CBO’s Analysis of the President’s FY 2018 Budget

The Congressional Budget Office (CBO) released its estimate of the President’s Fiscal Year (FY) 2018 budget, using its own assumptions to evaluate the budget’s policies. While the President’s budget claims to achieve balance and reduce debt to below 60 percent of Gross Domestic Product (GDP) after a decade, CBO’s analysis finds that these claims are based on a number of overly aggressive and unrealistic assumptions.

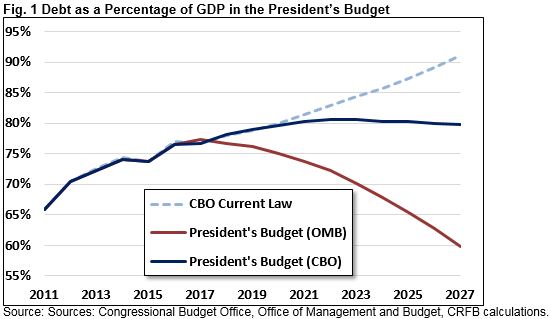

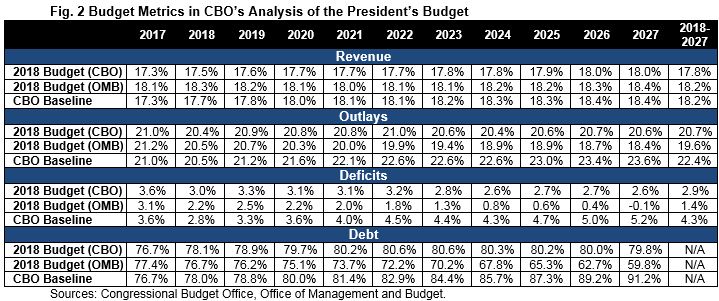

Using more realistic economic assumptions and independently evaluating the President’s policies, CBO finds the President’s budget will result in $3.8 trillion more debt than the President’s own estimate and save $3.3 trillion relative to our current path. As a result, CBO projects under the President’s budget debt as a share of GDP would rise from 77 percent in 2017 to 80 percent by 2027, and deficits would decline from 3.6 percent of GDP ($693 billion) in 2017 to 2.6 percent ($720 billion) in 2027.

Other major findings from CBO’s estimates include:

- Deficits would total $6.8 trillion from 2018-2027 under the President’s budget, which is $3.7 trillion above the Office of Management and Budget’s (OMB) estimate and $3.3 trillion below current law.

- The President’s budget would reduce revenue by $894 billion and spending by $4.2 trillion relative to current law, with the largest spending cuts coming from non-defense discretionary spending and health care.

- CBO estimates that debt would be 80 percent of GDP in 2027, 20 percentage points higher than OMB’s estimate of 60 percent. 18 percentage points of this difference can be explained by the fact that OMB ultimately assumes 3 percent annual economic growth despite nearly all public and private estimates suggesting growth rates much closer to CBO’s 1.9 percent.

The President deserves credit for putting forward $3.3 trillion of deficit reduction in his budget. It is worth noting however that CBO’s estimates incorporate $1.5 trillion of unspecified savings from Medicaid and discretionary spending. They also do not account for a potentially costly tax plan, since the President’s tax plan is not included in his budget (other than through several vague bullet points).

Overall, CBO’s estimate shows that after adjusting for extremely rosy assumptions, and even after incorporating deep unspecified spending cuts, the President’s budget would fall well far short of balance, allow debt to rise from today’s levels, but nonetheless, reduce the debt significantly relative to current law. Still debt would remain on an unsustainable path and CBO’s report makes clear that without serious tax and entitlement reform – including significant changes to Social Security and Medicare – it will not be possible to truly put debt on a sustainable path.

Spending, Revenue, Deficits, and Debt under the President’s Budget

CBO estimates that over the next ten years under the President’s budget, debt would rise modestly as a share of the economy from today’s post-war era record-high levels. Specifically, debt would rise from 77 percent of GDP this year to a high of 81 percent by 2022 before falling to 80 percent by 2027. These projections represent a significant improvement over CBO’s current law baseline, which estimates debt at 91 percent of GDP by 2027, but they are much worse than OMB’s estimate of the budget, which had debt at 60 percent in 2027.

