because they incorporate the economic effect of policies in the budget – and these scenarios often result in a more favorable fiscal picture than is likely to be the case.

However, this year’s budget took that optimism to a new level. The President’s FY 2019 budget assumes the economy will grow by roughly 3 percent per year, adjusted for inflation. By comparison, most other estimators – including CBO, the Federal Reserve, and most outside forecasters – project that the economy is likely to grow by closer to 2 percent per year. As we’ve shown in prior analysis sustained 3 percent economic growth would be almost impossible given current demographics and certainly implausible enough to have no justification as a baseline projection.

Yet the President’s budget essentially carried over this rosy assumption from last year’s budget, when it was also far outside of the mainstream (see Fig. 1).

Importantly, the use of this gimmick allows the President to claim far less debt than is likely to be the case. While the FY 2019 budget projects debt held by the public will fall to 73 percent of GDP ($23.7 trillion) by 2028, we estimate debt will actually rise to 91 percent of GDP ($26.6 trillion) using more realistic economic assumptions like those from CBO (removing other gimmicks results in debt rising to 93 percent). In other words, rosy growth assumptions allows the budget to claim 18 percentage points of GDP, or almost $3 trillion, less in federal debt.

Solutions:

One way to prevent rosy economic projections would be to require the congressional budget resolution – and possibly the President’s budget – to rely on economic projections from CBO or another nonpartisan source like the Federal Reserve. Economic assumptions are used to allow for a common understanding when analyzing and debating policies in a budget; they are not themselves intended to be heavily debated as part of the budget conversation.

To account for economic benefits of various proposals, under this solution budgets could be allowed to include “additional dynamic costs/savings” as an explicit line-item in the budget. These estimates should be the result of rigorous macroeconomic and budget analysis, not arbitrary assumptions.

Assuming the President's Office of Management and Budget (OMB) is allowed to continue using its own assumptions, another solution could be to require the agency to present a comparison and cross-walk from its assumptions to CBO’s, along with a written justification of why they differ. There is no strong case for Congress to be allowed to pick its own economic assumptions rather than those from its own nonpartisan budget office (CBO).

In addition, Congress could create a point of order against legislation directing CBO to use different economic models or assumptions without an express request from the CBO director. Since CBO is the official scorekeeper for legislation, it should be allowed to use the methods and assumptions it believes are most appropriate.

More Readings:

- How Fast Can America Grow?

- Analysis of the President's FY 2019 Budget

- Debt Could Be 20 Percent of GDP Higher than President's Budget Claims

- All the President’s Budget Gimmicks

Gimmick 3: Magic Asterisks and Unspecified Savings

Description:

Ideally, Presidents' budgets should itemize and specify the details of each policy they put forward – and congressional budget resolutions should be able to back up their proposed budget numbers with real policies. Often, however, these budget proposals assume savings without policies to back them up. These unspecified budget savings are colloquially referred to as “magic asterisks.”

Savings levels a budget proposes in in each budget function (like defense, transportation, and education) should be backed up with specific policies that could legitimately be expected to produce those savings. All deficit reduction policies should ideally be fully accounted for with specific policy proposals. In areas where a complex, cross-cutting policy has not been fully fleshed out, offsets should be at least as detailed as (and preferably far more detailed than) the policies they are paying for.

Policies that are only broadly defined (but attached to specific savings) should be avoided when possible, but the most egregious “magic asterisks” are not attached to any broad policy at all. For example, budget resolutions often rely on undistributed cuts, which are unspecified cuts that are not assigned to any budget function. Undistributed cuts should be used only sparingly to reflect policies that may cut across multiple functions or legitimate rescissions, not as a mechanism to make the numbers add up without providing substance behind them.

Examples:

Of the $1.5 trillion of non-defense discretionary outlay cuts in President Trump’s FY 2019 budget, about $900 billion are unspecified. About $600 billion of savings in the budget come from assuming each non-defense agency would reduce non-defense discretionary (NDD) appropriations by increasing amounts each year, with near-term savings coming from a variety of concrete policies such as eliminating the Low Income Home Energy Assistance Program and the Community Development Block Grant and cutting spending within the Departments of Transportation and State as well as the Environmental Protection Agency. The other $900 billion in cuts were not even distributed by agency and instead achieved by assuming the NDD caps will decline by 2 percent per year below the prior year, even as inflation rises by a similar amount.

Magic asterisks were also used to a significant degree in President Obama’s FY 2012 budget. That budget assumed $328 billion of revenue from “bipartisan financing” of infrastructure without any detail or even broad explanation as to where those funds would come from. That same budget also assumed $315 billion of cuts from future offsets of Medicare "doc fixes" without any detail of what those offsets would look like.

Solutions:

Presidents’ budgets should avoid magic asterisks and unspecified savings unless it is truly implausible to put forward policy details in time (for example, in the case of a President’s first budget) – and when unspecified savings are relied upon the budget should put forward as much detail as possible and be conservative in its estimates. To keep the Administration accountable, CBO should continue its current practice of ignoring deficit-reduction estimates not backed up by policy.

With regards to congressional budget resolutions, policymakers could amend the Congressional Budget Act to require budget writers to assign all cuts to proper budget functions unless the policy is directly cross-cutting.

This can be further clarified by assigning cuts directly to authorizing committees for mandatory spending and the Appropriations Committee for discretionary spending. Even better would be to include specific reconciliation instructions to carry out mandatory changes. This could be done by amending the Congressional Budget Act to automatically create reconciliation instructions for deficit reduction contained in the budget resolution.

Alternatively, or additionally, budget resolutions could be allowed or required to propose scoreable policies to back up some or all of their spending and revenue level proposals. Currently, such policies are just supplemental and generally illustrative.

More Readings:

- All the President's Budget Gimmicks

- The FY 2018 Senate Budget and Budget Gimmicks

- The FY 2018 House Budget and Budget Gimmicks

Gimmick 4: Inflated Savings Estimates

Description:

While legislation is subject to official scores by CBO and JCT (for tax legislation), budgets are not subject to initial scoring by independent sources. Thus, congressional budget resolutions or a President’s budget can contain specific proposals that have unrealistically high estimates of the savings they may provide. These inflated savings estimates undermine the integrity of the proposal and budget and may just exist on paper to help a budget reach a particular fiscal target or offset another proposal.

Examples:

The President’s FY 2019 budget proposes to reduce improper payments and claims that doing so would save almost $140 billion over ten years, including nearly $60 billion in the tenth year. This would be the equivalent of reducing improper payments by about one-third, a target most experts think is far in excess of what is possible. Given the lack of specificity in how these reductions would be achieved, CBO scored a similar proposal last year with no savings. And they scored improper payment reductions in the prior year – proposed under President Obama – as saving only $2 billion by the final year. In other words, assuming such high levels of savings paints a misleading picture of what is likely.

