Current Policy Gimmick Would Add Half-Trillion to Debt

Some tax cutters would like tax reform to embrace a troubling budget gimmick: a current policy baseline. Congressional leaders have set a revenue-neutral target for tax reform, which would be raising as much money as the current tax code. However, "current policy" would modify the baseline in order to redefine a tax cut as “neutral."

The House Republican Better Way blueprint “envisions tax reform that is revenue neutral,” but it is only revenue neutral relative to a current policy baseline, which is actually a tax cut of $462 billion compared to how legislation is traditionally scored.

The Congressional Budget Office's (CBO) current law baseline uses longstanding budget rules, generally assuming laws are unchanged. That baseline shows total revenues are projected to be $43 trillion over the next ten years. That current law revenue projection was reduced significantly by the 2015 tax extenders deal, which cost $680 billion over ten years and permanently extended several tax breaks while temporarily extending others. But the baseline for determining revenue neutrality may be reduced even further by assuming some of those tax breaks are extended even before they are.

The “current policy” baseline assumes all of the expiring tax breaks are permanently extended. In particular, the baseline suggested in the Better Way plan would assume bonus depreciation – which is scheduled to be reduced from 50 percent today to 30 percent by 2019 and then expire – would continue at 50 percent, and other expired and expiring tax provisions would continue indefinitely. Assuming these tax breaks continue instead of expire would lower the revenue baseline by $462 billion over ten years. With interest, switching to a current policy baseline would add $539 billion to debt.

The use of a current policy baseline is troubling for several reasons, essentially saying tax reform will reduce revenue, but by no more than this future set of tax cuts.

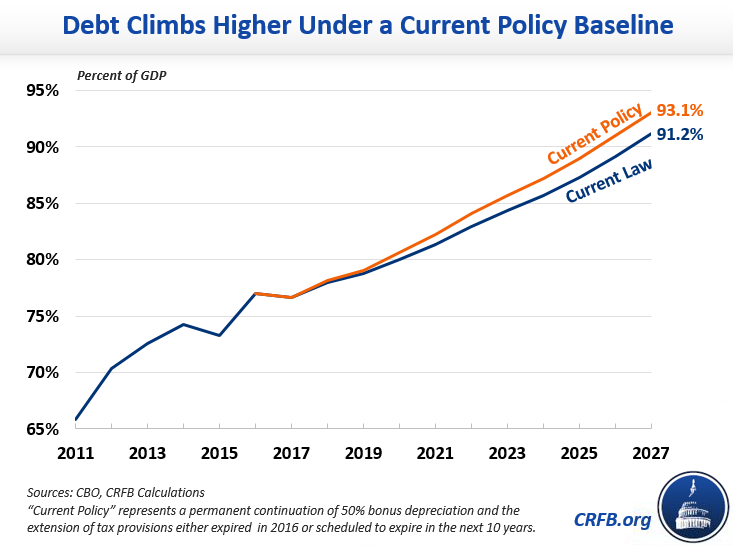

- A current policy baseline increases the debt. We listed the Five Reasons to Pay For Tax Reform, including that the debt is too high to add to it with unpaid-for tax cuts and that tax reform that does not add to the debt can do more for economic growth. Using a current policy baseline disguises a half-trillion dollar tax cut as "paid for" even though deficits would increase. Under a current policy baseline, debt held by the public would reach 93 percent of Gross Domestic Product (GDP) instead of 91 percent under CBO's current law projections.

- The House budget would no longer balance. The budget resolution reported by the House Budget Committee purports to achieve balance in ten years. It also assumes tax reform is revenue neutral relative to current law. If tax reform instead uses a current policy baseline, that budget would instead have a deficit of $50 billion in 2027.