CBO’s numbers assume the President’s nearly $1.5 trillion of unspecified spending cuts, mainly from non-defense discretionary spending and Medicaid. Without them, debt would rise to roughly 85 percent of GDP by 2027.

With these assumptions, CBO finds that deficits will total $6.8 trillion (2.9 percent of GDP) for 2018-2027, $3.3 trillion below current law but $3.7 trillion higher than OMB projections.

CBO projects deficits will be roughly stable over the next five years, hovering around 3 percent of GDP, before falling to 2.6 percent, or $720 billion, by 2027. The 2027 deficit is a clear improvement over the 5.2 percent of GDP deficit under current law but only halfway to the Administration’s estimate that they would balance the budget by that year.

Spending cuts in the President’s budget drive falling deficits late in the decade. As a share of GDP, CBO estimates the budget would stabilize spending at about 21 percent (20.6 percent in 2027) while allowing revenue to rise from 17.3 percent in 2017 to 18 percent by 2027, slightly below the current law projection of 18.4 percent. These totals do not include the President’s tax plan, which has not been detailed but could be quite costly based on available information.

Both spending and revenue under the President’s budget would be slightly above their historical averages. Spending would average 20.7 percent of GDP over the next ten years, compared to 20.3 percent over the previous 50 years. Revenue would average 17.8 percent of GDP over the next decade, compared to 17.4 percent over the previous 50 years. Both spending and revenue would be below current law projected levels of 22.4 and 18.2 percent over the next decade, respectively.

CBO also estimates that the President’s budget would increase economic growth by 0.1 percentage points (from 1.8 to 1.9 percent) on average over the next decade. This extra growth would reduce deficits by $161 billion over ten years and reduce the debt-to-GDP ratio by less than 1 percent in 2027. CBO states that the growth is due to the budget’s deficit reduction; other proposals that could affect growth are not specific enough for CBO to evaluate.

Policy Changes in the President’s Budget

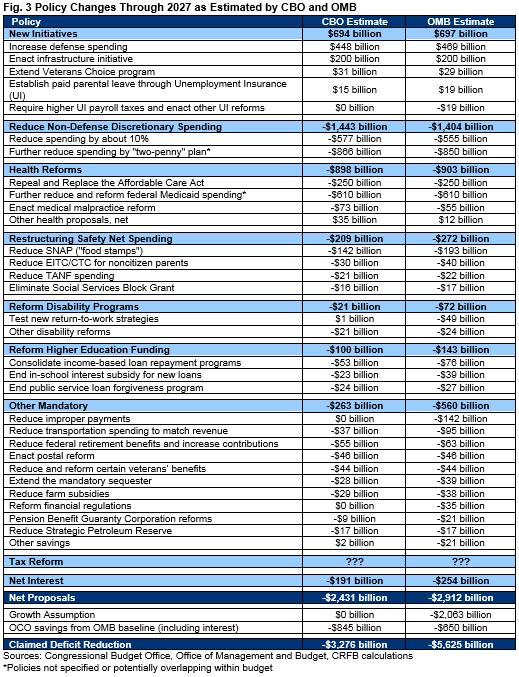

Although the President’s budget falls short of putting the debt on a sustainable path, it does incorporate significant deficit reduction, including a number of thoughtful spending cuts.

CBO estimates the budget would reduce deficits by $2.4 trillion relative to current law, excluding another $845 billion of savings from the war drawdown. That compares to OMB’s estimate of $2.9 trillion in deficit reduction (and another $2.1 trillion OMB estimated as a result of faster economic growth).

However, of this $2.4 trillion in deficit reduction, nearly $1.5 trillion comes from unspecified non-defense discretionary reductions and unspecified Medicaid savings that may partially overlap with other policies in the budget. Another $191 billion is net interest savings. That leaves nearly $800 billion of specified primary deficit reduction.

With regards various policy proposals in the President’s budget, the biggest differences between CBO and OMB’s estimates come from CBO disregarding unspecified savings from improper payments, reforming financial regulations, and Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) remain-at-work and return-to-work pilot projects, which accounted for a combined $223 billion in OMB’s estimate. For these proposals, the Administration did not provide enough detail to show how the changes would be achieved or if they even needed a change in legislation. (Note that properly designed SSDI and SSI reforms to support and encourage work can ultimately lead to significant savings, but substantial savings will take a number of years to materialize and will not begin to accrue until pilot programs are implemented broadly).