The FY 2019 budget makes a similarly rosy assumption with regards to return-to-work efforts in the Social Security Disability Insurance and Supplemental Security Income programs. The budget suggests that spending $100 million per year on pilots and demonstrations in the first five years can yield $50 billion in savings in the second five years – there is no basis for this extensive amount of savings.

Solutions:

It would be a challenge to restrict OMB from claiming unrealistic amounts of savings if they so choose in their budget. However, CBO’s Analysis of the President’s Budget could be directed to create a line item of specific policies where they substantially disagree with the President's budget’s estimates of the savings.

Inflated savings estimates could be limited more easily in the congressional budget resolution by amending the Congressional Budget Act. One option would be to require any savings to be backed up with a CBO score of a specific policy that could achieve those savings. Another option would be to require that any savings in the budget resolution be included in reconciliation instructions, which would discourage lawmakers from claiming savings from policies they had no intention of enacting or do not reasonably think CBO would score in such a manner because reconciliation instructions lose privilege without achieving their minimum required savings.

CBO could also be directed to estimate or re-estimate the possible savings specified by certain polices in a congressional budget resolution.

More Reading:

- All the President's Budget Gimmicks

- Debt Could Be 20 Percent of GDP Higher than President's Budget Claims

Gimmick 5: Shopping for Estimates

Description:

In order to determine its compliance with budgetary rules and overall fiscal impact, legislation must be scored by CBO, often with the assistance of staff at JCT. CBO and JCT provide point estimates based on what they believe to be the center of a range of possible outcomes. These estimates are not perfect, but they are based on sophisticated modeling and, importantly, are unbiased.

Because CBO estimates are imperfect, policymakers will often supplement them with other estimates from outside estimators. There is nothing wrong with policymakers pointing to these estimates in making the case for their legislation, but they must recognize that there is only one official scorekeeper. Using an outside score instead of CBO is a budget gimmick – particularly if lawmakers cherry-pick only the most favorable estimate.

An especially egregious version of this gimmick involves Congress using this outside score for enforcement purposes. While CBO is Congress’s official scorekeeper, scores are technically provided by the Chair of the Budget Committee – this means the Chair has the power to use “directed scorekeeping” to incorporate estimates from an outside group for their assumptions. Doing so is a gimmick even if the Chair requires a score to be based on estimates from OMB, which, like CBO, is capable of sophisticated modeling but is not impartial and unbiased.

Examples:

While CBO is the official scorekeeper, the Chair of the Budget Committee technically has the right to select the official score. To use a score that is not from CBO, however, would be extraordinarily unusual. Yet, it has been proposed. For example, in July 2017, one senator suggested having the Department of Health and Human Services score an amendment to the Better Care Reconciliation Act if CBO could not produce a score quickly enough (or favorably enough). Similarly, some Members of Congress proposed using cost estimates from OMB instead of CBO during the health care debate in 2009. Most recently, some suggested using revenue estimates of tax bills from the Treasury Department or other outside groups that are more likely to estimate large dynamic responses from tax cuts than JCT and CBO.

Solutions:

Current law technically gives the Chair of the Budget Committee the authority to produce scores, even though the clear intent is for the Chair to rely on estimates from CBO and JCT. Codifying this intent and longstanding practice and requiring the Budget Committees to use a score independently produced by CBO under House and Senate rules would prevent lawmakers from shopping around for scores.

More Readings:

- CBO’s Analysis of the President’s FY 2018 Budget

- A Dangerous Effort to Undermine the Work of the Congressional Budget Office

- Is CBO's Math on the BCRA Wrong Because It Uses Faulty Numbers?

Manipulating the Budget Window

Gimmick 6: Arbitrary Phase-Ins

Description:

Legislation is currently scored over ten years, a budget window considered long enough to be able to understand the true effects of a policy but short enough to avoid massive forecasting errors. However, this use of this time window – or any window – allows for the possibility of abuse. One way to abuse the ten-year window is through an arbitrary phase-in of a policy change.

To be sure, there are plenty of justifiable reasons why lawmakers may want to phase in a policy gradually – but obscuring the full cost of legislation is not one of them.

Gradual phase-ins can limit the cost of a policy over a ten-year budget window without much affecting the long-term cost. A policy phased in linearly over a decade, for example, will cost only about half as much as if the same policy was implemented immediately; the annual long-term cost will be roughly identical. As a result, phase-ins can reduce reported costs – for offsetting, enforcement, and reporting reasons – without having much impact on the actual cost of legislation. Similarly, delaying a policy’s start date to late in the budget window also gives an inaccurate impression of its long-term costs.

Examples:

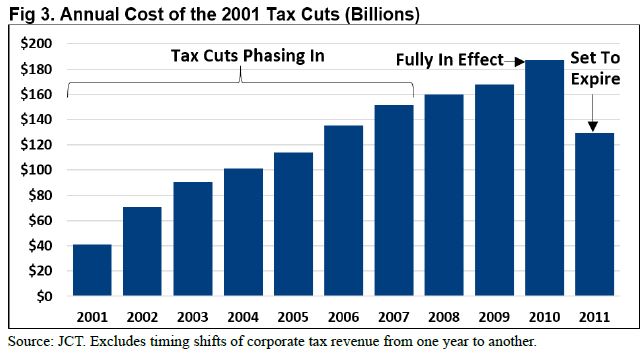

The 2001 tax cut legislation provides a clear example of using phase-ins to mask a proposal’s long-term costs. The legislation phased in reductions in marginal tax rates over five years, and also phased in a variety of other provisions over as long as nine years. As one particularly egregious example shows, the legislation called for a significant reduction in the estate tax to take place gradually between 2002 and 2007 – and then it eliminated the estate tax altogether in 2010.

There was little tax justification to any of the phase-ins in the 2001 tax legislation, but the budgetary effect was to keep the total ten-year cost of the legislation to under $1.35 trillion – despite costing nearly $190 billion per year in 2010. The estate tax portion alone cost only $138 billion over ten years despite two-fifths of the cost showing up in the tenth year ($54 billion in 2011).

Solutions:

While one cannot stop legislation from phasing policies in, process reforms can make it more difficult for such phase-ins to obscure the cost.

Requiring scorekeepers to provide more information on the long-term deficit impact of major legislation beyond the first ten years would discourage lawmakers from using phase-ins simply as a way to game the budget window. Alternatively scorekeepers could provide, if possible, a “steady state analysis” of the effect of a policy.