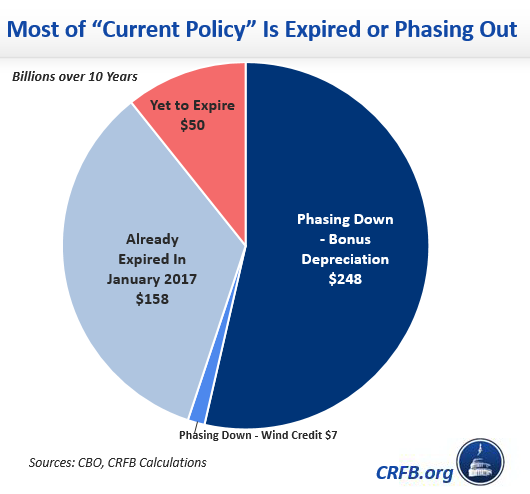

- Congress has indicated these provisions should expire. The tax agreement enacted in 2015 was intended to provide greater certainty in the tax code by permanently extending many of the temporary provisions, phasing down others, and letting others expire. Speaker of the House Paul Ryan (R-WI) said, "we are ending Washington’s days of extending tax policies one year at a time," while Senate Finance Committee Chairman Orrin Hatch (R-UT) said the bill was "putting an end to the repeated tax extenders exercise that has plagued Congress for decades.” The temporary provisions are not "current policy," since over 30 of them have already expired at the beginning of 2017. Another provision, bonus depreciation, was explicitly phased down over the next two years. If "current policy" is shorthand for Congressional intent, then Congress intended to have bonus depreciation phase down. By cost, almost 90 percent of the "current policy" provisions are either already expired or phasing down. It is inappropriate to suggest these represent "current policy."

- The baseline masks the choices that Congress is making. The Republican staff of the Senate Budget Committee noted that a current policy baseline hides the cost of extensions: "If these provisions are included, on the other hand, it masks the 'cost' of extending them, as the benchmark already would incorporate the revenue loss." If policymakers choose their own baseline, it allows them to hide the costs of policy proposals. If Congress wants to pass tax cuts, the cost should be acknowledged.

- The costs would disappear from the budget process. As we have previously explained, these expiring provisions were scored as temporary provisions when they were enacted. Congress never accounted for permanent costs of these provisions, and simply assuming they are continued in the baseline would hide those costs from the budget process. Some have argued that the current policy baseline makes tax programs treated more like spending programs, but this is an overly simplified view. All programs, whether tax or spending, are scored as either temporary or permanent. If they were originally scored as permanent, then the original legislation paid their costs and no additional costs are scored when the legislation is extended. If a program was originally scored as temporary (like these tax provisions), then the original legislation only paid the temporary costs, and further extensions cost money. This treatment ensures that all costs are accounted for at least once. If Congress only paid for the costs of a short-term extension, it should not be able to assume future extensions are automatically paid for.

- Congress would raise revenue from letting provisions expire on schedule. Under a current policy baseline, Congress could claim savings from removing a provision that was going to expire anyway or already expired at the start of 2017, improperly using that money to pay for a tax cut elsewhere.

- It creates an incentive for more temporary tax breaks. Using a current policy baseline establishes the precedent that temporary tax breaks can be later made permanent without being scored with a cost or requiring offsets. This would encourage Congress to enact new tax breaks as temporary measures, which would limit their cost and the amount of offsets needed, with the expectation that those provisions could later be made permanent without needing to offset the additional costs. Encouraging temporary provisions is counter to the idea of making a more permanent, stable, and simple tax code with tax reform.

Since enactment of the Congressional Budget Act of 1974, Congress has always used the CBO current law baseline as the basis for constructing and enforcing budget resolutions. However, the Budget Act does not explicitly require the current law baseline. Congress may have flexibility to choose which baseline will be used to score legislation and enforce the budget resolution, which is particularly important when trying to use reconciliation to pass tax reform without a 60-vote margin in the Senate.

Changing the baseline would allow a reconciliation bill for tax reform to reduce revenues by $462 billion below current law – and increase the deficit by $539 billion above current law with interest – but still comply with reconciliation instructions requiring the bill to nominally reduce the deficit. In addition, using a current policy baseline in the budget resolution would lower the bar for complying with the Senate PAYGO rule, which prohibits legislation that would increase the deficit relative to the budget resolution's baseline. However, the reconciliation bill would still be negative under the Statutory Pay-As-You-Go Act, which is enforced using a current law baseline.

The choice of baseline would also affect a bill’s dynamic estimate. If the Joint Committee on Taxation estimated legislation against a current policy baseline, the dynamic effects would likely be smaller for a plan like the House's Better Way that moves to full expensing, where businesses can immediately write off their capital purchases, instead of depreciating them over time.

A current policy baseline would assume continuation of bonus depreciation, so many investments could already be expensed at 50 percent. Full expensing would provide a smaller marginal benefit than it would relative to current law where bonus depreciation expires.

The revenue-neutral standard for tax reform is a useful fiscal goal that imposes some budget discipline, and any tax reform bill should be at least revenue neutral so as not to add to debt. We hope that Congress chooses to follow the long-established budget scoring rules to enforce revenue neutrality against current law. Neutrality should not be redefined using current policy to lower the bar, claim deficit neutrality, and obscure an increase in the deficit.