In addition, CBO estimates lower savings from the budget’s reform of the Supplemental Nutrition Assistance Program ($51 billion difference), consolidation of income-based repayment plans for student loans ($23 billion), Unemployment Insurance reforms ($19 billion), and Pension Benefit Guaranty Corporation changes ($12 billion). On the other hand, it finds $39 billion greater savings from the budget’s changes to discretionary spending and $18 billion greater savings from medical malpractice reform.

CBO does not count any of the $2.1 trillion of savings that OMB estimated for the implausibly large boost to economic growth it anticipated from the budget’s policies. In general, CBO uses its own economic assumptions to evaluate the President’s budget and does not take into account any added growth from the President’s policies. As mentioned above, however, CBO did include a separate analysis showing how the deficit reduction in the President’s budget would affect the economy. It found that deficit reduction would make the economy about 0.7 percent larger in 2027, resulting in an additional $160 billion of deficit reduction and reducing debt by 1 percentage point, down to 79 percent of GDP in 2027.

Differences Between CBO and OMB Estimates

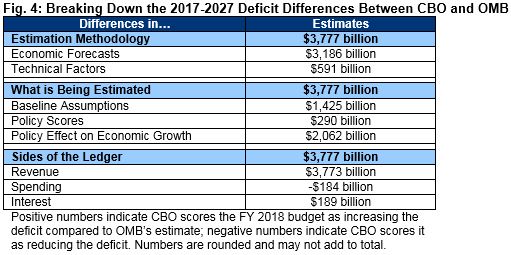

In total, CBO finds much higher deficits and debt in both nominal dollars and as a percent of GDP than OMB estimated. CBO estimates that deficits from 2017 through 2027 are $3.8 trillion higher than the President’s budget, and debt is 20 percent of GDP higher by 2027.

As mentioned above, the vast majority of the difference arises from different economic assumptions used by each agency. OMB’s much rosier and more implausible economic projections show economic growth that is 1.1 percentage points higher on average than CBO over the next decade, and an economy that is 11 percent larger by 2027. Those differences account for $3.2 trillion (84 percent) of the differences in the 2017-2027 total deficit. The remainder is due to technical differences in projections of federal programs and revenue sources.

OMB’s higher growth estimates also mean that the same dollar amount of debt appears lower as a share of GDP. For example, if OMB’s dollar amount of debt was measured with CBO’s baseline growth projections, debt would have been 66 percent of GDP instead of 60 percent in 2027.

Another way to understand the difference between CBO and OMB’s estimates is to determine how much is attributable to estimates of policy changes versus how much is attributable to differences in baseline projections prior to policy action. By our estimate, $1.4 trillion of the difference in 2017-2027 deficits is due to baseline projections, while $2.4 trillion is due to differences in either policy scores ($290 billion) or the growth that OMB predicted would arise from the policies ($2.1 trillion).

Finally, one can understand the differences by looking at them by budget category. CBO estimates that the budget will have $3.8 trillion of lower revenue, $184 billion lower primary spending, and $189 billion of higher interest spending over the 2017-2027 period than OMB’s estimates.

Conclusion

CBO’s analysis shows that after removing unrealistic economic and policy assumptions, the President’s budget would lead to debt rising slightly rising rather than falling precipitously as OMB projected, and a deficit in 2027 of $720 billion instead of a slight surplus. CBO’s estimate also incorporates large, unspecified savings, and omits any details on the President’s potentially costly tax plan.

Indeed, even after rosy economic assumptions are removed, CBO’s estimate still shows the President’s budget does include significant deficit reduction, and many of the spending cuts in the budget represent thoughtful improvements that deserve to be part of the legislative discussion.

Yet these savings are not nearly enough to fix the nation’s fiscal situation. The budget largely walls off the three largest spending programs – Social Security, Medicare, and defense – from any reductions. Even deep cuts to the rest of the budget are unlikely to result in sufficient savings to put the debt on a downward path, let alone balance the budget.

To grow the economy and put debt on a sustainable fiscal path, policymakers should combine many of the spending cuts in the President’s budget with significant reforms to slow the rapid growth of Social Security and Medicare, and reform the tax code to promote growth and generate more, not less, revenue.

Overall, CBO shows that when using realistic economic assumptions, the budget does not go far enough to put debt on a sustainable path. The Administration should widen the scope of its deficit reduction efforts.