To limit the use of phase-ins to circumvent budget enforcement rules, Statutory Pay-As-You-Go (PAYGO) and Senate PAYGO rules could be amended to require legislation be fully offset over the second five-year period of the budget window; current law only requires legislation be offset over the first five- and ten-year periods (the former is often ignored, waived, or circumvented). An even stricter standard would be a “final year test,” wherein legislation could not increase the deficit in the tenth year of the budget window. This would deter the use of phase-in gimmicks because the costs of a policy would have to be fully offset regardless of whether or not it was phased in, at least in the first ten years.

More Readings:

- Better Budget Process Initiative: Improving Focus on the Long Term

- Beware of Budget Gimmicks in Health Care Reform

Gimmick 7: Front-Loading Costs, Back-Loading Savings

Description:

While there may be perfectly legitimate reasons for legislation to have upfront costs and savings that materialize later on in the budget window, excessive and unjustified use of back-loaded savings to pay for front-loaded costs can often be considered a budget gimmick.

Budget enforcement rules are designed to require new spending or tax cuts be fully offset with spending reductions or revenue increases. Front-loading costs while back-loading savings reduces the likelihood that offsets will ultimately materialize while leading to additional borrowing costs even if they do.

In some cases, lawmakers may schedule future offsets with the intention of reversing them later. More often, the reversal of future offsets is not the original intent, but nonetheless the consequence of back-loading savings.

Front-loaded costs also have the effect of increasing the cost of legislation further in the form of higher debt service. As an extreme example, a policy that that increases the deficit by $100 billion in 2018 and reduces the deficit by $100 billion in 2027 would result in $28 billion of higher interest payments, even though budget enforcement rules that don’t take interest into account would see the policy as deficit-neutral.

Examples:

A number of laws have accompanied near-term costs with back-loaded offsets with little justification for doing so. For example, the Bipartisan Budget Act of 2013, which provided near-term sequester relief, proposed that $47 billion of its $85 billion in offsets occur in the final two years of the ten-year budget window. One of these back-loaded offsets – an adjustment to military retirement benefits – was later repealed and replaced with an extension of the mandatory sequester – an even more back-loaded offset that many policymakers have subsequently proposed repealing.

The Affordable Care Act also back-loaded savings to some degree, with its largest Medicare cut (“productivity adjustments”) phasing in gradually and one of its major revenue sources (the “Cadillac tax” on high-cost health insurance plans) not beginning until the ninth year of the budget window.

Solutions:

One relatively simple solution to address this gimmick is to modify the definition of “budget effects” subject to Statutory PAYGO to include net interest costs (or savings) on the PAYGO scorecard and require CBO to include estimated changes in debt service costs in its cost estimate for legislation. While doing so wouldn’t prevent policymakers from excessively back-loading savings, it would require them to recognize the cost of doing so and offset any net cost that arises from including interest.

A more ambitious alternative that effectively gets to the same place would be to require legislation be scored using a “net present value” concept, which discounts future costs and savings.

PAYGO rules could also be strengthened to make it harder for lawmakers to waive or circumvent the five-year test and even adding/strengthening the one-year test, though there is a risk this change would prevent some intentional and non-arbitrary back-loading.

More Readings:

- The Better Budget Process Initiative: Strengthening Statutory Budget Enforcement

- Everything You Need to Know About Budget Gimmicks, in 8 Charts

Gimmick 8: Pushing Costs OUtside the Budget Window or Savings Inside the Window

Description:

Because legislation is generally scored over a ten-year budget window, policymakers may be able to shift costs to or savings from the eleventh year to make legislation appear cheaper over ten years.

These timing shifts are blatant gimmicks since the on-paper savings in the tenth year are immediately erased the following year, sometimes within days or weeks. Though statutory PAYGO rules prohibit spending delays or revenue accelerations involving the tenth and eleventh years from counting for PAYGO purposes, there still exist opportunities to game the system by shifting spending cuts from the eleventh to the tenth year.

Examples:

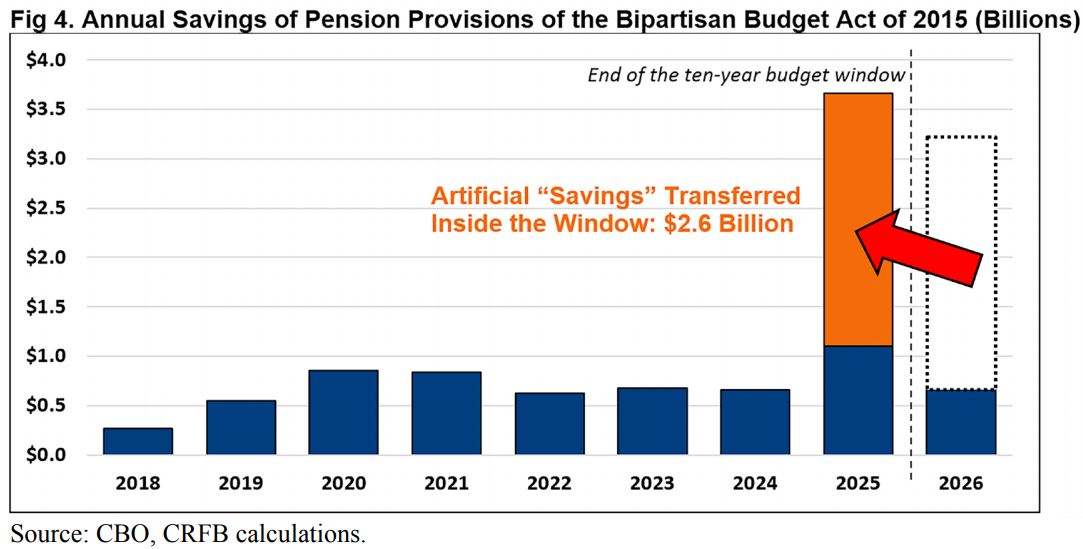

The Bipartisan Budget Act of 2015 used multiple timing gimmicks to offset the cost of increasing budget caps on discretionary spending. First, the law moved the due date for Pension Benefit Guaranty Corporation (PBGC) premiums in 2025 from October 2 to September 15, which shifted premium payments from FY 2026 (the eleventh year of the budget window) to FY 2025 (the tenth year). This policy produced $2.6 billion of “savings” that would be wiped out only a few days into FY 2026.

In addition, the legislation continued a policy that shifted Medicare sequester savings from the eleventh year into the tenth year. The legislation extended the sequester to 2025, which would normally apply to Medicare payments from February 1, 2025 to January 31, 2026. Four of those months are in FY 2026, which was outside the budget window at the time, but the legislation shifted all of the year’s cuts into the first six months, which are in FY 2025. This shift produced about $5 billion of “savings” in FY 2025, but those savings would be wiped out by February 2026.

Solutions:

To address this gimmick, lawmakers could broaden PAYGO rules against timing shifts to rule out any policy that shifts spending cuts from the eleventh to the tenth year. This would close the remaining loophole for blatant timing shifts.

In addition, lawmakers could codify the point of order against legislation that increases on-budget deficits by $5 billion or more in the three decades following the first decade. This rule already exists in the Senate, but it originated in a budget resolution and could be repealed in another budget resolution with a simple majority. The point of order should be strengthened by being codified in a law signed by the President and expanded to include the House. However, this enforcement mechanism may not prevent some timing shifts if they are less than $5 billion.

More Readings:

- Budget Deal Truly Offsets Only Half Its Cost

- Gimmick in Doc Fix Patch Should Be Replaced with Real Savings

Gimmick 9: Using Temporary Savings to Offset Permanent Costs

Description:

PAYGO rules and the Statutory PAYGO law require legislation to be offset over the budget window so that any tax cuts or mandatory spending increases are paid for with spending cuts and/or revenue increases. Because PAYGO generally operates over the first five and ten years, however, lawmakers may be able to enact permanent tax cuts or spending increases offset with temporary one-time savings.

While a package of permanent costs and temporary offsets wouldn’t increase the debt over ten years, it almost certainly would increase the long-term debt. Attempts to obscure this reality represent a clear budget gimmick.

Examples:

The Affordable Care Act claimed some of its savings from the CLASS Act, which would set up a new federal insurance program to finance long-term care. Because the program would start collecting premiums before it started paying out benefits, it was scored as saving $70 billion over a decade; however, these savings were temporary, and the program’s benefits would eventually overtake its premiums.

As another example, a 2014 House bill used temporary savings from delaying the individual mandate for five years to offset the cost of permanently repealing the Sustainable Growth Rate (SGR) formula for Medicare physician payments. The $159 billion of ten-year savings from a five-year delay of the individual mandate would have fully offset the $138 billion ten-year cost of the SGR replacement, but the legislation had a large net cost in the second five years and would have added significantly more to the debt in the subsequent years.

Solutions:

One way to restrict the use of temporary offsets for permanent costs is to add a second five-year test to PAYGO to ensure that bills meeting PAYGO rules in the first five years don’t violate them in the last five years of the ten-year window. Bills that use temporary savings to pay for permanent costs are more likely to violate the second five-year test, so the new test would help prevent this gimmick. The test would also have the advantage of not requiring any information not already provided in CBO estimates.

In addition, lawmakers could codify a point of order against legislation that increases spending or deficits by at least $5 billion over the three decades following the end of the budget window. This rule already exists in the Senate, but since it originated in a budget resolution it could be repealed in another budget resolution with a simple majority. The point of order would be strengthened by being codified in a law signed by the President and expanded to include the House. This would ensure that 60 votes are required in the Senate for bills that increase long-term deficits.

More Readings:

- House SGR Bill Increases Long-Term Deficits

- Gimmick, Responsible Budgeting, or Something in Between?

- The Better Budget Process Initiative: Improving Focus on the Long Term

Gimmick 10: Arbitrary Policy Sunsets

Description:

Generally, if a policy is intended to be permanent, lawmakers write it permanently into the law. For programs where ongoing review is desired, lawmakers sometimes pass a multi-year extension that ultimately expires but allow CBO to assume the program is permanent for budgetary purposes. Under proper budgeting principles, the only policies that should be enacted and scored as temporary are those intended to be in effect for a temporary period of time.

Unfortunately, lawmakers often violate these principles by establishing or extending policies on a temporary basis when they intend such policies to be permanent. Doing so can help reduce a policy’s reported ten-year cost or help legislation circumvent rules that prohibit long-term increases in debt (such as the "Byrd rule" for reconciliation bills in the Senate).

Unfortunately, once a policy is put in place the first time, lawmakers often use its existence as an excuse to continue it without offsets (the “current policy rationale”). The result is that temporary legislation often hides the "true cost" of what is being proposed and reduces the share of the policy that is ultimately offset.

Examples:

The recently passed Tax Cuts and Jobs Act contained a host of sunsetting individual income tax provisions. The Act’s lower marginal rates and changes to deductions, credits, and exemptions will sunset and revert to the old code by tax year 2026. The sunset was used to help keep the cost of the tax bill under $1.5 trillion dollars and prevent it from adding to long-term deficits. But policymakers have insisted that they have no intention of letting these provisions expire.

In 2014, the Senate passed a three-year proposal to expand veterans' benefits by allowing beneficiaries to seek out private (non-VA) health care paid for by the Department of Veterans Affairs. This proposal had large and growing costs that CBO estimated, if fully phased in, would cost $50 billion per year – more than doubling what was spent on VA health care. If the program was permanently extended and its fully phased-in costs grew with the economy, the total cost could exceed $500 billion over a decade before interest. This new healthcare entitlement proposal was limited to three years to limit the large and growing cost.

Solutions:

One solution to prevent arbitrary sunsets would be to instruct CBO to score temporary polices as permanent unless instructed to do otherwise. CBO already abides by this practice for certain spending programs (and a few taxes), but could be asked to do so on a more universal basis. Policies that are meant to be temporary – such as stimulus measures or disaster relief – could require acknowledgement as temporary in the legislative language and possibly signing statements by the President.

Importantly, CBO should only apply this practice to legislation going forward – if they applied it retroactively to existing legislation, some costs would never be realized.

A variation on this idea would be to create an official alternate baseline managed by CBO that assumes temporary policies are made permanent. This would apply to all tax and spending policies, not just the largest ones included in the Alternative Fiscal Scenario that CBO frequently produced in the past.

More Readings:

- The Better Budget Process Initiative: Setting the Benchmark: Reforms to Budget Baseline Rules

- Current Policy Gimmick Would Add Half a Trillion to Debt

- Senate Vets Bill Could Create New $500 Billion Entitlement Program

- Final Tax Bill Could End Up Costing $2.2 Trillion

- Five Gimmicks That May Hide the True Costs of Tax Reform

Gimmick 11: Back-Loading Costs Beyond the Ten-Year Window

Description:

While the ten-year window is meant to be long enough to give an indication of long-term costs, lawmakers can abuse it to enact legislation with significantly larger costs in the second decade than in the first. When this is done intentionally to obscure deficit impact or avoid offsets, it is a budget gimmick. Even if not intentional, legislation with substantial costs beyond the first decade can substantially worsen the nation’s long-term fiscal situation.

Examples:

In 2015, Congress debated ending temporary "doc fixes" to the sustainable growth rate for Medicare. When done on a yearly basis, these doc fixes were paid-for 98 percent of the time. The permanent doc fix bill, however, had significant costs that were not fully paid for. While the bill partially offset its substantial ten-year costs, savings from its offsets grew substantially slower than the costs of a long-term fix. As a result, the bill’s net cost of $140 billion in the first decade would swell to more than $500 billion over two decades. Picking offsets that would not keep up with growing costs obscured the long-term fiscal cost of the bill.

Solutions:

In order to prevent legislation from obscuring long-term costs, Congress could require CBO to provide second decade cost estimates when possible. This already exists in theory, having been included in prior budget resolutions, but it could be codified in the Congressional Budget Act and enforced with points of order, limiting the ability of Congress to take up bills needing long-term estimates until those estimates are available.

On the enforcement side, policymakers could codify the Senate point of order against bills that increase on-budget deficits by more than $5 billion in the three decades following the first ten years. This rule was created in a budget resolution and can be repealed in another budget resolution with a simple majority vote. Instead, lawmakers should codify the rule in a law signed by the President and extend the point of order to apply to the House as well.

In addition, lawmakers could allow reconciliation instructions to include long-term savings targets as well as the ten-year targets they normally include. This would allow the Budget Committees to bring some long-term budgetary discipline to the instructed committees.

More Readings:

- The Better Budget Process Initiative: Improving Focus on the Long Term

- SGR Bill Would Add $500 Billion to Long-Term Debt

- CBO's Latest Estimate of the Partial ACA Repeal

Gimmick 12: Changing the Ten-Year Budget Window to Evade Fiscal Responsibility

Description:

Generally, mandatory spending and revenue changes are measured over a ten-year budget window. In some cases, supplemental long-term estimates are also incorporated into scores or budgets – and these long-term estimates should be used more, not less – but these estimates do not supersede the ten-year ones.

However, policymakers could extend (or shrink) the budget window simply to evade current budget rules or norms. For example, policymakers could largely avoid the Byrd rule prohibition on increasing deficits beyond the budget window under reconciliation by extending the window to 20, 30, or even 100 years. They could also use longer windows to make legislation appear fully paid-for even if it adds to the debt for many years upfront.

Examples:

Recently, Congress passed the Tax Cuts and Jobs Act. While various budget rules require any reductions in taxes to be fully offset with other revenue increases or spending cuts, many advocates preferred legislation that cut taxes and added to the debt. In addition to violating Senate PAYGO rules, debt-financed tax reform might be unworkable through the fast-track “reconciliation” process, since the Byrd rule prohibits reconciliation from adding to the deficit in years beyond what the budget resolution covers.

To circumvent this rule, some had advocated extending the budget resolution from ten years to 20 or 30 years, which would enable a tax cut to last for 20 or 30 years before expiring to be Byrd-compliant. While this would not have achieved the permanence that most tax reform advocates desired, it would certainly come close: a decades-long budget window would ensure a stable tax code for a generation. But in doing so, it could massively increase the federal debt over the long term and effectively neuter the Byrd rule.

Solutions:

A number of options exist to restrict this gimmick without discouraging more long-term budgeting.

One option would be to codify and clarify that budget enforcement rules like PAYGO apply over the ten-year window, while revising long-term budget enforcement rules like the Byrd rule to apply after ten years, rather than after the budget resolution’s timeframe.

When it comes to reconciliation, Congress could also re-instate the “Conrad rule,” which prohibits reconciliation legislation from adding to the deficit during the budget resolution’s window as well.

Finally, Congress could codify the ten-year window for mandatory and revenue legislation, the President’s budget, and budget resolutions. Supplemental long-term scores and budget proposals should still be allowed and encouraged, but provided separately from ten-year estimates.

More Readings:

- The Better Budget Process Initiative: Improving Focus on the Long Term

- Five Gimmicks That May Hide the True Costs of Tax Reform

- Reconciliation 101

Gimmick 13: Counting Timing Shifts as Budgetary Savings

Description:

Some tax or spending policies with no net fiscal effect with still result in costs or revenues being shifted over time. While occasionally these shifts are intentionally egregious – for example, legislation that simply changes the date certain funds are spent or collected – timing shifts are often the natural result of a given policy change.

Unfortunately, policies with timing effects can have the effect of reducing deficits over the ten-year window even if they do not ultimately change deficits much at all. If this illusory deficit reduction is claimed as savings or used to offset other legislation, it is a clear timing gimmick.

Examples:

One common example of this gimmick is through the use of something called “pension smoothing,” which policymakers used in 2012, 2014, and 2015 to pay for highway and other spending.

The pension smoothing gimmick temporarily reduces the amount that companies must contribute to their pensions. Because pension contributions are tax-deductible, lower contributions mean more corporate tax revenue in the near term. However, whatever money companies do not contribute in the near term needs to be made up later, so the net effect on revenue is close to zero (and possibly negative if it puts more pensions in jeopardy).

For example, the pension smoothing passed in 2014 was projected to save $6.4 billion over ten years – all of which was used for a transfer to the Highway Trust Fund. In reality, it raised $19 billion in the first seven years but lost almost $13 billion in the following four, and would likely lose at least another $7 billion in the subsequent years. Timing gimmicks allow policymakers to claim savings in the budget window without fully accounting for the costs that come after.

Another example is related to the use of Roth-style retirement accounts. While traditional tax-preferred retirement accounts allow tax-free contributions that are taxed upon withdrawal, Roth-style accounts allow for post-tax contributions that are tax-free upon withdrawal. Any expansion or move toward Roth accounts, therefore, reduces near-term deficits but worsens long-term deficits.

Solutions:

To restrict this gimmick, Congress could amend statutory PAYGO and other enforcement rules to exclude any savings from provisions that are projected to significantly increase deficits beyond the ten-year window. This would prevent shifts in the budget window to attempt to capture temporary savers or timing shifts.

Lawmakers could also codify in the Congressional Budget Act the Senate point of order against bills that increase on-budget deficits by more than $5 billion in the three decades following the first ten years.

Additionally, the House and Senate could also establish points of order against counting savings from provisions that CBO believes would result in zero or negative deficit reduction over an extended period of time.

More generally, expanding long-term budgeting – in budget estimating, reconciliation instructions, PAYGO rules, and other places – would make these timing gimmicks more difficult to enact and easier to expose.

More Readings:

- Pension Smoothing Does Not Reduce the Deficit

- Don't Use a Gimmick to Fund Our Highways

- The Better Budget Process Initiative: Strengthening Statutory Budget Enforcement

- The Better Budget Process Initiative: Improving Focus on the Long Term

Discretionary Spending Gimmicks

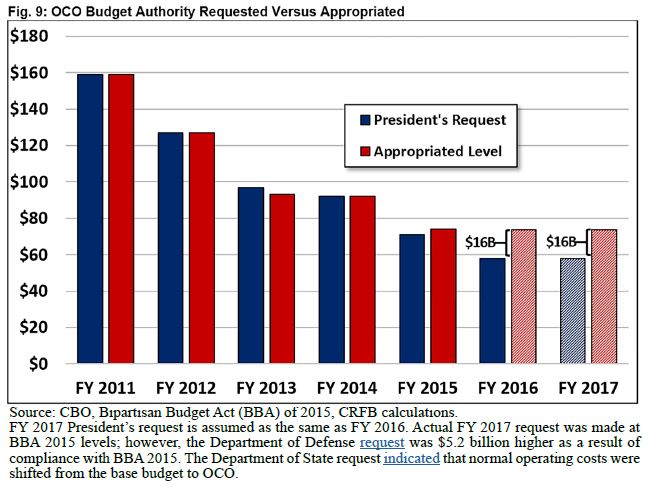

Gimmick 14: Using OCO to Circumvent Discretionary Spending Caps

Description:

Overseas Contingency Operations (OCO) is a designation of discretionary spending that applies to “war spending” for the wars in Iraq and Afghanistan and related activities. Unlike most defense and non-defense discretionary spending, this category is uncapped and not subject to the budgetary restraints put in place by the Budget Control Act of 2011. Because there are no formal criteria for what can be designated as OCO funding, the lack of a cap to this category creates an incentive for Congress or the President to include activities not related to war operations under this banner to avoid spending limits. By using a war spending account as a slush fund, policymakers circumvent the discretionary budget caps that are intended to constrain ordinary non-war non-emergency spending.

Examples:

For several years, lawmakers have designated some funds as OCO that were actually being used to fund base defense operations. The Bipartisan Budget Act of 2015 took this gimmick further by explicitly appropriating over $16 billion per year of OCO funds that were meant to finance ordinary defense and non-defense government operations (on top of other funds that backfilled the defense budget less explicitly).

Specifically, in the 2015 Bipartisan Budget Act both parties agreed to lift defense- and non-defense caps by $25 billion each for FY 2016, while also appropriating $16 billion of OCO funds above the President’s (already inflated) war spending request and splitting the funds between defense and non-defense. Whereas the explicit cap increases were offset (on paper), the OCO increases were deficit-financed. This was a clear and intentional effort to get around the statutory discretionary spending caps without offsetting the cost.

Solutions:

OCO spending is intentionally uncapped to allow Congress to spend what is needed on the wars abroad. Short of eliminating the special OCO designation, it may not be possible to fully end the use of this gimmick; however, its use could be limited in a number of ways.

One option is to create and codify a strict definition of what may count as OCO spending. Both the President (or OMB director) and Congress (or Budget Committee Chairs and Ranking Members) could be required to certify this criteria is met or identify which OCO-designated funds do not meet the criteria.

A second option would be to place a separate discretionary cap on OCO spending in order to end its uncapped nature. The cap could be set legislatively to reflect a reasonable war drawdown, or it could be based on requested levels from the President. Additional war spending needs could be financed by raising the OCO caps and offsetting the cost.

These options could be adopted separately or together.

More Readings:

- The Better Budget Process Initiative: Strengthening Statutory Budget Enforcement

- War Spending in the Omnibus Bill

- Limiting War Spending to Strengthen Budget Enforcement

- A New War Spending Gimmick In The Budget Deal

Gimmick 15: Counting Planned War Spending Reductions as Savings

Description:

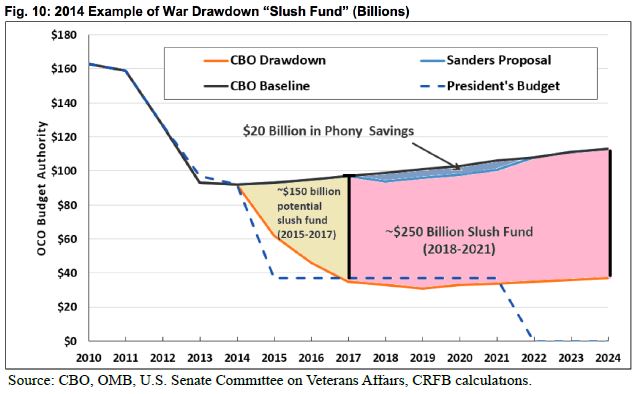

Because the Overseas Contingency Operations (OCO) designation is for war spending and is not capped, CBO’s budget projections follow the convention of assuming OCO costs grow with inflation in future years, regardless of current policy or future plans.

One oft-discussed gimmick is to limit future OCO spending to reflect a policy of continued troop drawdown and count the difference between these caps and the CBO baseline as savings. Worse still, some have tried to use these phantom savings to pay for other priorities. While PAYGO principles allow reductions in planned spending to pay for new policies, they don’t allow policymakers to take credit for reductions already occurring absent a new law. Using this quirk in the CBO baseline would increase spending without actually offsetting the new cost.

Examples:

This OCO gimmick has become less popular in recent years as baseline OCO spending had declined and lawmakers have used OCO more as a way to circumvent caps on other discretionary spending (as detailed above). However, it was commonly proposed just a few years ago.

For example, a 2014 proposal to replace the Medicare Sustainable Growth Rate (SGR) formula for physician payments claimed to finance the bill’s roughly $140 billion cost by capping war spending between 2016 and 2021. As another example, a 2014 Senate bill that would have increased veterans’ retirement and health benefits by $5.5 billion was offset with $5 billion per year of “reductions” in baseline OCO spending between 2018 and 2021. CBO made it clear that with regards to the war drawdown, such savings “might simply reflect policy decisions that have already been made and that would be realized even without such funding constraints.”

Solutions:

Under current law, reductions in discretionary spending levels technically cannot be used to pay for new mandatory spending or revenue. However, lawmakers often waive this rule – justifiably – in order to allow for trade-offs between discretionary and mandatory spending. To ensure that only true reductions in discretionary spending are counted, one option is to require CBO to use a different baseline for war spending – one reflective of current military plans rather than a simple inflation adjustment.

Another option would be to clarify in rules or in statute that no changes in OCO spending can be counted as savings or offsets under any circumstances.

More Readings:

- Democratic SGR Offset Alternative Replaces One Gimmick With Another

- Sanders Bill Would Add to the Debt, Create a $250 Billion Slush Fund

- OCO Gimmick Makes an Unwanted (and Unnecessary) Comeback

Gimmick 16: Phantom Savings from Reducing Uncapped Discretionary Spending

Description:

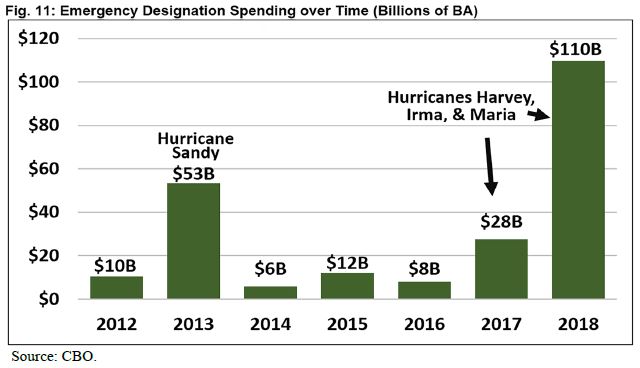

Currently, CBO assumes most uncapped discretionary spending will grow each year with inflation – even though appropriations are made only one year at a time. When this practice is applied to temporary or one-time appropriations such as emergency spending, it opens the door for possible abuse.

Lawmakers could claim significant savings compared to the baseline from simply creating a cap on this temporary spending. If savings from capping future temporary spending were to be used as an offset, it would be a budget gimmick because temporary spending in one year by definition should not affect future years. This gimmick could ultimately be unsustainable because emergency needs vary from year to year, and a cap would not stop lawmakers from appropriating in case of an emergency.

Examples:

In 2012 (for FY 2013), lawmakers appropriated $41 billion of disaster relief spending in the aftermath of Hurricane Sandy. Though this spending was a one-time occurrence, it was incorporated into CBO’s budget projections for every year going forward. This provided the opportunity for lawmakers to claim $302 billion of savings over ten years by simply removing that disaster spending from future years’ appropriations. Ultimately, lawmakers did not use these savings, and the opportunity to use them went away once the next year’s appropriations were made without a similar amount of disaster relief.

Solutions:

Lawmakers should make clear that reductions in uncapped discretionary spending do not count as savings.

In the case of disaster funding, perhaps the most straightforward option is to instruct CBO to assume appropriations are temporary and are not continued (with an inflation adjustment) year after year.

Lawmakers should also consider broader reforms in the way they budget for and finance disaster and emergency spending, independent from a hunt for offsets.

More Readings:

- A Mini-Bargain to Improve the Budget Updated for Disaster Relief

- The Peterson-Pew Commission on Budget Reform: Budgeting for Emergencies

Gimmick 17: Counting Savings from Extending Discretionary Spending Caps

Description:

The Budget Control Act’s discretionary spending caps technically end after FY 2021. At that time, discretionary spending levels can be set yearly without any legal limits. However, CBO’s baseline still projects FY 2022’s base discretionary spending at 2021 levels, adjusted for inflation per CBO conventions.

Congress should extend the discretionary spending caps beyond 2021 to prevent limitless discretionary spending. However, claiming savings from this extension would be a gimmick unless the extension were to be below the CBO baseline (and it would need to be realistically achievable – which is unlikely to be the case given recent legislation, especially if a reduction is paired with near-term cap increases).

In extending spending caps, policymakers would need to choose whether to set them at, above, or below current law levels. If set above current law, this cap extension would actually represent a spending increase relative to the CBO baseline.

Examples:

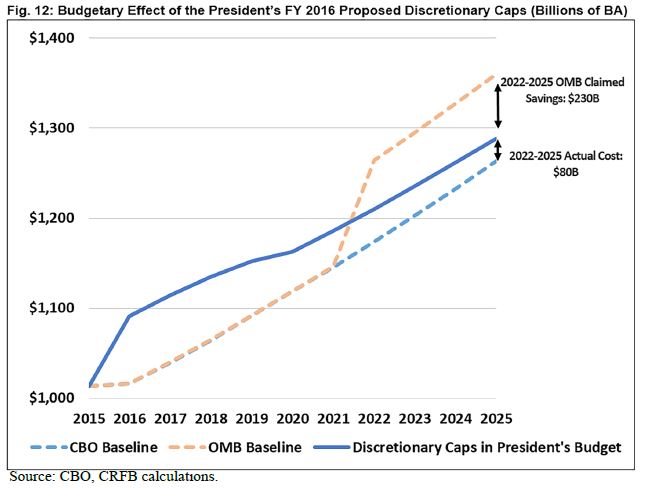

President Obama’s FY 2016 budget claimed savings from modified extensions of the discretionary caps by comparing them to the pre-sequester discretionary baseline after 2021.

By using a higher baseline for discretionary spending, the budget was able to claim savings of $230 billion from 2022 to 2025; by contrast, it increased spending by about $80 billion compared to CBO’s current law baseline.

Solution:

The discretionary spending caps were established to control spending, and they were lowered because of the sequester. CBO’s baseline convention requires them to set the post-2021 discretionary baseline at the 2021 levels. To avoid abuse, policymakers could mandate that the President’s budget and congressional budget resolutions compare their policy proposals to CBO’s baseline.

In addition, Congress should cap discretionary spending for 2022 through the end of the budget window without claiming it as an offset to prevent opening up extra “savings” if the 2021 cap is increased.

More Reading:

Gimmick 18: Phony Changes in Mandatory Programs (CHIMPs)

Description:

Changes in Mandatory Programs (CHIMPs) allow policymakers to reduce mandatory spending in an appropriations bill in order to finance an increase in discretionary spending. While there is technically nothing wrong with this, most CHIMPs are actually fake cuts in mandatory spending used to finance real increases in discretionary spending.

One way policymakers abuse CHIMPs is by rescinding mandatory budget authority that would not have actually been spent – sometimes called empty Budget Authority, or “empty BA.” Cuts in empty BA result in no actual reduction in outlays, but because cutting BA constitutes a CHIMP, it results in real discretionary spending increases.

A more egregious gimmick involves delaying mandatory spending from one fiscal year to the next and then taking credit for the “cut” in year one, ignoring the equal-sized cost in year two.

In both instances, the phony on-paper savings are then used to “offset” appropriations above the normal spending allocations, resulting in an increase in spending without any real offsets to pay for it.

Examples:

The CHIMP gimmick is often used in appropriations bills, most recently in the FY 2017 omnibus appropriations bill passed in May 2017. About $20.4 billion of net CHIMPs were in the bill, but only about $1 billion represented actual savings – allowing lawmakers to raise spending by $19 billion without having to pay for it. Of the other $19 billion, roughly half was empty BA, and the other half was delayed spending. Much of the savings came from shifting $8 billion in BA for the Crime Victims Fund from 2017 to 2018, resulting in no actual outlay savings but allowing for $8 billion of new discretionary spending.

Solutions:

One way to prevent policymakers from counting delayed spending as CHIMP savings would be to limit single-year CHIMP savings to the ultimate long-term savings of a given policy change (the ten-year cost could provide a reasonable approximation). To limit the use of empty BA, CHIMP savings could be limited to ten-year outlay savings or perhaps 110 percent of those savings to account for the fact that not all discretionary BA is spent.

A more blunt option, which has received support recently, could be to increasingly limit the total amount of CHIMP savings that can be used in a given appropriations bill. Ideally, such a limit would ultimately be reduced to $0, though it could be phased down gradually.

Another alternative would be to prohibit the use of savings from BA rescissions that result in no (or practically no) net outlay savings.

More Readings:

- Senate Budget Takes Issue With CHIMPS

- CRFB Explainer: Gimmicks in the FY 17 Omnibus Bill

- Better Budget Process Initiative: Strengthening Statutory Budget Enforcement 2015

Other Gimmicks

Gimmick 19: Double Counting Trust Fund Improvements

Description:

While most tax revenue funds general operations and most spending is financed from general revenue, the federal government finances several major and minor programs through trust funds with dedicated revenue sources. The most well-known of these include the Social Security trust funds (funded by payroll taxes), the Medicare Hospital Insurance (HI) trust fund (funded by payroll taxes), and the highway trust funds (funded by gas taxes). A reduction in trust fund spending or increase in trust fund revenue can strengthen the solvency of these and other trust funds and can also reduce unified budget deficits, which are measured without regard to trust fund accounting.

However, lawmakers often try to use trust fund savings or revenue to finance non-trust-fund spending or tax cuts – and do so without transferring money from trust funds to general revenue. Counting this same money twice – both to strengthen a trust fund and to offset new costs – is a gimmick that should not be allowed where trust fund accounting is relied upon. Similarly, transferring money into a trust fund while also using it to offset other costs is also a form of double counting.

Examples:

One well-known example of double counting took place in the Affordable Care Act (ACA). Among the pay-fors included in the ACA was a new Medicare surtax on wages over $200,000 as well as a number of spending reductions within the Medicare HI program. These changes improved the solvency and extended the life of the HI trust fund; at the same time, they were counted as offsets to new spending.

Another example comes from the proposed Tax Reform Act of 2014, which would have raised $127 billion in direct revenue from a one-time tax on income held abroad and simultaneously used that revenue to help finance the rest of the bill while transferring the same amount into the Highway Trust Fund.

Solutions:

One way to prevent double counting of trust fund money is to exclude changes to trust fund balances from scorekeeping for enforcement purposes and count transfers into or out of trust funds as costs or savings. Thus, paying for general tax or spending changes with trust fund savings would require transferring money out of the trust fund, and paying to shore up a trust fund with general savings would prevent that savings from offsetting other costs.

Another option would be to modify CBO’s budget baseline to reflect that a trust fund’s spending is limited to its available assets. At least over the long run, this would ensure that trust fund savings for financially-troubled trust funds would go to trust fund spending and not to other purposes.

More Readings:

- The Affordable Care Act and the HI Trust Fund

- Double Counting: The Tax Reform Act and the Highway Trust Fund

Gimmick 20: Directed Scorekeeping

Description:

As a matter of convention, most legislation must be scored (or determined to be non-scoreable) by CBO. However, it is technically the Budget Committees that decide what scores are used (or not used) to estimate and enforce budget rules against legislation.

The Budget Committees therefore have the power to direct CBO to change the way they score certain legislation relative to CBO’s practice for Congressional scorekeeping purposes. In the most extreme version, the Committees may be able to simply produce their own score. But far short of that, they can use their power to manipulate the score put forward by CBO.

Examples:

In 2000, the Budget Committees directed CBO to approximate OMB’s methods for estimates of a variety of programs but most notably for defense. The directed scorekeeping lowered the score of appropriations by $3 billion in budget authority and about $19 billion in outlays compared to CBO’s preferred method. This particular example allowed for defense spending to be higher than it otherwise would have been. The direction did not change CBO’s baseline nor its estimates for sequestration.

Solutions:

To limit directed scorekeeping, Congress could amend the Congressional Budget Act to make CBO’s scorekeeping authority and autonomy more clear. They could also establish a point of order against legislation that makes such directions, including specific language declaring something unscoreable. This would provide another on-record vote to bring attention to the use of this gimmick.

Congress could also include language in the Congressional Budget Act and the Statutory PAYGO Act explicitly clarifying that estimates for enforcing the respective laws are based on existing scorekeeping rules. As a result, even if directed scoring were used, it would not affect existing points of order and rules in the Congressional Budget Act nor would if affect proper enforcement of Statutory PAYGO.

Congress should codify in the Congressional Budget Act that scorekeepers should make good faith attempts to score provisions even if Congress directs that a score will be unenforced, negated, or not scored. Scorekeepers should produce a public score even if Congress chooses to ignore it, and any changes to scorekeeping methods should be done in a nonpartisan, fact-based way that has input from both academics and the scorekeepers themselves.

More Readings:

- A Short Primer on the Congressional Budget Office

- Is CBO's Math on the BCRA Wrong Because It Uses Faulty Numbers?

Conclusion

The United States faces serious fiscal and economic challenges. Recognizing our unsustainable fiscal situation, Congress and the President must adhere to strict rules of budget discipline while also putting forward budgets and legislation to stabilize and reduce our debt as a share of GDP. However, budget discipline and deficit reduction on paper mean very little if done through games that do not allow it to materialize in reality.

The flagrant and pervasive use of budget gimmicks weakens budget discipline and increases debt levels, creating serious economic damage. Moreover, gimmicks undermine trust in the transparency and effectiveness of our political system, damaging representative democracy itself.

Budget process reforms are sorely needed to make gimmicks more transparent, more difficult to use, less harmful, and ultimately far less frequent.

Such reforms can complement – but not replace – the political courage and will that is ultimately needed from our leaders in Washington.

We dedicate this paper to our colleague Ed Lorenzen, who tragically passed away this January. A former House "budget cop," Ed was one of the nation's strongest advocates for budget discipline and spent much of his career fighting against gimmicks, games, and other budget workarounds. Most of the solutions presented in this paper were based on Ed's ideas. We miss Ed very much.